If you own a free standing home in Whyalla, SA 5600, you're probably wondering whether the home insurance quote sitting in your inbox is a fair deal — or whether you're leaving money on the table. This article breaks down a real quote for a 3-bedroom, 1-bathroom property in Whyalla, comparing it against local, state, and national benchmarks so you can make a genuinely informed decision.

---

Is This Quote Fair?

The quote in question comes in at $2,077 per year (or $199/month) for combined Home and Contents cover, with a building sum insured of $497,000 and contents valued at $50,000. Both the building and contents excess are set at $500.

Our price rating for this quote is Expensive — above average for the Whyalla area.

To put that in perspective: the suburb average premium for Whyalla sits at just $1,546/year, and the median is $1,624/year. This quote lands well above both figures, and even exceeds the 75th percentile of $1,861/year — meaning it's pricier than at least three-quarters of comparable quotes we've seen for this postcode.

That said, "expensive" doesn't automatically mean "wrong." The sum insured of $497,000 is a significant figure, and the inclusion of contents cover, solar panels, and ducted climate control all contribute to a higher premium. Still, the gap between this quote and the suburb median is substantial enough to warrant shopping around.

---

How Whyalla Compares

Understanding where Whyalla sits in the broader insurance landscape is useful context. Here's a snapshot:

| Benchmark | Premium |

|---|---|

| This Quote | $2,077/yr |

| Whyalla Suburb Average | $1,546/yr |

| Whyalla Suburb Median | $1,624/yr |

| Whyalla 25th Percentile | $1,172/yr |

| Whyalla 75th Percentile | $1,861/yr |

| SA State Average | $2,433/yr |

| SA State Median | $1,679/yr |

| Unincorporated SA LGA Average | $1,823/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

(Based on 38 quotes sampled for the Whyalla postcode.)

A few things stand out here. First, Whyalla is actually a relatively affordable area to insure compared to the rest of South Australia and the country as a whole. The SA state average sits at $2,433/year, while the national average is a striking $5,347/year — largely driven by high-risk coastal and cyclone-prone regions. Whyalla, by contrast, benefits from not being classified as a cyclone risk area, which keeps premiums more manageable across the board.

The suburb-level data for Whyalla shows a median of $1,624/year, suggesting that most homeowners in this postcode are paying noticeably less than the quote under review. If your current renewal notice looks similar to this figure, it may be worth getting a second (or third) opinion.

---

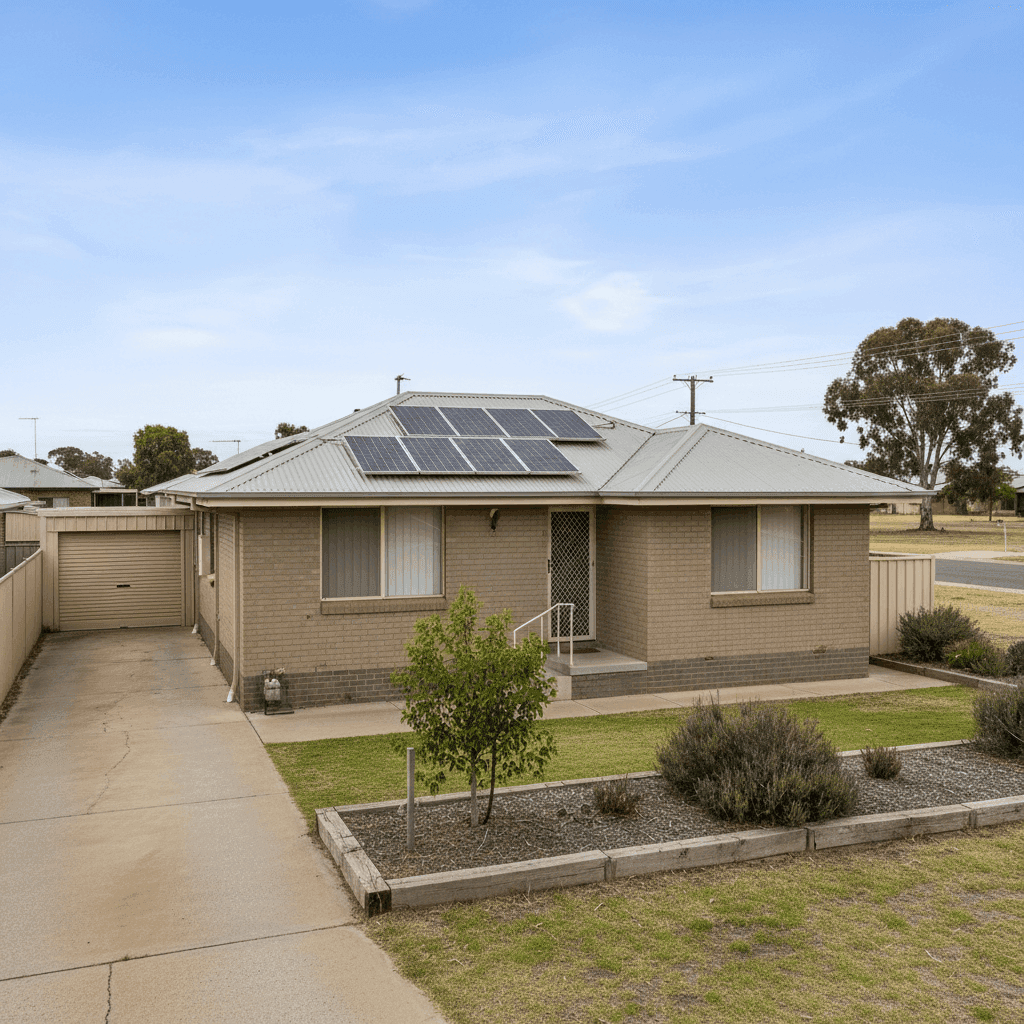

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium quoted. Here's how each one factors in:

Double Brick Construction Double brick walls are generally viewed favourably by insurers. They offer strong resistance to fire and impact, which can help moderate premiums compared to timber-framed or clad homes. This is a genuine asset for the property.

Steel/Colorbond Roof Colorbond roofing is another positive signal for insurers. It's durable, fire-resistant, and performs well in extreme heat — all relevant considerations for regional South Australia. Compared to older terracotta or asbestos-cement roofs, Colorbond tends to attract lower risk ratings.

Construction Year: 1969 At over 55 years old, the home falls into an age bracket that can attract slightly higher scrutiny from insurers. Older homes may have ageing plumbing, electrical wiring, or structural elements that increase the likelihood of a claim. However, a slab foundation and double brick construction help offset some of this concern.

Solar Panels Solar panels are increasingly common on Australian rooftops, but they do add to the replacement cost of a home and can complicate roof-related claims. Insurers typically factor these into the building sum insured, which may contribute to a higher premium.

Ducted Climate Control Ducted systems represent a meaningful capital investment. If damaged or destroyed, they're expensive to replace, and this is reflected in the building sum insured and, by extension, the premium.

Timber/Laminate Flooring Flooring type can influence contents and building claims, particularly in the event of water damage. Timber and laminate floors are susceptible to warping from leaks, which is worth keeping in mind when reviewing your excess and policy inclusions.

No Pool, No Cyclone Risk The absence of a pool removes a common liability and maintenance concern for insurers. And as noted, Whyalla is not classified as a cyclone risk area — a significant factor that keeps premiums lower than many coastal Queensland or WA properties.

---

Tips for Homeowners in Whyalla

1. Compare at least three quotes before renewing Given that this quote sits above the 75th percentile for Whyalla, there's a reasonable chance you could find comparable cover at a lower price. Use a comparison service like CoverClub to benchmark your options quickly without committing to anything.

2. Review your building sum insured carefully At $497,000, the building sum insured is a substantial figure for a 130 sqm home in Whyalla. It's worth getting an independent building replacement cost estimate to ensure you're not over-insured — paying premiums on a sum that exceeds what it would actually cost to rebuild. Equally, being under-insured carries serious risk, so accuracy matters in both directions.

3. Ask about discounts for home security and safety features Many insurers offer discounts for properties with deadbolts, monitored alarms, or smoke detectors. If your home has any of these features and they haven't been declared, you may be missing out on a reduction.

4. Consider a higher excess to reduce your annual premium If you're financially comfortable absorbing a larger out-of-pocket cost in the event of a claim, increasing your excess from $500 to $1,000 or more can meaningfully reduce your annual premium. Just make sure the saving justifies the added exposure.

---

Ready to Find a Better Deal?

Whether you're renewing your existing policy or shopping for the first time, comparing quotes is the single most effective way to make sure you're not overpaying. Head to CoverClub to enter your property details and see how your current premium stacks up against the market — it takes just a few minutes and could save you hundreds of dollars a year.