If you own a free standing home in Wattle Ponds, NSW 2330, you've probably wondered whether you're paying a fair price for home insurance — or leaving money on the table. This article breaks down a real home and contents insurance quote for a three-bedroom property in the area, benchmarks it against local, state, and national data, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The annual premium for this quote came in at $2,966 per year (or $277 per month), covering both building and contents for a sum insured of $568,000 on the building and $50,000 on contents. The building excess is $5,000 and the contents excess is $2,000.

Our price rating for this quote is CHEAP — below average for the area. That's genuinely good news for the homeowner. To put it in perspective:

- The suburb average for Wattle Ponds is $5,463/yr, and the median sits even higher at $6,099/yr

- This quote comes in 45% below the suburb average and well beneath the 25th percentile of $3,134/yr — meaning it's cheaper than at least 75% of comparable quotes in the area

- Against the NSW state average of $9,528/yr, this quote looks even more competitive, though it's worth noting the NSW median is $3,770/yr, suggesting a wide spread of premiums across the state

In short: this is a strong result. Whether it reflects smart shopping, a favourable risk profile, or both, the homeowner is paying well under the going rate for this suburb.

---

How Wattle Ponds Compares

Understanding where Wattle Ponds sits in the broader insurance landscape helps contextualise any quote you receive. You can explore the full local data on the Wattle Ponds insurance stats page.

| Benchmark | Premium |

|---|---|

| This Quote | $2,966/yr |

| Suburb 25th Percentile | $3,134/yr |

| Suburb Average | $5,463/yr |

| Suburb Median | $6,099/yr |

| Suburb 75th Percentile | $7,293/yr |

| NSW State Average | $9,528/yr |

| NSW State Median | $3,770/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

| LGA (Hawkesbury) Average | $10,350/yr |

A few things stand out here. First, the Hawkesbury LGA average of $10,350/yr is strikingly high — more than three times this quote — which likely reflects elevated flood and bushfire risk across parts of the Hawkesbury region. Wattle Ponds, sitting within the broader Hunter Valley area near Singleton, may benefit from a comparatively lower risk profile than flood-prone Hawkesbury townships closer to the river system.

Second, the gap between the NSW average ($9,528) and median ($3,770) is enormous, pointing to a small number of very high-risk or high-value properties pulling the average up significantly. The NSW insurance stats page has more detail on this spread.

Compared to national benchmarks, this quote also sits just above the national median of $2,764/yr — reasonable for a property of this size and specification.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth examining through an insurance lens:

Vinyl Cladding Exterior Vinyl cladding is generally viewed as a moderate-risk wall material. It's not as robust as brick veneer in a fire scenario, but it's also less susceptible to moisture damage than some timber alternatives. Insurers may price this slightly higher than brick but lower than weatherboard.

Steel/Colorbond Roof This is a positive for insurers. Colorbond steel roofing is durable, fire-resistant, and handles hail better than terracotta or concrete tiles. It's one of the more insurer-friendly roofing materials available in Australia, and likely contributes to a more competitive premium.

Slab Foundation Concrete slab foundations are considered low-risk by most underwriters. There's no subfloor cavity to harbour pests or moisture, and slabs tend to perform well in most ground conditions — a tick in the risk assessment column.

Timber/Laminate Flooring Flooring type can affect contents and building replacement costs. Timber and laminate are mid-range in cost to replace, but they can be vulnerable to water damage. This is worth keeping in mind when reviewing your sum insured.

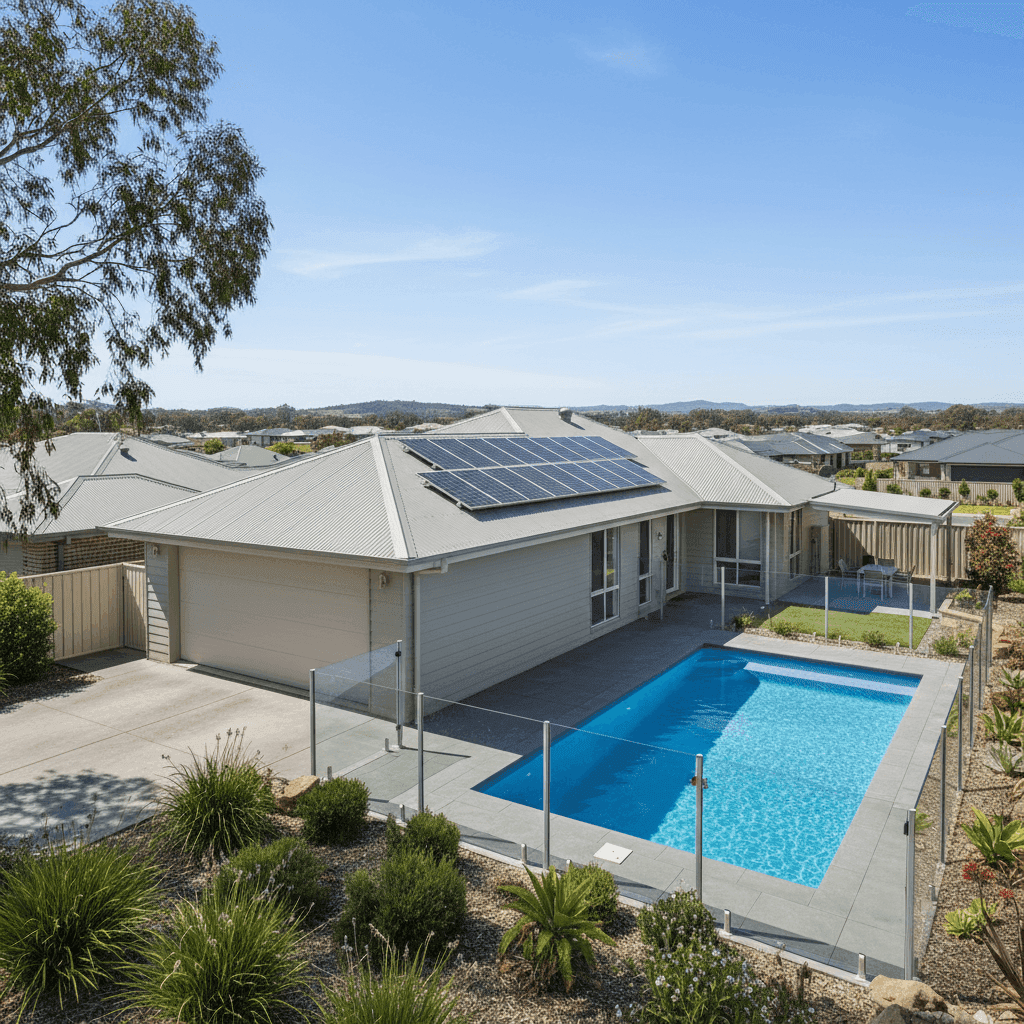

Pool, Solar Panels & Ducted Climate Control These three features add value to the property and can increase replacement costs. A pool introduces liability considerations (particularly relevant in NSW given strict pool safety legislation), while solar panels add to the building sum insured. Ducted climate control systems can be expensive to replace — make sure your $568,000 building sum insured accounts for all of these.

No Cyclone Risk Wattle Ponds is not in a cyclone-risk zone, which keeps premiums lower compared to properties in northern Queensland or coastal WA. This is a meaningful factor in the competitive pricing seen here.

---

Tips for Homeowners in Wattle Ponds

1. Double-check your sum insured covers everything With solar panels, a pool, and ducted air conditioning, your building replacement cost can creep up quickly. Use a building cost calculator or ask your insurer to confirm that $568,000 would genuinely cover a full rebuild — including demolition, site clearance, and professional fees.

2. Review your contents cover annually $50,000 in contents cover is on the modest side for a three-bedroom, two-bathroom home with standard fittings. If you've acquired new furniture, appliances, or electronics since taking out the policy, it may be worth increasing this figure to avoid being underinsured at claim time.

3. Understand your excess before a claim A $5,000 building excess is relatively high. This means you'll be out of pocket for the first $5,000 of any building claim. If you're comfortable with that trade-off for a lower premium, great — but make sure you have that amount accessible if you ever need to lodge a claim.

4. Compare quotes at renewal time Even if this quote is already below average, the insurance market shifts every year. Insurers reprice based on claims data, reinsurance costs, and weather events. What's cheap today may not be cheap in 12 months. Set a reminder to compare quotes before your renewal date to ensure you stay on the right side of the market.

---

Ready to See What You Could Pay?

Whether you're a first-time buyer or a long-time Wattle Ponds resident, comparing home insurance quotes is one of the easiest ways to save money without sacrificing cover. CoverClub makes it simple to see multiple quotes side by side, so you always know if you're getting a fair deal.