If you own a free standing home in Warrock, VIC 3312, you already know this part of the Southern Grampians is a long way from the bustle of Melbourne — but that distance doesn't necessarily mean cheaper home insurance. A recent quote for a 1-bedroom weatherboard home in the area came in at $14,406 per year for combined home and contents cover. That's a significant figure, and it's worth unpacking exactly why this property attracts such a hefty premium — and what, if anything, can be done about it.

---

Is This Quote Fair?

The short answer: this quote is rated Expensive — above average by CoverClub's pricing benchmark. To put it in perspective, the Victorian state average premium sits at around $3,000 per year, with a median of $2,718. Even at the national level, where the average is $5,347 and the median $2,764, this quote is still dramatically higher.

At nearly 4.8 times the Victorian state average and more than 2.6 times the national average, a premium of $14,406 per year — or $1,381 per month — is a serious financial commitment. That said, it doesn't necessarily mean the insurer has made an error or is being unreasonable. Several compounding risk factors specific to this property and location are almost certainly driving the price upward. We'll explore those in detail below.

---

How Warrock Compares

Without suburb-level data available for Warrock specifically, we can look at the broader local government area of Southern Grampians, which has an average premium of $3,537 per year. That's already above the Victorian state average, suggesting that properties in this region carry elevated risk profiles compared to the broader state.

Here's a quick snapshot of how this quote stacks up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $14,406 |

| Southern Grampians LGA Average | $3,537 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

The gap between this quote and even the LGA average is stark. While the Southern Grampians region already trends above the state norm, this particular property sits well above even that elevated benchmark — pointing to a combination of property-specific characteristics that insurers view as high risk.

---

Property Features That Affect Your Premium

Several features of this property are likely contributing significantly to the above-average premium. Understanding them can help you make informed decisions.

Heritage Overlay

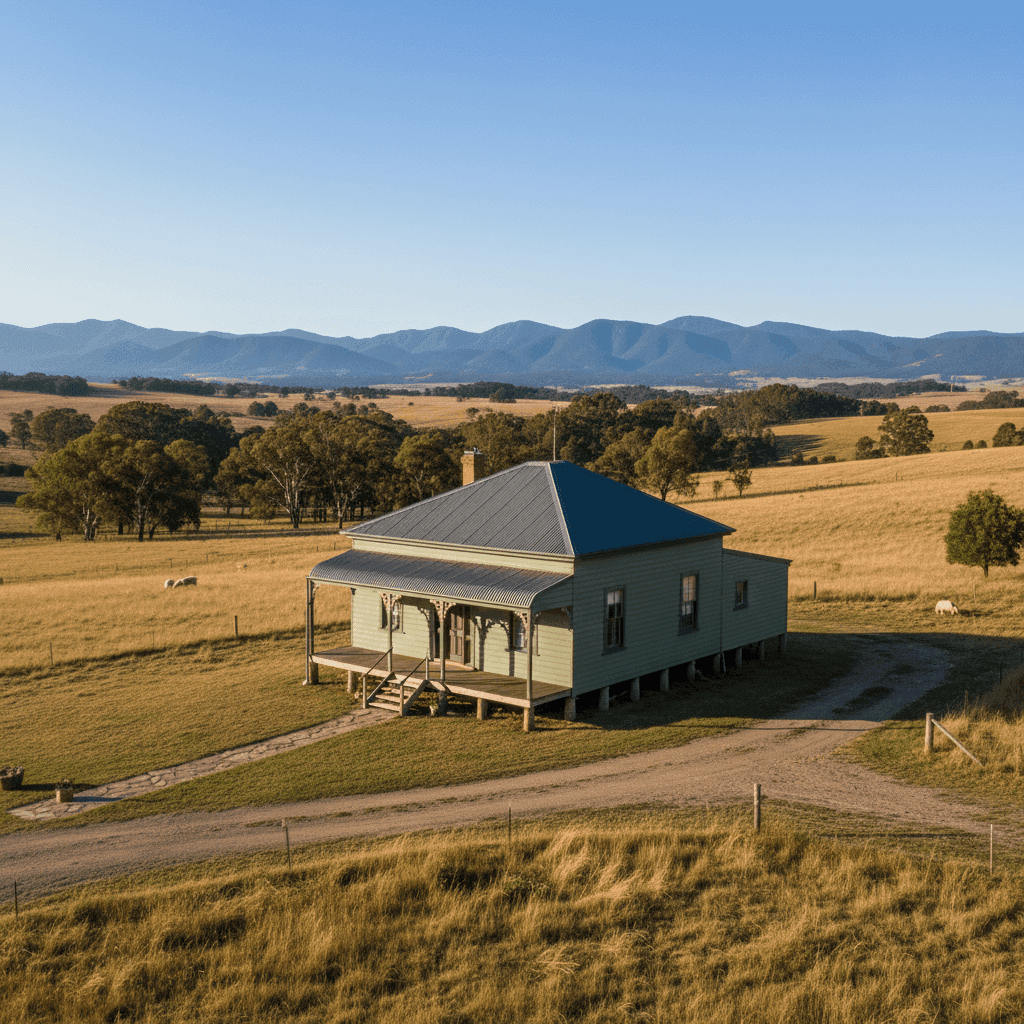

This is arguably the single biggest factor. The property carries a Heritage Overlay, meaning it is subject to heritage protection regulations. For insurers, this is a major cost driver — if the home is damaged, repairs must often use period-appropriate materials and techniques, which are significantly more expensive than standard modern construction methods. Finding qualified tradespeople who can work on heritage properties also adds to rebuild complexity and cost.

Weatherboard Timber Construction

Weatherboard wood external walls are a common feature of older Australian homes, but they come with elevated risk in the eyes of insurers. Timber is more susceptible to fire, rot, and pest damage than brick or steel alternatives. In rural Victoria, where properties may be further from fire services, this risk is amplified.

Age of Construction — 1906

At over 115 years old, this home is well into heritage territory. Older properties typically have ageing electrical wiring, plumbing, and structural elements that increase the likelihood of a claim. Insurers price this risk accordingly.

Stump Foundation

Homes built on stumps (also called pier or post foundations) are common in older Victorian properties. While they offer good ventilation and can handle ground movement, they are more exposed to damage from moisture, pests, and subsidence over time — all of which factor into premium calculations.

Timber and Laminate Flooring

Timber flooring in an older home can be expensive to repair or replace, particularly if it's original hardwood. This increases the contents and building replacement costs, which in turn affects the sum insured and premium.

Rural Location

Warrock is a small rural locality in western Victoria. Properties in rural and regional areas often face longer response times from emergency services, which can increase the severity of fire and storm damage events. This geographic risk is reflected in premiums across the Southern Grampians LGA.

Sum Insured

The building is insured for $200,000 with $21,000 in contents cover. While these figures may seem modest, the heritage listing means the true cost to rebuild to heritage standards could be considerable — and insurers price for that complexity.

---

Tips for Homeowners in Warrock

If you're looking to manage your insurance costs without compromising on cover, here are some practical steps worth considering:

1. Review Your Sum Insured Carefully

Make sure your building sum insured accurately reflects the cost to rebuild your home — not its market value. For a heritage property, this figure can be surprisingly high due to specialised labour and materials. Underinsuring to save on premiums can leave you seriously exposed after a claim.

2. Shop Around and Compare Quotes

Not all insurers price heritage weatherboard homes the same way. Some have more appetite for older, character-rich properties than others. Using a comparison platform like CoverClub allows you to see multiple quotes side by side and identify whether a better rate is available for your specific circumstances.

3. Consider a Higher Excess

Both the building and contents excess on this policy are set at $1,000. Opting for a higher voluntary excess — say, $2,500 or $5,000 — can meaningfully reduce your annual premium. This strategy works best if you have savings to cover the excess in the event of a claim and don't anticipate making frequent smaller claims.

4. Maintain the Property Proactively

Insurers look favourably on well-maintained properties. For a heritage weatherboard home, this means regularly inspecting and treating timber for rot and pests, keeping gutters clear, ensuring the roof is in good condition, and having electrical systems inspected periodically. A well-maintained property reduces your actual risk — and can support your case when negotiating with insurers.

---

Ready to Find a Better Rate?

A premium of $14,406 per year is a significant outlay, and it's always worth checking whether you can do better. At CoverClub, we make it easy to compare home and contents insurance quotes from multiple providers — so you can see exactly where your money is going and whether there's a more competitive option out there. Get a quote today and find out what Warrock homeowners are actually paying for cover like yours.