West End, QLD 4810 — sitting within the Townsville local government area — is a suburb that carries a distinctive character: older homes, tropical climate, and a risk profile that insurers take seriously. This article analyses a real home and contents insurance quote for a three-bedroom free-standing home in the area, breaks down what's driving the price, and offers practical guidance for homeowners looking to make sense of their premiums.

---

Is This Quote Fair?

The short answer: this quote is rated expensive — sitting noticeably above the local suburb average.

At $8,288 per year (or $794/month), this home and contents policy covers a building sum insured of $661,000 and $50,000 in contents, with a $1,000 excess on both building and contents claims. While that level of coverage is substantial, the premium still warrants scrutiny when placed alongside what other homeowners in the area are paying.

The suburb average premium for West End (4810) sits at $3,629/yr, with a median of $3,428/yr. That means this quote is more than double the typical price being paid in the same postcode. Even the 75th percentile — the upper end of what most locals pay — comes in at just $4,035/yr, still well below this figure.

It's worth noting, however, that the QLD state average is $9,129/yr, which means this quote actually falls below the state average when viewed through that lens. Queensland is one of the most expensive states in Australia for home insurance, largely due to its exposure to cyclones, flooding, and severe weather events. So while the quote is expensive relative to nearby neighbours, it's not out of step with broader Queensland pricing.

---

How West End Compares

Understanding where a premium sits in the broader landscape is key to assessing value. Here's a snapshot:

| Benchmark | Premium |

|---|---|

| This Quote | $8,288/yr |

| West End Suburb Average | $3,629/yr |

| West End Suburb Median | $3,428/yr |

| Townsville LGA Average | $7,340/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. The Townsville LGA average of $7,340/yr is the most relevant regional benchmark, and this quote of $8,288/yr sits moderately above it — suggesting the specific property features are pushing costs higher than even the typical Townsville home. Meanwhile, the national average of $5,347/yr and median of $2,764/yr reinforce just how elevated insurance costs are in cyclone-prone parts of Queensland compared to the rest of the country.

You can explore how Queensland compares to other states in more detail — the data tells a compelling story about the weight of natural hazard risk on premiums across the state.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to the elevated premium. Understanding them can help homeowners make informed decisions.

Cyclone Risk Area

This is arguably the single biggest factor. West End falls within a designated cyclone risk zone, and insurers price this risk heavily. North Queensland properties face a statistically higher likelihood of wind, storm surge, and associated damage — and that exposure is baked directly into the premium calculation.

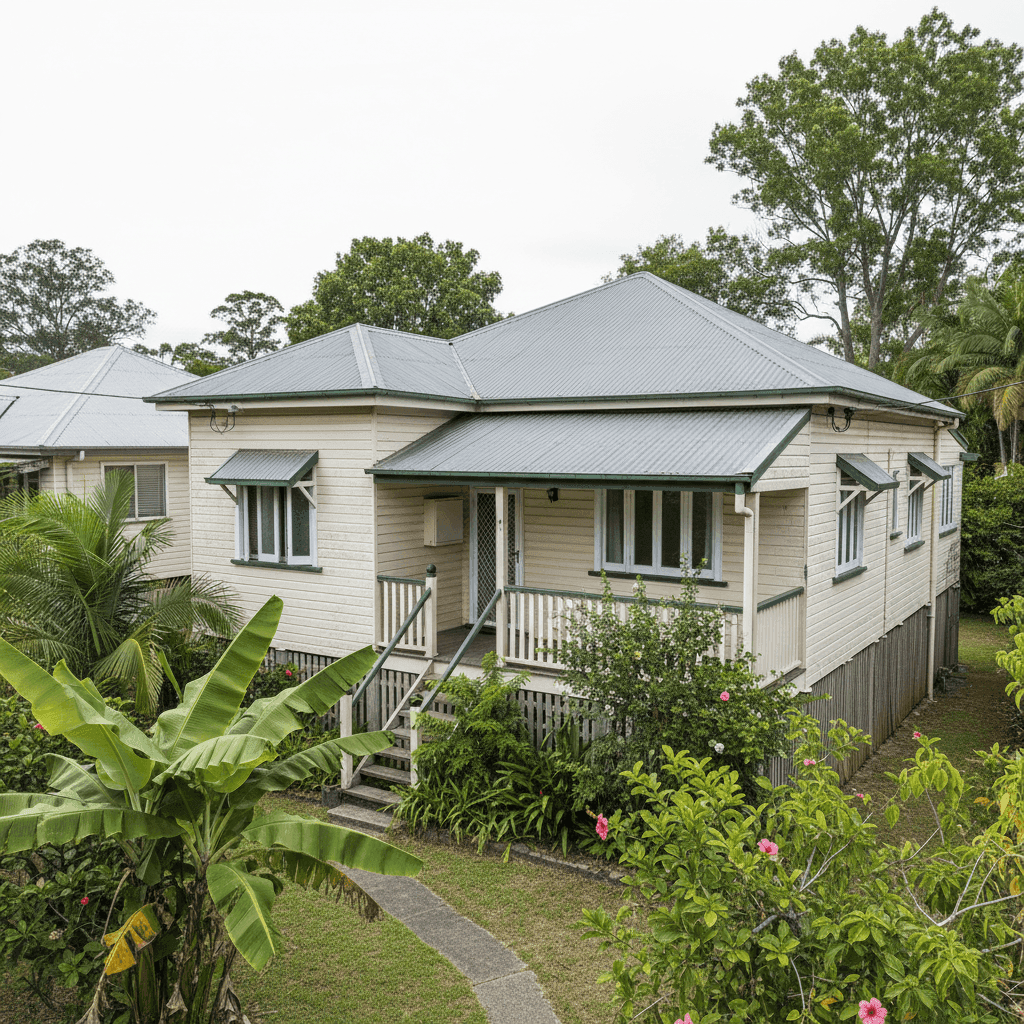

Fibro Asbestos External Walls

The home's external walls are constructed from fibro asbestos, a material common in pre-1980s Australian homes. Insurers view this as a higher-risk construction type for several reasons: asbestos-containing materials require specialist handling during repairs, which significantly increases claim costs. Some insurers may also apply loadings or exclusions specifically related to asbestos remediation.

Construction Year: 1930

At nearly 100 years old, this home predates modern building codes and cyclone-resilient construction standards. Older homes are statistically more vulnerable to storm damage, and replacement or repair costs can be harder to estimate — both of which push premiums upward.

Stump Foundation

Homes built on timber stumps — as is typical of this era in Queensland — can be more susceptible to movement, subsidence, and termite damage over time. Insurers factor foundation type into their risk assessments, and stumped homes may attract higher premiums than slab-on-ground alternatives.

Colorbond Steel Roof

On a more positive note, the steel/Colorbond roof is generally regarded as a durable, cyclone-resilient roofing material. It performs well in high-wind events compared to tiles, which can become dangerous projectiles in severe storms. This may offer a modest offset to some of the other risk factors.

Building Sum Insured: $661,000

The sum insured is substantial for a 130 sqm home, but it's important to remember that building insurance covers replacement cost, not market value. In a cyclone-risk area with asbestos walls and heritage construction, rebuilding costs per square metre can be considerably higher than a modern equivalent — particularly when factoring in asbestos removal, specialist trades, and compliance with current building codes.

---

Tips for Homeowners in West End

1. Shop around — seriously. With a premium more than double the suburb median, there is meaningful room to explore alternatives. Different insurers model cyclone and construction risk differently, and the spread between quotes in high-risk areas can be significant. Use a comparison tool like CoverClub to see multiple quotes side by side before committing.

2. Review your sum insured carefully. Over-insuring a property inflates your premium without providing additional benefit — insurers will only pay up to the actual cost of rebuilding. Consider getting a professional building replacement cost assessment to ensure your sum insured is accurate rather than estimated.

3. Ask about cyclone mitigation discounts. Some insurers offer reduced premiums for homes with cyclone-rated upgrades — things like storm shutters, reinforced roofing fixings, or cyclone straps on the roof frame. If you've made any improvements to the home's wind resistance, make sure your insurer knows about them.

4. Understand your asbestos position. If your home contains asbestos-containing materials, clarify exactly what your policy covers in the event of a claim. Some policies have specific conditions or sub-limits around asbestos removal and reinstatement. Knowing this upfront avoids nasty surprises at claim time.

---

Find a Better Deal with CoverClub

Whether you're a first-time buyer in West End or a long-term homeowner questioning your renewal price, comparing quotes is the smartest first step. CoverClub makes it easy to see what the market is offering for your specific property — in one place, without the runaround. Get a home insurance quote today and find out if you're paying more than you need to.