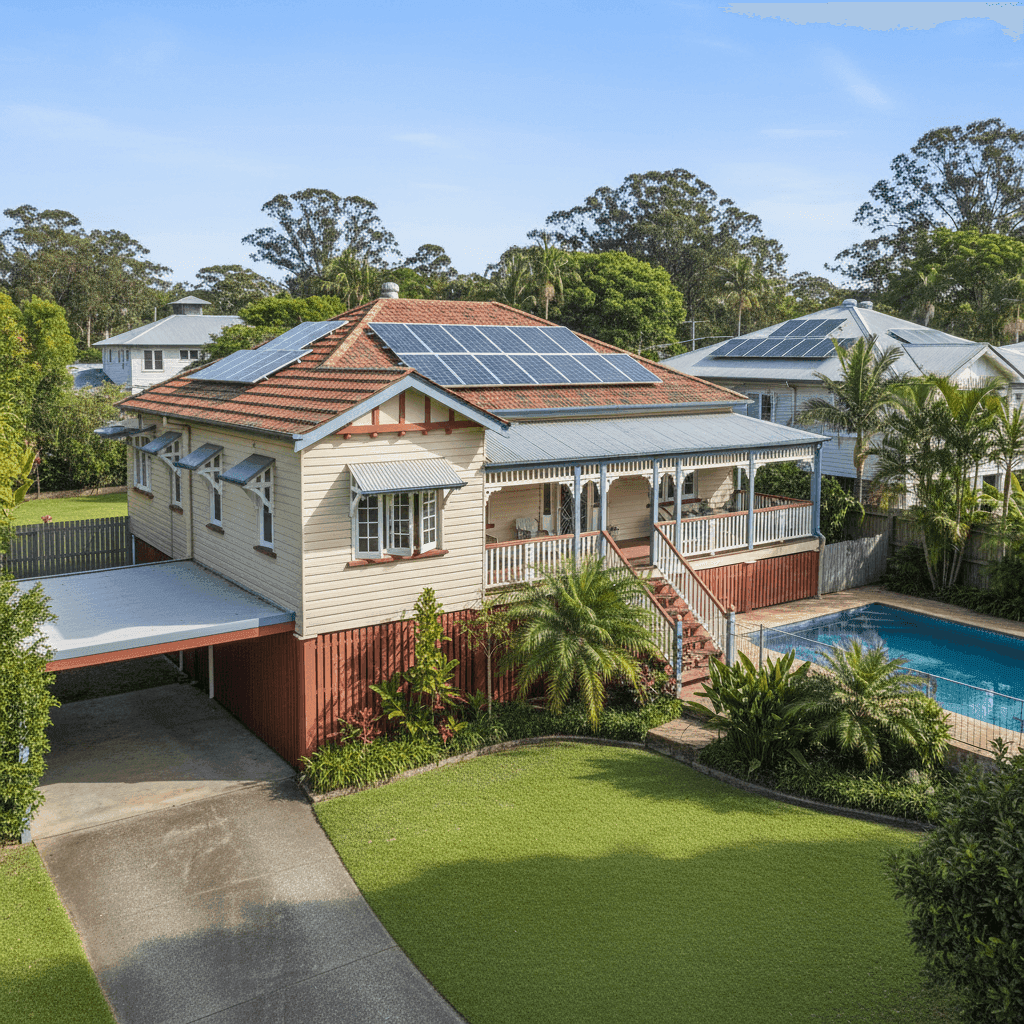

Wavell Heights is a well-established suburb in Brisbane's north, known for its leafy streets and a mix of classic post-war homes alongside more modern renovations. If you own a free standing home here — particularly one of the character-filled weatherboard properties that define the area — understanding what you should be paying for home and contents insurance is an important part of protecting one of your biggest assets. This article breaks down a real insurance quote for a 4-bedroom, 2-bathroom home in Wavell Heights (QLD 4012), and puts the numbers in context so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $1,859 per year (or $182/month) for combined home and contents cover, with a building sum insured of $759,000 and contents valued at $133,000. The building excess sits at $2,000, and the contents excess at $600.

Our pricing analysis rates this quote as Fair — Around Average. That's a reasonable outcome, but it's worth unpacking what "average" actually means in this context.

Within Wavell Heights itself, the suburb average premium is $2,490/yr and the median sits slightly higher at $2,524/yr — meaning this quote is notably below both benchmarks. In fact, at $1,859, this policy sits closer to the 25th percentile of $1,509/yr than to the median, suggesting it's on the more competitive end of what's available locally. Homeowners paying near the suburb's 75th percentile are forking out $3,402/yr or more — nearly double this quote.

So while the "Fair" rating might sound middling, the underlying data tells a more positive story: this is a below-average price for Wavell Heights, which is a solid result for a property with a high sum insured and quality fittings.

---

How Wavell Heights Compares

To appreciate how this quote stacks up, it helps to zoom out and look at the broader picture. You can explore the full breakdown on the Wavell Heights insurance stats page.

| Benchmark | Premium |

|---|---|

| This Quote | $1,859/yr |

| Wavell Heights Suburb Average | $2,490/yr |

| Wavell Heights Suburb Median | $2,524/yr |

| QLD State Average | $4,547/yr |

| QLD State Median | $3,931/yr |

| National Average | $2,965/yr |

| National Median | $2,716/yr |

The contrast with Queensland's state-wide averages is striking. The QLD average of $4,547/yr is more than 2.4 times this quote — a reflection of the significant insurance burden faced by homeowners in cyclone-prone coastal and far-north Queensland regions, which pull the state figures upward considerably.

Even compared to national averages, this quote performs well. The national average of $2,965/yr and median of $2,716/yr are both comfortably above what's being paid here.

It's also worth noting the Brisbane LGA average of $16,277/yr — an extraordinarily high figure that is almost certainly skewed by commercial or high-value properties within the broader LGA dataset, and shouldn't be taken as a typical residential benchmark.

Based on a sample of 52 quotes in the suburb, Wavell Heights homeowners are paying a wide range of premiums. The spread between the 25th percentile ($1,509/yr) and 75th percentile ($3,402/yr) is substantial, which underscores just how much individual property features, insurer choice, and cover levels can influence your final premium.

---

Property Features That Affect Your Premium

Several characteristics of this particular property have a meaningful impact on the insurance premium — for better and for worse.

Weatherboard Timber Construction

Weatherboard wood external walls are common in Brisbane's older suburbs, and while they give homes enormous character, they do carry a higher fire risk than brick or rendered masonry. Insurers typically price this in, so it's notable that this quote remains competitive despite the timber construction.

Age of the Home (Built 1947)

At nearly 80 years old, this home falls into a category that insurers assess carefully. Older homes can have ageing electrical wiring, plumbing, and structural elements that increase the likelihood of a claim. However, a well-maintained heritage-style home with updated systems can still attract reasonable premiums.

Stump Foundation & Elevated Design

The home sits on stumps and is elevated by less than one metre — a classic Queensland construction style. This elevation can actually be a modest flood-mitigation factor, though it also means the subfloor space requires attention. Insurers will consider the foundation type when assessing structural risk.

Tiled Roof

Terracotta or concrete tile roofs are generally viewed favourably by insurers compared to older materials like fibrous cement sheeting. They offer good durability and weather resistance, which can support a more competitive premium.

Pool, Solar Panels & Ducted Climate Control

These features increase the overall replacement cost of the home, which is reflected in the $759,000 building sum insured. A pool adds liability considerations, solar panels represent a significant capital investment, and ducted climate control systems are expensive to replace. All three are correctly captured in the sum insured to avoid underinsurance.

Top-of-the-Range Fittings

With premium fittings throughout, the cost to rebuild or repair this home to its current standard is higher than a comparable property with standard finishes. This is a key reason the building sum insured is set at $759,000 — and getting this figure right is critical.

---

Tips for Homeowners in Wavell Heights

1. Review your sum insured annually Construction costs have risen sharply in recent years. A sum insured that was adequate two years ago may no longer cover a full rebuild today — especially for a home with top-of-the-range fittings and extras like a pool and solar system. Use a building cost calculator or speak with a quantity surveyor to validate your figure.

2. Ask about discounts for security and safety features Many insurers offer premium reductions for homes with monitored alarms, deadbolts, and smoke detectors. Given this home's timber construction, demonstrating active fire safety measures could work in your favour at renewal time.

3. Consider your excess strategy This policy carries a $2,000 building excess. A higher excess typically lowers your premium, but make sure you can comfortably cover that amount out of pocket in the event of a claim. For contents, the $600 excess is relatively modest — review whether adjusting either figure makes financial sense for your situation.

4. Compare quotes at every renewal The 52-quote sample for Wavell Heights shows a wide pricing range. Loyalty doesn't always pay in insurance — shopping around at renewal can reveal meaningful savings without sacrificing cover quality. Even a "Fair" quote can often be improved with the right comparison.

---

Ready to Compare?

Whether you're renewing soon or just curious about what you should be paying, comparing quotes is the single most effective way to ensure you're not overpaying. Get a home and contents insurance quote at CoverClub and see how your current premium stacks up against the market in seconds.