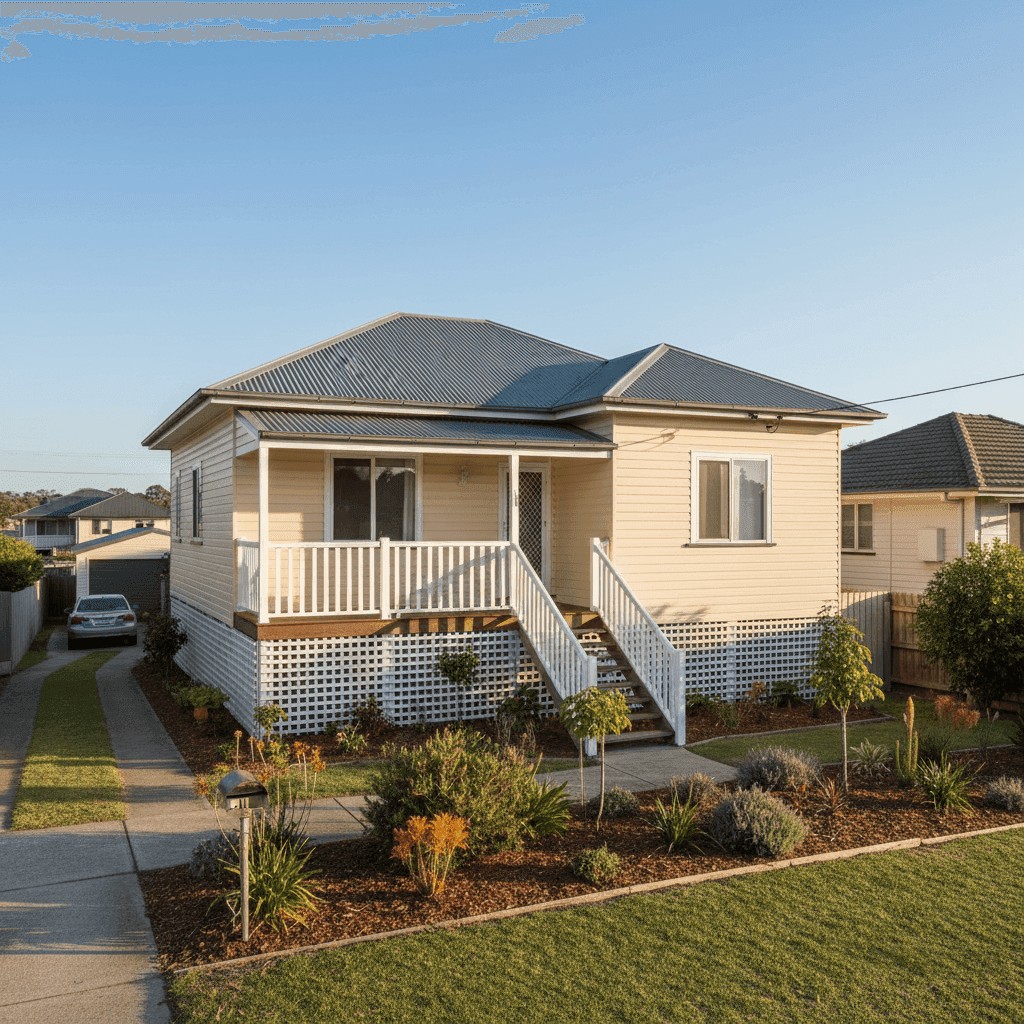

Warilla is a laid-back coastal suburb on the New South Wales South Coast, sitting within the Wollongong Local Government Area just a stone's throw from Lake Illawarra. It's a popular spot for owner-occupiers and downsizers alike, with a mix of older fibro homes and more modern builds lining quiet residential streets. If you own a free standing home here, understanding what drives your insurance premium — and whether you're paying a fair price — can make a real difference to your household budget.

This article breaks down a recent home and contents insurance quote for a 2-bedroom free standing home in Warilla, compares it against local, state and national benchmarks, and offers practical tips for getting the best value cover.

---

Is This Quote Fair?

The quote in question comes in at $2,494 per year (or $239 per month) for combined home and contents cover, with a building sum insured of $400,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, which is a reasonable result for this suburb and property type. Here's what that means in context:

- The suburb average for Warilla (postcode 2528) sits at $2,541/yr, meaning this quote comes in just below the local average — a positive sign.

- The suburb median is $2,002/yr, which is noticeably lower, suggesting there are cheaper options available in the market for comparable properties.

- The 25th percentile is $1,814/yr and the 75th percentile is $3,546/yr, so this quote falls comfortably in the middle range of what Warilla homeowners are paying.

In short, you're not being overcharged, but there's room to explore whether a more competitive premium is available — particularly if you can edge closer to that median figure. You can explore suburb-level insurance data for Warilla (2528) to see how quotes in your area are trending.

---

How Warilla Compares

One of the more striking takeaways from this data is just how favourably Warilla sits relative to broader benchmarks.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Warilla (2528) | $2,541/yr | $2,002/yr |

| Wollongong LGA | $2,751/yr | — |

| NSW State | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

The NSW state average of $9,528/yr looks alarming at first glance, but it's heavily skewed by high-risk and high-value properties across the state — think flood-prone regions, bushfire zones, and premium coastal real estate in Sydney. The median of $3,770/yr is a more grounded figure, and Warilla's median still comes in well below that.

Compared to the national average of $5,347/yr, the Warilla quote of $2,494/yr represents a significant saving — nearly half the national average. Even against the NSW state median, this quote looks competitive.

The Wollongong LGA average of $2,751/yr also provides useful local context. At $2,494/yr, this quote sits about $257 below the LGA average, which is encouraging for homeowners in the area.

> Note: The Warilla suburb sample includes 11 quotes, so while directionally useful, the local data should be interpreted with some caution given the relatively small sample size.

---

Property Features That Affect Your Premium

Several characteristics of this particular property influence how insurers price the risk. Here's what's worth understanding:

Hardiplank / Hardiflex External Walls

Fibre cement cladding products like Hardiplank and Hardiflex are generally viewed favourably by insurers. They're non-combustible, resistant to rot and termites, and hold up well in coastal environments — all of which can help moderate your premium compared to timber-clad homes.

Steel / Colorbond Roof

A Colorbond steel roof is another tick in the risk-mitigation column. It's durable, fire-resistant and handles severe weather well. Insurers tend to price these roofs more favourably than terracotta tiles or older corrugated iron, which can be prone to cracking or rusting.

Elevated Foundation (Stumps, at Least 1m)

This is a notable feature. The home sits on stumps and is elevated by at least one metre. While this style of construction — sometimes called a raised or Queenslander-style foundation — can improve ventilation and reduce flood risk in some contexts, insurers assess elevation carefully. Elevated homes can face higher wind-loading exposure and may have different repair cost profiles. It's worth confirming your building sum insured accurately reflects the cost to rebuild, including the subfloor structure.

Ducted Climate Control

The presence of ducted climate control adds to the replacement value of the home, which is factored into the building sum insured. Ensuring your sum insured accounts for the full cost of replacing this system is important — underinsurance is a common issue for homeowners who set and forget their cover.

Carpet Flooring & Standard Fittings

Carpet and standard-grade fittings are relatively straightforward to price. They don't push premiums up the way high-end timber floors or luxury fixtures might, which helps keep this quote in a reasonable range.

No Pool, No Solar Panels

The absence of a pool and solar panels simplifies the risk profile. Both can add complexity and cost to a policy, so their absence here is a modest premium-saver.

---

Tips for Homeowners in Warilla

1. Review Your Building Sum Insured Carefully

At $400,000 for a 105 sqm home built in 2006, the sum insured looks reasonable — but building costs have risen sharply in recent years. Use an independent building cost calculator or speak with a quantity surveyor to confirm this figure reflects current rebuild costs, including your elevated subfloor structure, ducted air conditioning and any outbuildings.

2. Compare Multiple Quotes Before Renewing

A "Fair" rating means you're around the average — but the suburb median of $2,002/yr suggests cheaper options exist. Get a fresh quote at CoverClub to see how different insurers price your specific property. Even a saving of $300–$400 per year adds up over time.

3. Consider Your Excess Level

This policy carries a $1,000 excess for both building and contents. Opting for a higher excess — say $1,500 or $2,000 — can meaningfully reduce your annual premium. Just make sure the excess is an amount you could comfortably cover in the event of a claim.

4. Keep Your Home Well-Maintained

Insurers look more favourably on well-maintained properties, and some will ask about the condition of your roof, gutters and subfloor during the underwriting process. Regular maintenance of your Colorbond roof and stump foundations can also prevent minor issues from becoming costly claims.

---

Ready to Compare?

Whether you're renewing your existing policy or shopping for cover for the first time, it pays to compare. CoverClub makes it easy to see how your quote stacks up against real data from your suburb and beyond. Start your comparison at CoverClub and make sure you're getting the right cover at a fair price.