White Sands is a quiet residential locality in South Australia's Mid Murray region, sitting along the banks of Lake Alexandrina. It's the kind of place where properties tend to be well-built family homes — and insuring them properly matters. This article takes a close look at a real home and contents insurance quote for a four-bedroom, two-bathroom free standing home in White Sands (SA 5253), breaking down whether the premium is reasonable and what factors are likely driving the cost.

---

Is This Quote Fair?

The annual premium for this property came in at $4,011 per year (or $384/month), covering both building (sum insured: $734,000) and contents ($100,000), each with a $500 excess.

Our pricing analysis rates this quote as EXPENSIVE — above average for the area. That's a meaningful signal worth unpacking.

To put it in context:

- The [SA state average](https://coverclub.com.au/stats/SA) for home insurance is $2,433/yr, and the median sits at $1,679/yr

- The [national average](https://coverclub.com.au/stats/national) is $5,347/yr, with a national median of $2,764/yr

- The Mid Murray LGA average is just $1,547/yr

So while this quote is well below the national average, it's running significantly higher than both the SA state average and the local LGA benchmark. Against the Mid Murray LGA average of $1,547/yr, this premium is roughly 2.6 times more expensive — a gap that deserves closer examination.

It's worth noting that sum insured levels play a large role here. A building insured for $734,000 is on the higher end for the region, and contents cover of $100,000 adds meaningfully to the total. That said, even accounting for higher coverage limits, there's likely room to find a more competitive rate by shopping around.

---

How White Sands Compares

Without suburb-level data available for White Sands specifically, we can use the broader regional and state figures to frame this quote.

| Benchmark | Premium |

|---|---|

| This quote | $4,011/yr |

| Mid Murray LGA average | $1,547/yr |

| SA state average | $2,433/yr |

| SA state median | $1,679/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

The quote sits above every South Australian benchmark but below the national average — suggesting that while this isn't the most expensive policy in the country, homeowners in White Sands may still be paying more than necessary relative to their local market.

One factor to keep in mind: White Sands is not classified as a cyclone risk area, which typically helps keep premiums lower compared to properties in northern or coastal Queensland. The relatively benign risk profile of the region makes the above-average premium even more worth questioning.

For a deeper look at how premiums across South Australia compare, or to see national trends, CoverClub's stats pages offer useful context.

---

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers calculate risk — and therefore price.

Construction Materials

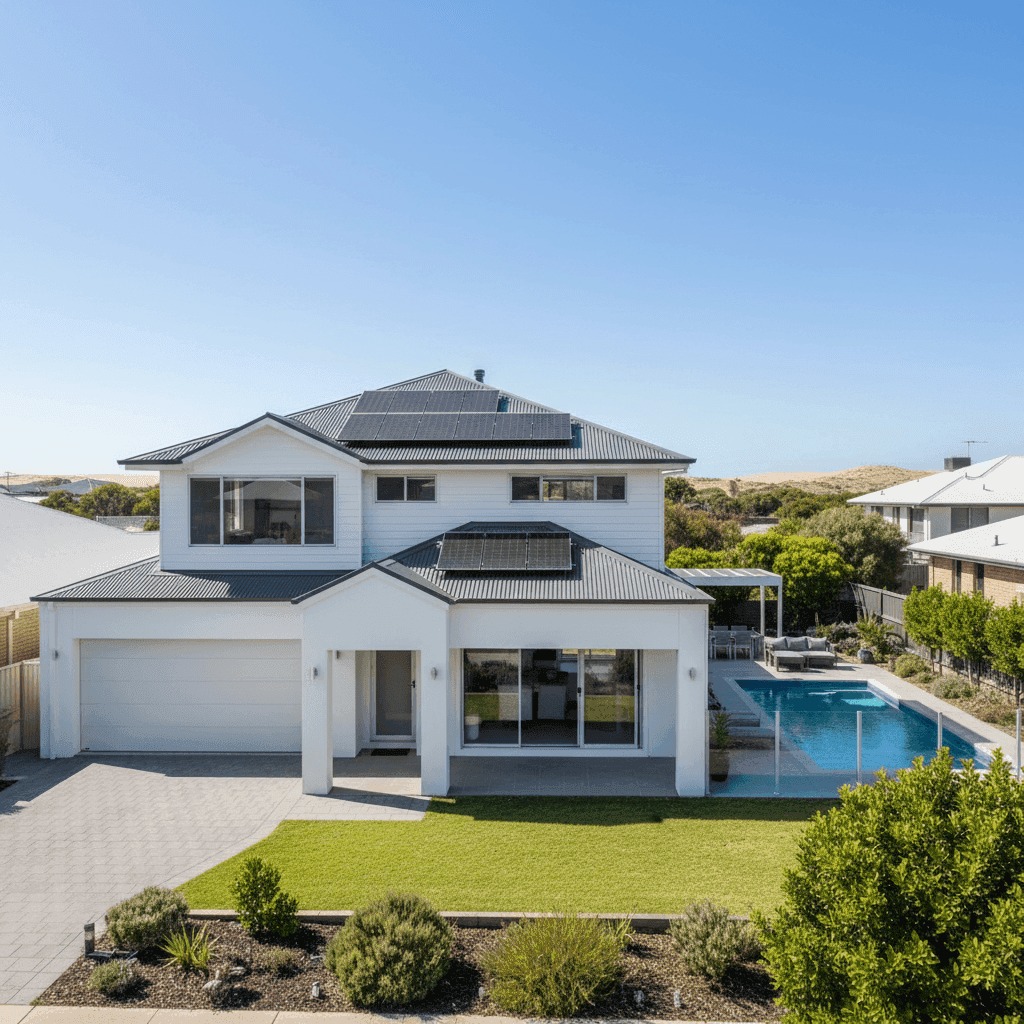

The home features Hardiplank/Hardiflex external walls and a steel/Colorbond roof. Both are generally viewed favourably by insurers. Colorbond roofing is durable, fire-resistant, and low-maintenance, while fibre cement cladding like Hardiflex is non-combustible and resistant to rot and termites. These materials can work in your favour when it comes to pricing.

Slab Foundation

A concrete slab foundation is typically considered a stable, lower-risk base compared to raised stumped or pier foundations. It reduces the likelihood of subsidence-related claims and is generally preferred by underwriters.

Timber and Laminate Flooring

Timber and laminate flooring can be a double-edged sword for insurers. While aesthetically appealing, these materials can be more costly to replace after water damage or flooding than tiles or vinyl. This may contribute marginally to the contents or building replacement cost.

Swimming Pool

Having a pool on the property adds to the replacement cost of the home and can introduce additional liability considerations. Pool fencing compliance, pump equipment, and tiling all factor into building sum insured calculations.

Solar Panels

Solar panels are increasingly common in SA, but they do add to the insured value of the home. Many policies now include solar panels under building cover automatically, though it's worth confirming this with your insurer. Panels on a Colorbond roof are generally straightforward to insure.

Ducted Climate Control

A ducted climate control system is a significant fixed asset within the home. As a built-in system, it typically falls under building cover and contributes to the overall replacement cost — which at $734,000 for this property is already on the higher side.

Property Size

At 235 square metres, this is a substantial family home. Larger floor areas mean higher rebuild costs, which directly influences the building sum insured and, in turn, the premium.

---

Tips for Homeowners in White Sands

If you're a homeowner in White Sands — or anywhere in the Mid Murray region — here are some practical ways to make sure you're getting value from your home insurance.

1. Review Your Sum Insured Carefully

A building sum insured of $734,000 is significant. Make sure this figure reflects the actual cost to rebuild your home (not its market value), including demolition, site clearance, and professional fees. Overinsuring can drive up your premium unnecessarily, while underinsuring leaves you exposed. Use a building cost calculator or consult a quantity surveyor if you're unsure.

2. Compare Multiple Quotes

This is the single most effective way to reduce your premium. Insurers price risk differently, and the same property can attract wildly different quotes depending on the provider. Use CoverClub to compare quotes side by side and find a policy that matches your needs at a fairer price.

3. Consider Your Excess Level

Both the building and contents excess on this policy sit at $500 — a fairly standard level. Opting for a higher excess (say, $1,000 or $2,000) can meaningfully reduce your annual premium. Just make sure you're comfortable covering that amount out of pocket in the event of a claim.

4. Check What's Actually Covered

With a pool, solar panels, and ducted air conditioning, it's important to confirm that all of these features are explicitly included in your policy. Some insurers exclude or limit cover for certain fixed assets, and finding out at claim time is a costly surprise. Read the Product Disclosure Statement (PDS) carefully before committing.

---

Ready to Find a Better Deal?

Whether you're renewing an existing policy or insuring a new property, it pays to compare. CoverClub makes it easy to see what home and contents insurance actually costs for properties like yours in White Sands and across South Australia. Get a quote today and find out if you could be paying less for the same level of protection.