Home insurance costs can vary enormously depending on where you live, what your home is made of, and how much cover you need. To illustrate what homeowners in regional New South Wales might expect to pay, we've analysed a real home and contents insurance quote for a four-bedroom free standing home in Winton, NSW 2344 — a quiet locality in the Tamworth Regional Council area. Here's what the numbers tell us, and what they mean for you.

---

Is This Quote Fair?

The annual premium for this property came in at $5,950 per year (or $563/month), covering both building and contents with a building sum insured of $1,305,000 and contents valued at $300,000. Both the building and contents excess are set at $1,000.

Our pricing analysis rates this quote as CHEAP — below average — which is good news for the homeowner. To put that in context:

- The NSW state average premium is $9,528/yr

- The national average is $5,347/yr

- The NSW state median is $3,770/yr

- The national median is $2,764/yr

At $5,950/yr, this quote sits well below the NSW state average, and only slightly above the national average — a strong result for a property of this size and age. Given the relatively high building sum insured of $1.3 million, the premium represents solid value. Homeowners in regional NSW often face elevated premiums due to factors like limited insurer competition and exposure to weather events, so securing a below-average rate here is a meaningful win.

---

How Winton Compares

Suburb-level pricing data for Winton (2344) is limited, but we can benchmark this quote against the broader Tamworth LGA average of $4,038/yr and the wider NSW state figures.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $5,950 |

| Tamworth LGA Average | $4,038 |

| NSW State Average | $9,528 |

| NSW State Median | $3,770 |

| National Average | $5,347 |

| National Median | $2,764 |

The quote is higher than the Tamworth LGA average, which makes sense — this property carries a significantly higher building sum insured and contents value than many homes in the region. When you adjust for the level of cover, the per-dollar-of-coverage rate is quite competitive. Compared to the national picture, the premium is only marginally above the national average despite covering a large, older regional home with a high rebuild value.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence what insurers charge. Understanding these factors can help you make sense of your quote — and potentially negotiate a better one.

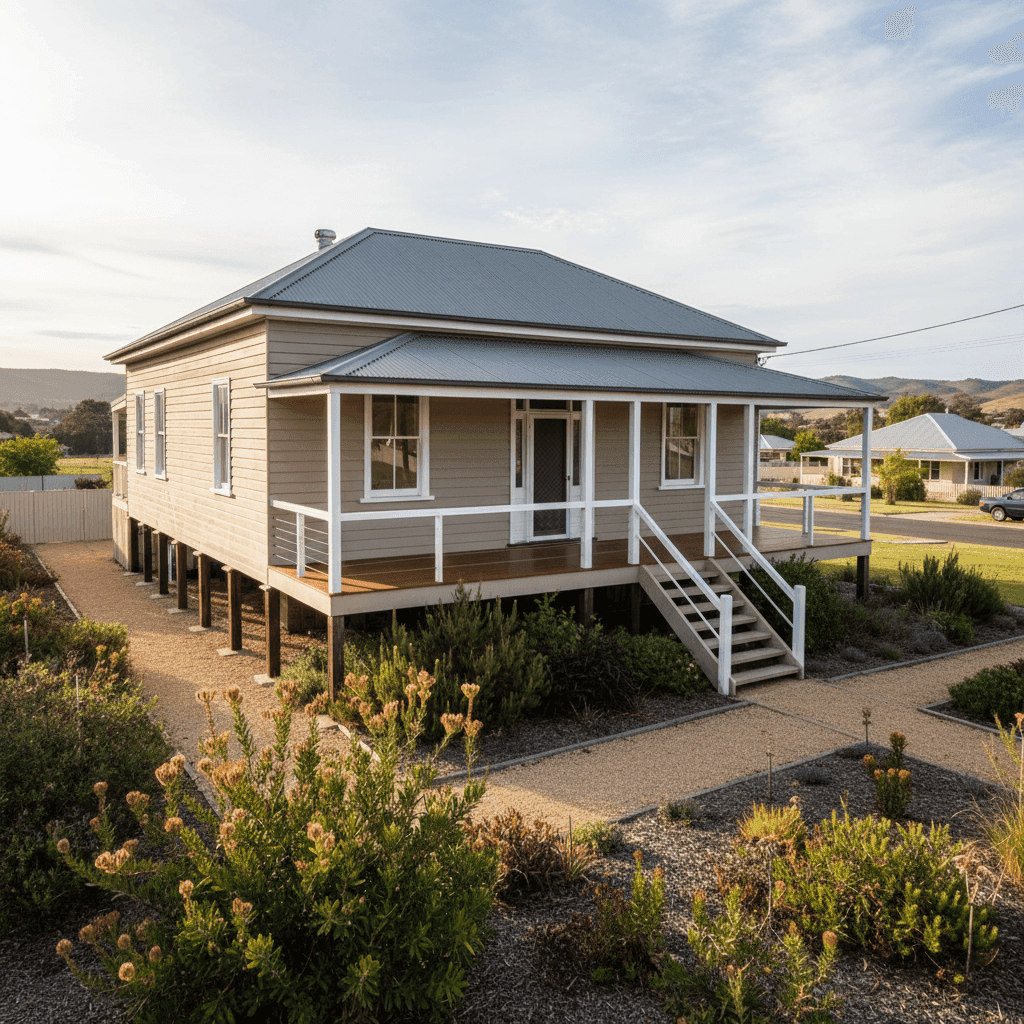

Weatherboard Timber Walls

Weatherboard wood external walls are one of the most significant premium drivers for older Australian homes. Timber is considered a higher fire risk than brick or rendered masonry, and it can be more costly to repair or replace after storm or impact damage. Insurers typically apply a loading to timber-clad homes, particularly those built before modern building codes came into effect.

Steel/Colorbond Roof

On the positive side, a steel Colorbond roof is generally viewed favourably by insurers. It's durable, fire-resistant, and performs well in high-wind conditions compared to terracotta tiles or older corrugated iron. This may help offset some of the premium loading from the timber walls.

Stump Foundation

Built in 1950, this home sits on stumps — a common foundation type for older Queensland-style and rural NSW homes. While stumps allow good ventilation and are well-suited to certain soil types, they can be susceptible to movement, pest damage, and moisture issues over time. Insurers may factor this in when assessing structural risk.

Timber and Laminate Flooring

Timber and laminate floors are attractive but can be costly to repair or replace after water damage or flooding. This is worth keeping in mind when reviewing your contents and building policy inclusions — particularly around water damage and escape of liquid cover.

Construction Year: 1950

The age of the home is a notable factor. Pre-1960s construction predates many modern building standards, including those related to fire separation, structural bracing, and electrical wiring. Older homes can cost more to repair to a comparable standard, which is partly why the building sum insured here is set at $1,305,000 — reflecting the true cost of rebuilding a home of this character and size (235 sqm) in today's market.

Ducted Climate Control

The presence of ducted climate control adds to the insured value of the building. These systems can be expensive to repair or replace, and their inclusion in the sum insured is appropriate and prudent.

---

Tips for Homeowners in Winton

Whether you're reviewing an existing policy or shopping for new cover, here are four practical steps worth considering.

1. Review your building sum insured annually Construction costs in regional NSW have risen sharply in recent years. A sum insured that was accurate two years ago may no longer reflect the true cost of rebuilding your home. Use an independent building calculator or ask your insurer to reassess — underinsurance is one of the most common and costly mistakes homeowners make.

2. Ask about discounts for security and safety features Many insurers offer discounts for homes with monitored alarm systems, deadbolt locks, or smoke detectors. If you've made any upgrades since your last renewal, make sure your insurer knows — it could reduce your premium.

3. Consider your excess carefully This policy carries a $1,000 excess on both building and contents. Opting for a higher excess (say, $2,500) can meaningfully reduce your annual premium, but only makes sense if you have the cash reserves to cover it in the event of a claim. Conversely, a lower excess means more predictable out-of-pocket costs.

4. Compare quotes before each renewal Loyalty doesn't always pay in insurance. Insurers frequently offer better rates to new customers than to existing ones. Using a comparison platform like CoverClub before your renewal date takes only a few minutes and could save you hundreds of dollars — particularly given the wide spread between the Tamworth LGA average and the NSW state average.

---

Get a Better Deal on Home Insurance

Whether you think your current premium is fair or you're not sure where to start, comparing quotes is the single most effective way to ensure you're getting value for money. At CoverClub, we make it easy to see what multiple insurers would charge for your specific property — no obligation, no hidden fees.