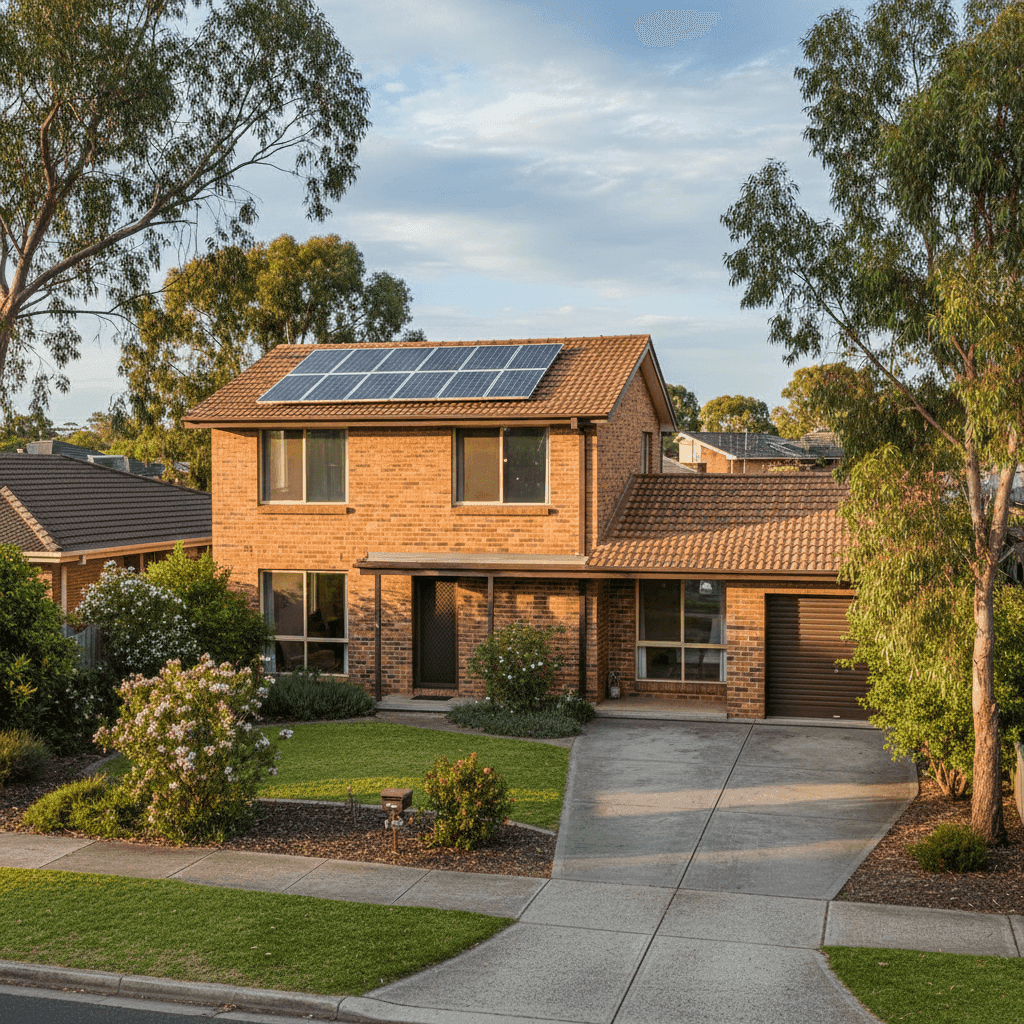

Werribee is one of Melbourne's fastest-growing outer-western suburbs, and with that growth comes an increasing number of homeowners asking a very reasonable question: am I paying too much for home insurance? This article breaks down a real home and contents insurance quote for a four-bedroom, double brick free standing home in Werribee (VIC 3030), and puts the numbers in context so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question sits at $2,228 per year (or $214/month) for combined home and contents cover, with a building sum insured of $952,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — above average for the Werribee suburb. Based on a sample of 125 quotes from the area, the suburb average annual premium is $1,741, and the median sits lower again at $1,554. This quote comes in roughly 28% above the suburb average and nearly 43% above the median — a meaningful gap worth investigating.

That said, "expensive" is relative. The building sum insured of $952,000 is on the higher end, which will naturally push premiums up. A larger insured value means greater liability for the insurer in the event of a total loss, and that cost is passed on through the premium. If your home genuinely costs that much to rebuild from scratch — accounting for demolition, materials, labour, and compliance — then the higher premium may simply reflect the reality of your coverage needs.

---

How Werribee Compares

To put this quote in proper perspective, it helps to zoom out and look at the broader pricing landscape.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,228 |

| Werribee Suburb Average | $1,741 |

| Werribee Suburb Median | $1,554 |

| Werribee 25th Percentile | $1,206 |

| Werribee 75th Percentile | $2,040 |

| Wyndham LGA Average | $1,591 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

A few things stand out here. While this quote is above the local suburb average, it sits below both the Victorian state average and the national median — which is actually a reassuring sign. Homeowners in coastal, flood-prone, or cyclone-affected parts of Australia can face dramatically higher premiums, sometimes multiples of what Werribee residents pay.

Compared to the Wyndham LGA average of $1,591, this quote is noticeably higher, but the LGA figure captures a wide range of property types, sizes, and sum insured values. A larger, well-appointed home with a higher rebuild cost will always skew above the local average.

You can explore more suburb-level data on the Werribee insurance stats page, compare against all of Victoria, or see how your premium stacks up against national benchmarks.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Here's how each one plays into the pricing:

Double Brick Construction Double brick is generally viewed favourably by insurers. It's durable, fire-resistant, and holds up well structurally over time. Compared to timber-framed or clad homes, double brick properties can attract lower premiums — though the rebuild cost per square metre tends to be higher, which may offset some of that benefit.

Tiled Roof Terracotta or concrete tile roofs are considered a lower-risk roofing material compared to older materials like fibro or corrugated iron. They're resilient in most weather conditions and have a long lifespan, both of which insurers tend to reward.

Slab Foundation A concrete slab foundation is standard for homes of this era and construction type. It's generally stable and doesn't carry the same subsidence concerns associated with strip or pier foundations in certain soil types. Werribee's expansive clay soils can be a factor for some properties, so this is worth keeping in mind.

Construction Year: 1979 Homes built in the late 1970s are well past their initial depreciation curve, but they can carry hidden risks — older wiring, plumbing, or roofing materials that may not meet current standards. Insurers often price older homes slightly higher to account for this uncertainty.

Solar Panels This property has solar panels installed, which adds a layer of complexity for insurers. Panels represent an additional asset to cover and can complicate roof-related claims. Some insurers include solar panels under building cover automatically; others require them to be specified. It's worth confirming exactly what your policy covers.

Ducted Climate Control Ducted heating and cooling systems are a significant fixed asset. They're typically covered under building insurance as a permanent fixture, but it's worth checking the policy wording to ensure the system is adequately covered — particularly for mechanical breakdown if that's a feature of your policy.

Timber and Laminate Flooring Flooring type matters for contents and building claims alike. Timber and laminate floors can be costly to repair or replace after water damage events, which is one of the more common home insurance claims. Ensuring your sum insured reflects the cost of replacing these finishes is important.

---

Tips for Homeowners in Werribee

1. Review your building sum insured annually Construction costs in Victoria have risen significantly in recent years. A sum insured that was accurate three years ago may now fall short of what it would actually cost to rebuild your home. Use a building cost calculator or speak to a quantity surveyor to make sure you're not underinsured.

2. Check your solar panel coverage Not all policies treat solar panels the same way. Some cover them under building insurance as a fixture; others exclude them or require a separate endorsement. Given that solar systems can be worth $5,000–$15,000 or more, it's worth a phone call to your insurer to confirm exactly what's covered.

3. Compare quotes before your renewal date Loyalty doesn't always pay in insurance. Premiums can vary significantly between providers for the same property and level of cover. Shopping around — ideally 4–6 weeks before your renewal — gives you time to compare properly without the pressure of a lapsing policy.

4. Consider your excess carefully Both the building and contents excess on this policy are set at $1,000. Opting for a higher excess can reduce your annual premium, which makes sense if you're unlikely to make small claims. Conversely, if you'd struggle to cover a $1,000 excess in an emergency, a lower excess may be worth the extra premium cost.

---

Ready to Compare?

If you're a homeowner in Werribee and want to see whether you could be paying less — or simply want to make sure your current cover stacks up — get a home insurance quote through CoverClub. We compare policies across a range of Australian insurers so you can find the right cover at a price that makes sense for your property.