Warwick, nestled in Queensland's Southern Downs region, is a charming regional city known for its heritage architecture, cool-climate gardens, and relaxed lifestyle. But like any property owner in Queensland, homeowners here face the ongoing challenge of securing adequate insurance at a fair price. This article breaks down a real home and contents insurance quote for a three-bedroom, free-standing home in Warwick (postcode 4370) — and helps you understand whether the price stacks up.

---

Is This Quote Fair?

The quote in question comes in at $3,565 per year (or $343/month) for combined home and contents cover, with a building sum insured of $750,000 and contents valued at $85,000. Both the building and contents excess are set at $2,000.

Our analysis rates this quote as Expensive — above average for the area.

To put that in context: the suburb average for Warwick (4370) sits at $2,544/yr, with a median of $2,464/yr. This quote lands well above both figures — and even sits above the suburb's 75th percentile of $3,127/yr, meaning it's pricier than roughly three-quarters of comparable quotes in the area.

That said, "expensive" doesn't automatically mean "wrong." The sum insured here is $750,000 for the building, which is on the higher end and will naturally push the premium up. The contents cover of $85,000 is also a meaningful addition. Still, it's worth shopping around to ensure you're not overpaying for equivalent coverage.

---

How Warwick Compares

Understanding where your premium sits relative to broader benchmarks is one of the most useful tools a homeowner has. Here's how this quote lines up:

| Benchmark | Premium |

|---|---|

| This Quote | $3,565/yr |

| Warwick (4370) Suburb Average | $2,544/yr |

| Warwick (4370) Suburb Median | $2,464/yr |

| Warwick 25th Percentile | $1,963/yr |

| Warwick 75th Percentile | $3,127/yr |

| Southern Downs LGA Average | $2,861/yr |

| QLD State Median | $3,903/yr |

| QLD State Average | $9,129/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. First, the QLD state average of $9,129/yr is extraordinarily high — heavily skewed by coastal and cyclone-prone postcodes in Far North Queensland where premiums can run into the tens of thousands. The state median of $3,903/yr is a more representative figure, and this quote actually falls below that mark, which is a more encouraging sign.

Compared to the national average of $5,347/yr, this quote also looks reasonable. However, when benchmarked against the local Warwick suburb data — based on 60 quotes — it's clearly on the higher end. The Southern Downs LGA average of $2,861/yr further reinforces that most comparable properties in the region are insured for less.

The takeaway: this quote isn't outrageous in a broader Queensland or national context, but locally it's above what most Warwick homeowners are paying.

---

Property Features That Affect Your Premium

Several characteristics of this property help explain why the premium sits where it does — and some may be working against the homeowner more than others.

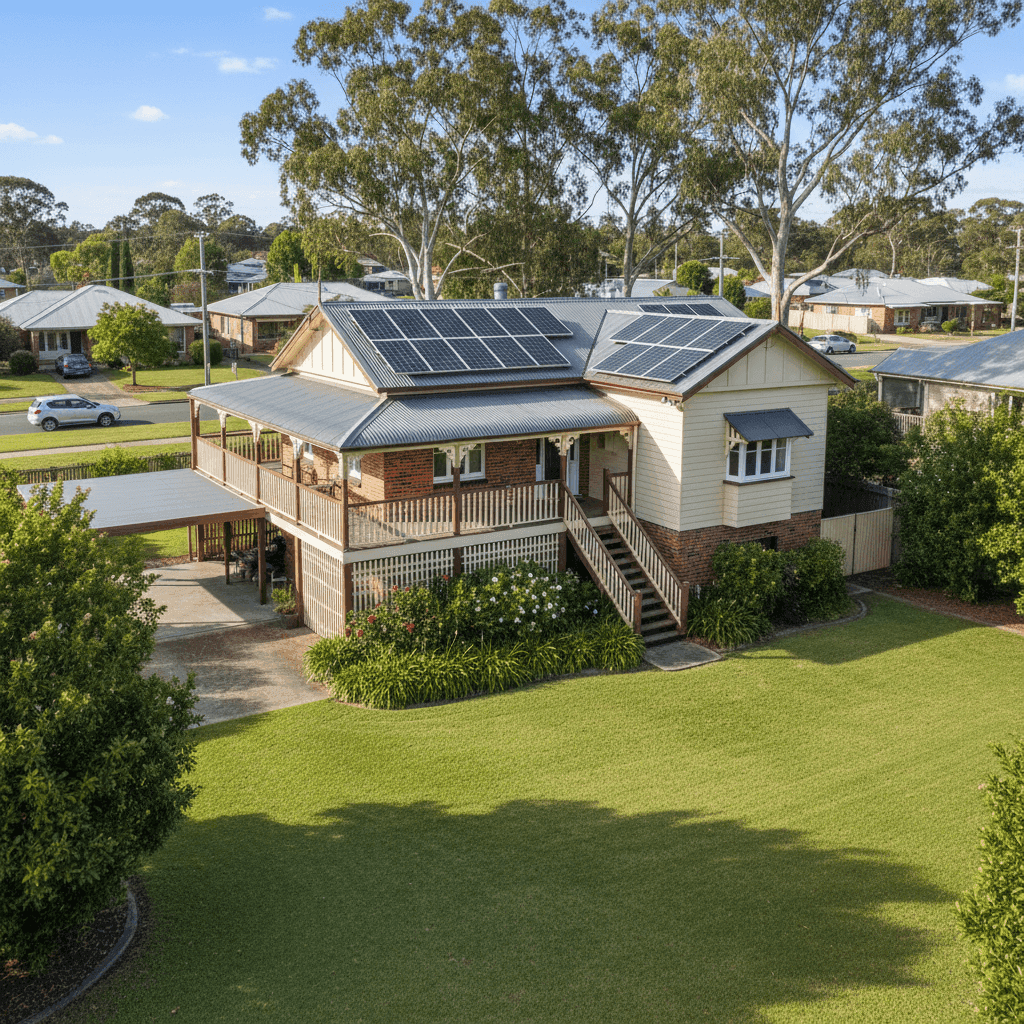

Age of construction (1967): Older homes, particularly those built before modern building codes were introduced, can attract higher premiums. Insurers factor in the increased likelihood of outdated wiring, plumbing, and structural elements that may be more costly to repair or replace.

Elevated on stumps: This is a classic Queensland construction style — the elevated, stump-based design offers excellent ventilation and some flood resilience. However, insurers can view stumped homes as having higher repair complexity, particularly for underfloor damage or structural movement over time.

Timber/laminate flooring: Timber floors, while beautiful, are more susceptible to water damage than tiles or concrete. This can influence the contents and building risk assessment, particularly in a region that does experience periodic rainfall events.

External walls listed as "Other": Non-standard wall construction materials can sometimes attract a loading on premiums, as they may be harder or more expensive to source and repair compared to brick veneer or weatherboard.

Solar panels: Great for the electricity bill, but solar panels add to the insured value of the building and introduce additional risk (fire, storm damage, panel replacement costs). Most insurers include them under building cover, which contributes to a higher sum insured.

Ducted climate control: Similarly, ducted systems are expensive to repair or replace and are typically included in the building sum insured, contributing to the overall premium.

No pool, no cyclone risk zone: These are genuine positives. Pools introduce liability and equipment risks, and being outside a cyclone risk area removes one of the biggest premium drivers in Queensland.

Building size (130 sqm) and sum insured ($750,000): The rebuild cost estimate of $750,000 for a 130 sqm home works out to roughly $5,770 per square metre — which is on the higher side. It may be worth reviewing whether this figure accurately reflects current rebuild costs in the Southern Downs region, as over-insuring can unnecessarily inflate your premium.

---

Tips for Homeowners in Warwick

1. Review your building sum insured carefully A $750,000 sum insured for a 130 sqm home may be higher than necessary. Use a reputable building cost calculator or speak with a local builder to get a realistic rebuild estimate. Adjusting this figure (without under-insuring) could meaningfully reduce your annual premium.

2. Consider increasing your excess Both the building and contents excess are currently set at $2,000. If you have the financial buffer to absorb a higher out-of-pocket cost in the event of a claim, opting for a higher excess (e.g., $3,000–$5,000) can reduce your annual premium noticeably.

3. Shop around at renewal time Insurer loyalty rarely pays off in Australia. Premiums can vary significantly between providers for the same property and coverage level. Use a comparison platform like CoverClub to benchmark quotes before your renewal date — ideally 4–6 weeks out.

4. Ask about discounts for security and safety features Some insurers offer premium reductions for homes with security systems, smoke alarms, or deadbolts. Given this home already has solar panels and ducted climate control, it's worth asking whether any additional safety features could attract a discount.

---

Compare Your Home Insurance Today

Whether you're a long-time Warwick local or new to the Southern Downs, it pays to know what others are paying for similar cover. CoverClub makes it easy to see real quote data for your suburb and compare your options side by side. Get a home insurance quote today and find out if you could be paying less — without sacrificing the cover you need.