If you own a semi detached home in Wattle Glen, VIC 3096, you're likely no stranger to the rolling green hills, leafy streetscapes, and semi-rural charm that make this pocket of the Nillumbik Shire so appealing. But with that lifestyle comes a set of insurance considerations that can push your annual premium well above what flat suburban properties elsewhere might attract. This article breaks down a recent home and contents insurance quote for a four-bedroom, two-bathroom semi detached property in Wattle Glen — and helps you understand exactly what's driving the cost.

---

Is This Quote Fair?

The quote in question comes in at $3,134 per year (or $300 per month) for combined home and contents cover, with a building sum insured of $948,000 and contents valued at $100,000. Both the building and contents excess are set at $500.

Our price rating for this quote is Expensive — above average for the Wattle Glen suburb.

To put that in perspective: the suburb average for comparable properties sits at $1,877 per year, and the median is even lower at $1,743 per year. This quote is roughly 67% above the suburb average, which is a significant gap worth investigating before simply accepting the renewal or new policy offer.

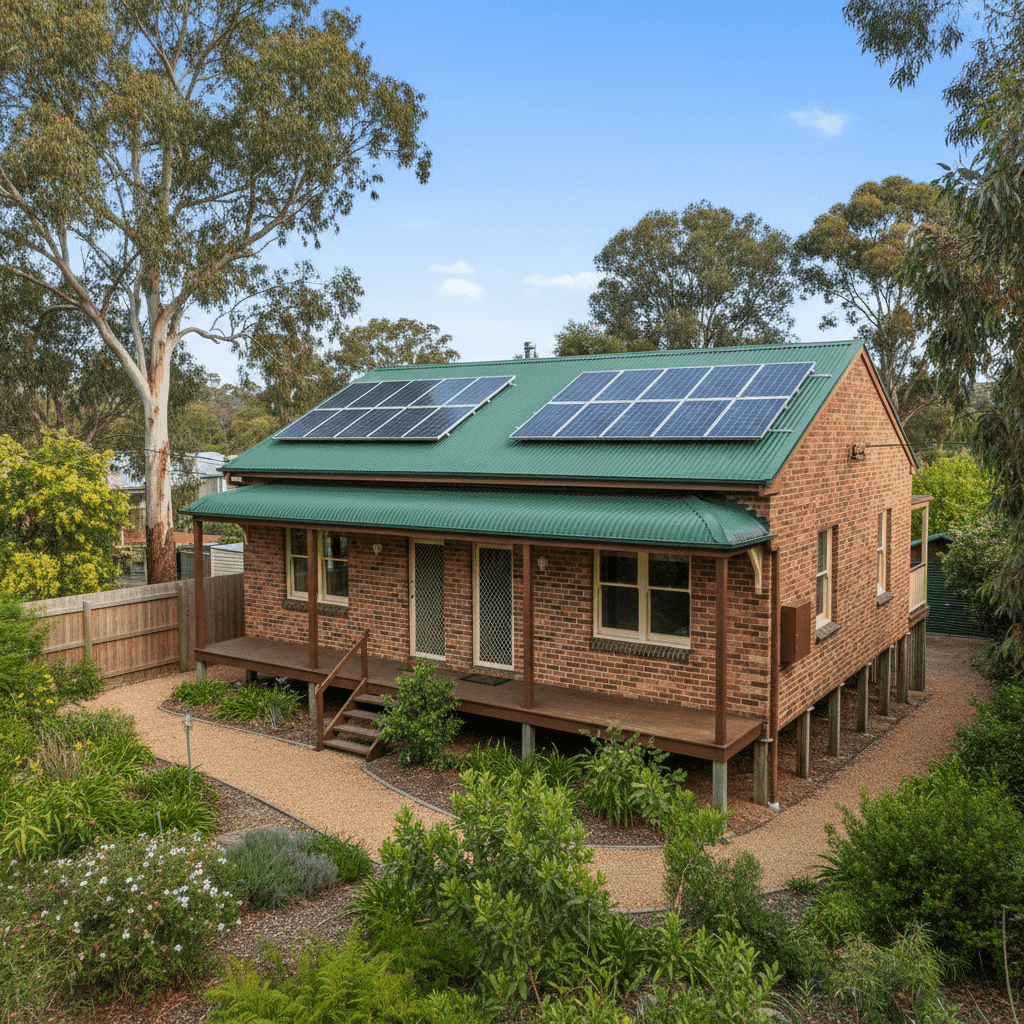

That said, "expensive relative to the suburb" doesn't automatically mean the quote is unreasonable. The building sum insured of $948,000 is substantial, and a 235 sqm brick veneer semi detached built in 1996 with ducted climate control and solar panels will naturally attract a higher replacement cost than a smaller, more modest dwelling. Insurers price to the rebuild — not the land value — so a well-appointed, larger-than-average home will always sit at the upper end of the local range.

---

How Wattle Glen Compares

Understanding where your premium sits in the broader landscape is one of the most useful tools a homeowner has. Here's how this quote stacks up across three levels:

| Benchmark | Premium |

|---|---|

| Wattle Glen suburb average | $1,877/yr |

| Wattle Glen suburb median | $1,743/yr |

| Wattle Glen 75th percentile | $2,064/yr |

| This quote | $3,134/yr |

| VIC state average | $3,000/yr |

| VIC state median | $2,718/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| Nillumbik LGA average | $3,693/yr |

A few things stand out here. First, this quote actually sits below the Nillumbik LGA average of $3,693 per year — which suggests that across the broader shire, insurers are pricing properties at a notably higher level, likely reflecting bushfire exposure and the rural-interface nature of the region. Second, it's almost exactly in line with the Victorian state average of $3,000 per year, which means while it looks expensive locally, it's broadly consistent with what Victorian homeowners are paying across the state.

For national context, the national average home insurance premium sits at $5,347 per year, though this is heavily skewed by high-risk areas in Queensland and Northern Australia. The national median of $2,764 is a more useful yardstick — and this quote sits modestly above that figure.

You can explore more local data on the Wattle Glen suburb insurance stats page or browse Victoria-wide premium trends to get a fuller picture.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Here's what's most relevant:

Brick veneer construction with a Colorbond roof Brick veneer is generally viewed favourably by insurers — it's durable, relatively fire-resistant, and widely understood by assessors. A steel Colorbond roof is similarly well-regarded: it's lightweight, long-lasting, and performs well in high-wind and ember-attack scenarios. Together, these materials help keep the premium more manageable than, say, a weatherboard home with a tiled roof.

Stump foundation and elevation This property sits on stumps and is elevated by less than one metre. While this is a common construction method for older Victorian homes (particularly in hilly terrain like Wattle Glen), it does introduce some additional considerations around subfloor ventilation, pest exposure, and the cost of access during repairs. Insurers may factor this into their pricing.

Solar panels and ducted climate control Both of these features increase the insured value of the home. Solar panels represent a meaningful capital investment that must be covered under the building sum insured, and ducted climate control systems are expensive to repair or replace. Their inclusion is one reason the $948,000 building sum is appropriate for a property of this size and specification.

Bushfire and environmental risk Wattle Glen sits within the Nillumbik Shire — an area with well-documented bushfire risk. While this property is not in a cyclone risk zone, the surrounding vegetation and semi-rural interface location are factors that insurers weigh carefully. This is reflected in the elevated Nillumbik LGA average of $3,693 per year compared to the suburb-level figures.

No pool The absence of a pool removes one common source of liability and contents complexity from the policy, which works in the homeowner's favour.

---

Tips for Homeowners in Wattle Glen

If you're looking to get better value from your home insurance without compromising on cover, here are four practical steps worth taking:

- Review your building sum insured annually. Construction costs have risen sharply in recent years, and an underinsured property can leave you significantly out of pocket after a major claim. Use an independent building cost calculator or ask your insurer to justify the figure they're using — $948,000 for 235 sqm in this region is plausible, but worth verifying.

- Compare at least three quotes before renewing. The 31-quote sample for Wattle Glen shows a wide spread — from $1,550 at the 25th percentile to over $2,064 at the 75th percentile. There's meaningful variation in how insurers price this suburb, and shopping around could save you hundreds of dollars annually.

- Ask about bushfire mitigation discounts. Some insurers offer reduced premiums for properties with ember guards, maintained asset protection zones (APZs), or non-combustible decking. Given Wattle Glen's bushfire risk profile, any steps you've taken to harden your home could be worth mentioning when you apply.

- Consider your excess strategically. The $500 excess on both building and contents is relatively modest. Increasing your excess — particularly on the building component — can reduce your annual premium noticeably. Just make sure you could comfortably cover the higher excess amount if you needed to make a claim.

---

Compare Your Options with CoverClub

Whether this quote represents good value ultimately depends on the specific policy inclusions, the insurer's claims reputation, and how well the cover aligns with your circumstances. The numbers suggest it's priced at the higher end locally but sits within a reasonable range for the Nillumbik region and the Victorian state average.

The smartest move is to compare. At CoverClub, you can benchmark your premium against real quotes from across your suburb and state — so you know exactly where you stand. Get a home insurance quote today and find out if you could be paying less for the same level of protection.