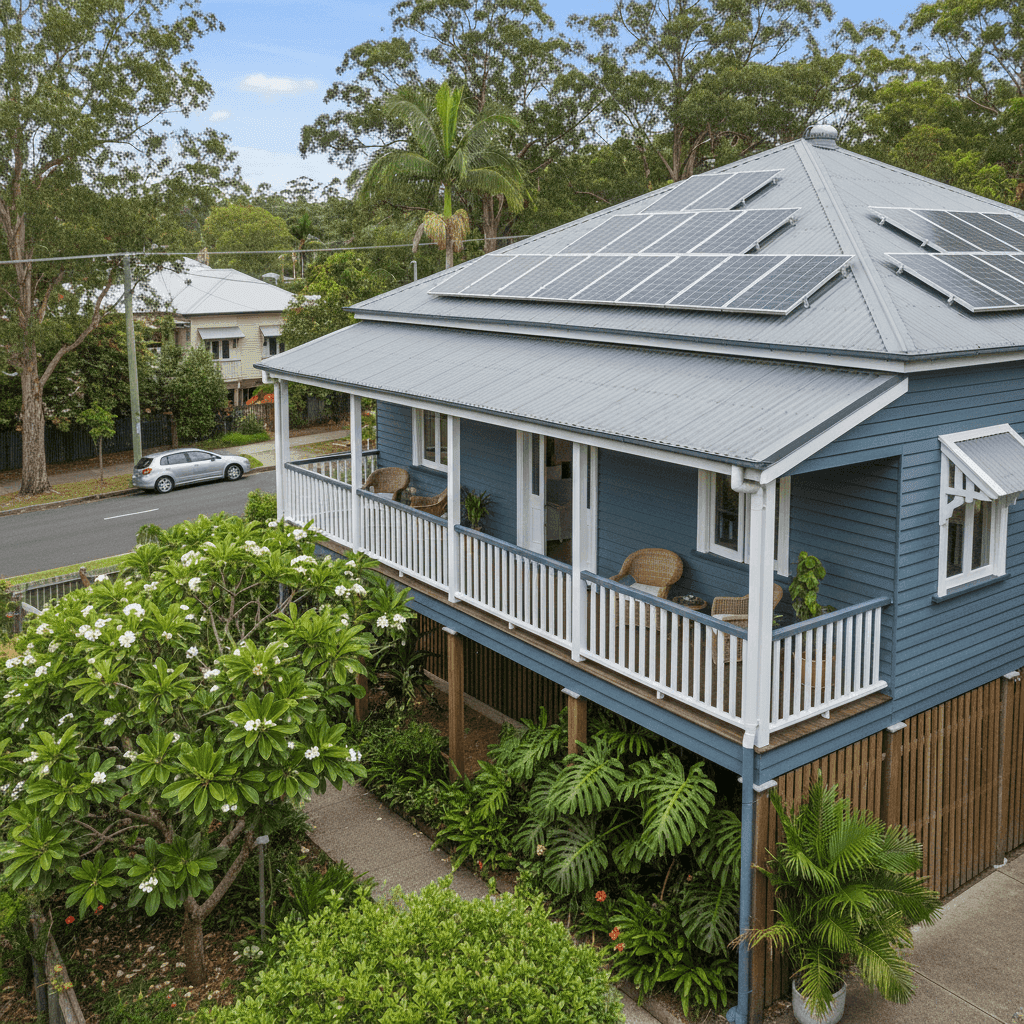

West End is one of Brisbane's most characterful inner-city suburbs — a vibrant, tree-lined pocket of Queensland living just 2 kilometres south of the CBD. It's also a suburb where home insurance premiums can vary enormously, making it all the more important to understand whether the quote sitting in your inbox is genuinely competitive. In this article, we analyse a real home and contents insurance quote for a four-bedroom, two-bathroom free-standing home in West End (QLD 4101) and put it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property came in at $4,089 per year (or $400/month), covering a building sum insured of $678,000 and contents valued at $50,000. Both the building and contents excess are set at $5,000.

Our pricing engine has rated this quote as Fair — Around Average, and the data backs that up.

Compared to the West End suburb average of $6,999/year, this quote sits notably below the mean — a good sign. However, it's worth noting that suburb averages can be heavily skewed by a handful of high-premium outliers. The more telling figure is the suburb median of $3,683/year, which places this quote slightly above the midpoint for the area. In practical terms, roughly half of comparable West End properties are paying less, and half are paying more.

The quote also sits comfortably within the interquartile range — between the 25th percentile ($2,249/yr) and the 75th percentile ($9,914/yr) — suggesting it's neither a bargain nor a red flag. For a 1975-built weatherboard home on stumps with solar panels and ducted climate control, a premium in this range is broadly consistent with what insurers price for this type of property.

The bottom line: this is a reasonable quote, but there may be room to do better with the right comparison.

---

How West End Compares

To appreciate where this quote lands, it helps to zoom out and look at the broader pricing landscape.

| Benchmark | Average | Median |

|---|---|---|

| West End (QLD 4101) | $6,999/yr | $3,683/yr |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

(Based on 31 quotes sampled for the West End suburb. See [QLD insurance stats](https://coverclub.com.au/stats/QLD) and [national stats](https://coverclub.com.au/stats/national) for more.)

A few things stand out here. Queensland's state average of $9,129/year is significantly higher than the national average of $5,347 — a reflection of the elevated natural hazard risk across much of the state, including flooding, storms, and cyclones in northern regions. Brisbane's LGA average is even more striking at $16,277/year, though this figure is heavily influenced by high-value properties and flood-affected postcodes across the broader Brisbane area.

West End itself has a wide spread of premiums — the gap between the 25th and 75th percentile is over $7,600 — which tells you that property-specific factors play a huge role in what you'll actually pay. The suburb's proximity to the Brisbane River means flood risk is a live consideration for many homes in the area, even if the specific property assessed here may not be directly affected.

Explore the full West End insurance data here.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on the insurance premium. Understanding them helps you make sense of the pricing — and know what levers you might have to pull.

Weatherboard Timber Walls

Weatherboard construction is common in older Queensland homes and carries a higher fire risk than brick or rendered masonry. Insurers typically price this in, as timber-framed homes can be more costly to repair or rebuild following fire or storm damage.

Steel / Colorbond Roof

On the upside, a Colorbond steel roof is generally viewed favourably by insurers. It's durable, resistant to ember attack, and less prone to storm damage than older tile or fibrous cement roofing. This can help moderate your premium compared to properties with ageing or fragile roof materials.

Stump Foundation

Homes built on stumps — very characteristic of pre-1980s Queensland architecture — can be more vulnerable to subsidence, pest damage, and movement over time. While this doesn't automatically inflate your premium, it's a factor insurers consider when assessing rebuild risk and structural integrity.

Construction Year: 1975

Older homes often attract higher premiums due to the cost of sourcing period-appropriate materials and the likelihood of outdated wiring, plumbing, or structural elements. A 1975 build is squarely in this category, and the $678,000 building sum insured reflects the genuine cost of rebuilding a home of this age and character.

Solar Panels

Solar panels are an increasingly common inclusion on Queensland homes, and this property has them. Most insurers cover rooftop solar as part of the building, but it's worth confirming this explicitly in your policy — particularly for battery storage systems, which may require separate cover.

Ducted Climate Control

Ducted air conditioning systems are a significant fixed asset and are typically covered under building insurance. Their presence can modestly increase the sum insured required to accurately reflect full rebuild costs.

---

Tips for Homeowners in West End

1. Check your flood cover carefully. West End's proximity to the Brisbane River means flood risk is a real consideration for parts of the suburb. Review whether your policy includes flood cover (not just storm or rainwater damage) and confirm whether your specific address falls within a flood-mapped zone. This can make an enormous difference to both your coverage and your premium.

2. Review your building sum insured annually. Construction costs in South East Queensland have risen sharply in recent years. A sum insured of $678,000 for a 235 sqm weatherboard home may be appropriate today, but it's worth reassessing each year — ideally using a quantity surveyor's estimate or an online rebuild calculator — to ensure you're not underinsured.

3. Consider the impact of your excess. Both the building and contents excess on this policy are set at $5,000. A higher excess typically reduces your premium, but it also means a significant out-of-pocket cost when you claim. Make sure your chosen excess reflects what you could realistically afford in a worst-case scenario.

4. Compare quotes before renewal. Insurance loyalty rarely pays. With a suburb median of $3,683/year and a 25th percentile of $2,249/year, there are clearly more competitive options available in this postcode. Shopping around at renewal — or even mid-policy — could yield meaningful savings without sacrificing cover quality.

---

Compare Your Home Insurance Quote Today

Whether you're reviewing an existing policy or shopping for cover on a new property, understanding the market is the first step to paying a fair price. CoverClub makes it easy to compare home and contents insurance quotes tailored to your property's specific features and location.