If you own a free standing home in Wedderburn, NSW 2560, you're probably curious about what a fair home insurance premium looks like — and whether you're paying too much, too little, or just right. This article breaks down a real home and contents insurance quote for a three-bedroom, three-bathroom brick veneer home in Wedderburn, comparing it against suburb, state, and national benchmarks so you can make a more informed decision at renewal time.

---

Is This Quote Fair?

The quote in question comes in at $4,174 per year (or $409 per month) for combined home and contents cover, with a building sum insured of $692,000 and contents valued at $150,000. The building excess is $5,000 and the contents excess is $2,000.

Our price rating for this quote? Cheap — below average. That's genuinely good news for the homeowner.

To put it in perspective: the average home insurance premium across Wedderburn sits at $7,260 per year, and the median is $6,357 per year. This quote comes in at roughly 42% below the suburb average and well beneath even the 25th percentile of local quotes ($5,447/yr) — meaning it's cheaper than at least 75% of comparable quotes in the area. That's a meaningful saving of over $3,000 annually compared to what many Wedderburn homeowners are paying.

It's worth noting that the excess settings here are on the higher side — $5,000 for building and $2,000 for contents. Choosing a higher excess is a common and legitimate strategy to reduce your premium, so this likely contributes to the competitive price. Just make sure you're comfortable covering that amount out of pocket in the event of a claim.

---

How Wedderburn Compares

Understanding where Wedderburn sits in the broader insurance landscape helps frame just how competitive this quote really is.

| Benchmark | Premium |

|---|---|

| This quote | $4,174/yr |

| Wedderburn suburb average | $7,260/yr |

| Wedderburn suburb median | $6,357/yr |

| NSW state average | $9,528/yr |

| NSW state median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| Wollongong LGA average | $2,751/yr |

A few things stand out here. The NSW state average of $9,528/yr is notably high — driven in part by elevated premiums in flood-prone, bushfire-exposed, and coastal regions across the state. The national average of $5,347/yr is more moderate, though still above this quote.

Interestingly, the Wollongong LGA average of $2,751/yr is significantly lower than the Wedderburn suburb average, suggesting there may be considerable variation within the broader LGA depending on specific suburb risk profiles. You can explore more localised data on the Wedderburn suburb stats page.

It's also worth noting that with only nine quotes in the suburb sample, the local data has a relatively small sample size — so individual results can shift the averages considerably. Still, the directional picture is clear: this quote is well-positioned.

---

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers assess and price the risk. Here's what's relevant:

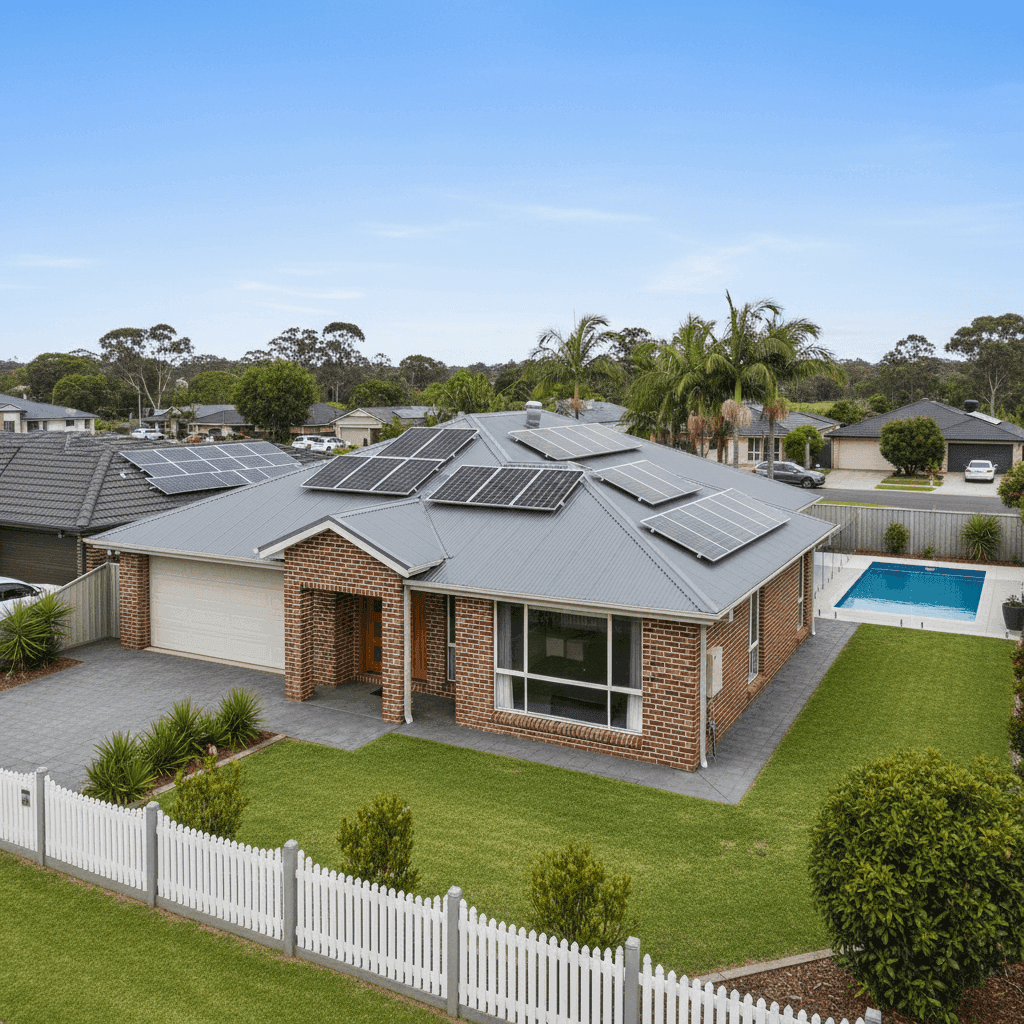

Brick veneer construction with a Colorbond steel roof is generally viewed favourably by insurers. Brick veneer offers solid fire and impact resistance, while Colorbond roofing is durable, lightweight, and performs well in Australian conditions — including heat and moderate wind events. Together, they tend to attract more competitive premiums than, say, weatherboard walls or older tile roofing.

Slab foundation is standard for homes built in this era and region, and poses no unusual risk flags for insurers. Similarly, tile flooring is a practical and durable choice that doesn't negatively affect premium calculations.

Above average fittings quality does push the sum insured higher — and rightly so. Kitchens and bathrooms with quality fixtures, stone benchtops, and premium appliances cost more to repair or replace. The $692,000 building sum insured reflects this, and it's important that figure accurately represents your full rebuild cost (not market value).

The swimming pool adds liability and maintenance considerations, and typically nudges premiums upward slightly. Insurers factor in the risk of accidents and the cost of pool-related damage.

Solar panels are an increasingly common feature and most modern policies cover them as part of the building. However, it's worth confirming with your insurer that your panels and inverter are explicitly included in your policy wording — some older policies may treat them as an optional add-on.

Ducted climate control is another above-average inclusion that contributes to the higher contents and building values, and is worth specifically mentioning when getting quotes to ensure adequate coverage.

The property is not in a cyclone risk zone, which removes one of the more significant premium loading factors that affect homes in northern Queensland and parts of WA.

---

Tips for Homeowners in Wedderburn

1. Review your sum insured regularly. Building costs have risen sharply in recent years. A $692,000 sum insured may have been accurate when the policy was set up, but construction costs in NSW have increased significantly. Use an independent building cost calculator or speak with a quantity surveyor to make sure you're not underinsured.

2. Understand your excess trade-off. The $5,000 building excess on this policy is high. While it lowers your premium, it means smaller claims may not be worth lodging. Consider whether you'd be comfortable absorbing that cost if, say, storm damage occurred. There may be a sweet spot with a lower excess that still keeps your premium competitive.

3. Confirm solar panel and pool coverage. Ask your insurer directly: are the solar panels and inverter covered under the building section? Is the pool — including the pump, filter, and surrounding paving — explicitly included? Getting clarity now avoids nasty surprises at claim time.

4. Compare at renewal, every year. Insurance loyalty rarely pays. Premiums can shift significantly from year to year, and the market is competitive. Even if you're happy with your current cover, it takes only minutes to compare quotes and ensure you're still getting a fair deal.

---

Ready to Compare Your Own Quote?

Whether you're a first-time buyer or a long-term Wedderburn homeowner, it pays to know what the market looks like. CoverClub makes it easy to compare home and contents insurance quotes side by side, so you can see exactly where your premium sits relative to your neighbours. Get a quote today at CoverClub and find out if you're getting the deal you deserve.