West Pennant Hills is one of Sydney's leafy, well-established suburbs in the Hills District — and if you own a free standing home here, you already know that protecting it is no small consideration. This article breaks down a real home and contents insurance quote for a five-bedroom property in the area, compares it against suburb, state, and national benchmarks, and offers practical guidance for homeowners looking to get the best value on their cover.

---

Is This Quote Fair?

The quote in question comes in at $2,208 per year (or roughly $216 per month) for combined home and contents insurance, covering a building sum insured of $1,000,000 and contents valued at $50,000. Both the building and contents excess are set at $5,000.

Our pricing analysis rates this quote as FAIR — Around Average, which is a reasonable outcome for a property of this size and specification. It sits comfortably within the typical range seen across the suburb, neither a standout bargain nor an overpriced outlier.

To put this in context:

- The suburb average for West Pennant Hills (2125) is $2,467/yr, so this quote is roughly $259 below average — a meaningful saving.

- The suburb median sits at $2,006/yr, meaning this quote is slightly above the midpoint of what locals are paying.

- The suburb's interquartile range runs from $1,687/yr (25th percentile) to $2,400/yr (75th percentile), placing this quote just above the upper quartile.

In short, the quote is competitive relative to the suburb average but does sit on the higher side of the median range. Whether it represents good value depends on the breadth of cover and any optional extras included in the policy.

---

How West Pennant Hills Compares

One of the most striking takeaways from the data is just how much cheaper West Pennant Hills is compared to broader NSW benchmarks. You can explore the full picture on the West Pennant Hills insurance stats page.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| West Pennant Hills (2125) | $2,467/yr | $2,006/yr |

| Hornsby LGA | $3,958/yr | — |

| NSW State | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

The NSW state average of $9,528/yr is dramatically higher than what West Pennant Hills homeowners typically pay — though it's worth noting that NSW averages are heavily skewed by high-risk flood and coastal areas. The median of $3,770/yr is a more representative figure, and West Pennant Hills still comes in well below it.

Even against the national median of $2,764/yr, this suburb holds its own. Homeowners in West Pennant Hills benefit from relatively low natural disaster risk — no cyclone exposure, limited flood risk in most parts of the suburb — which keeps premiums more manageable than in many other parts of the country.

The Hornsby LGA average of $3,958/yr is notably higher than the suburb-level data, suggesting that some neighbouring areas within the same local government zone carry more risk or have higher property values that push premiums up.

---

Property Features That Affect Your Premium

Every insurer assesses risk based on the specific characteristics of a property. Here's how the features of this home are likely influencing the premium:

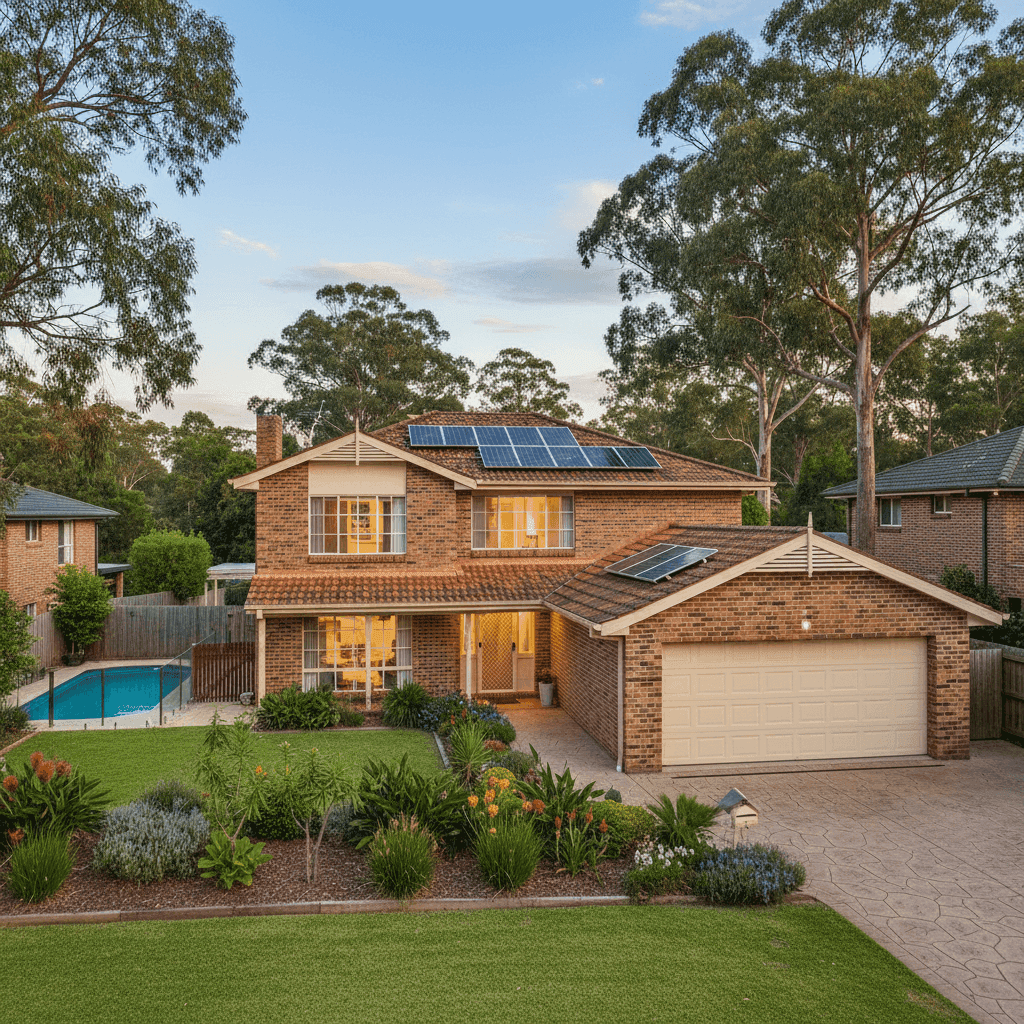

Brick veneer construction with a tiled roof is generally viewed favourably by insurers. Brick veneer offers solid fire resistance and structural durability, while tiled roofs are considered more resilient than corrugated iron in many weather scenarios. Together, these materials typically attract lower premiums compared to timber-framed or Colorbond alternatives.

Slab foundation is standard for homes built in this era and region, and doesn't introduce the subsidence or moisture concerns sometimes associated with older stumped or suspended floors.

Built in 2000, the property is relatively modern — old enough to have some wear but young enough to avoid the significant compliance and structural concerns that can affect pre-1980s homes. This is generally a neutral-to-positive factor for insurers.

Swimming pool adds replacement cost to the building sum insured and can introduce liability considerations, particularly if fencing or safety compliance is a factor. Insurers may factor this into their risk assessment, though it's rarely a major premium driver on its own.

Solar panels are an increasingly common feature and most insurers now include them under building cover, though it's worth confirming this explicitly with your provider. Panels add to the replacement value of the home and can affect rebuild cost calculations.

Ducted climate control is another high-value fixture that contributes to the overall rebuild cost. A full ducted system can cost tens of thousands of dollars to replace, so it's important that your building sum insured accounts for it — which a $1,000,000 sum insured on a 235 sqm home should comfortably do.

Contents valued at $50,000 is on the modest side for a five-bedroom, three-bathroom home with standard fittings. It's worth reviewing whether this figure adequately covers furniture, appliances, clothing, electronics, and other belongings — especially in a larger family home.

---

Tips for Homeowners in West Pennant Hills

1. Review your contents sum insured carefully $50,000 in contents cover spread across five bedrooms and three bathrooms may leave you underinsured. Walk through each room and tally up the replacement cost of your belongings — many homeowners are surprised by how quickly the total climbs. Most insurers allow you to adjust this figure easily.

2. Confirm solar panels and pool equipment are covered Ask your insurer specifically whether solar panels are included under your building cover and whether pool equipment (pumps, filters, heating systems) is covered. These are often included but the specifics can vary between policies.

3. Consider whether your $5,000 excess is right for you A higher excess generally reduces your premium, but $5,000 is a significant out-of-pocket amount at claim time. If you'd struggle to cover that in an emergency, it may be worth comparing quotes with a lower excess to find the right balance between upfront savings and financial comfort.

4. Compare quotes before your renewal date Even a "fair" quote can be beaten. Insurers adjust their pricing regularly, and loyalty doesn't always pay — in fact, long-term customers are sometimes charged more than new ones. Set a reminder to compare at least 30 days before your policy renews.

---

Ready to Compare?

Whether you're assessing a new quote or approaching your annual renewal, it pays to see what else is on the market. Get a home insurance quote through CoverClub to compare options tailored to your property in West Pennant Hills and find cover that genuinely fits your needs and budget.