Wolffdene is a semi-rural suburb tucked into the northern Gold Coast hinterland, known for its spacious blocks, leafy surrounds, and a relaxed lifestyle that sits somewhere between acreage living and suburban convenience. For homeowners in this pocket of Queensland, protecting a substantial family home comes with a price tag that reflects both the property's size and the broader insurance landscape of South East Queensland.

This article breaks down a recent home and contents insurance quote for a five-bedroom, three-bathroom free-standing home in Wolffdene (postcode 4207), helping you understand what's driving the premium and how it stacks up against local, state, and national benchmarks.

---

Is This Quote Fair?

The quoted annual premium of $6,996 (or approximately $686 per month) has been rated Fair — Around Average, and the numbers back that up.

Looking at suburb-level data for Wolffdene (QLD 4207), the average premium in this postcode sits at $6,795 per year, with a median of $6,318. The quoted figure lands just above both of those marks, and comfortably within the interquartile range — the 25th percentile is $5,859 and the 75th percentile is $7,110. In other words, this quote is neither a bargain nor an outlier; it's squarely in the middle of what Wolffdene homeowners are paying.

It's worth noting that the sample size for this suburb is relatively small (10 quotes), so the data should be interpreted with some caution. That said, the consistency of the figures suggests a reasonably reliable picture of local pricing.

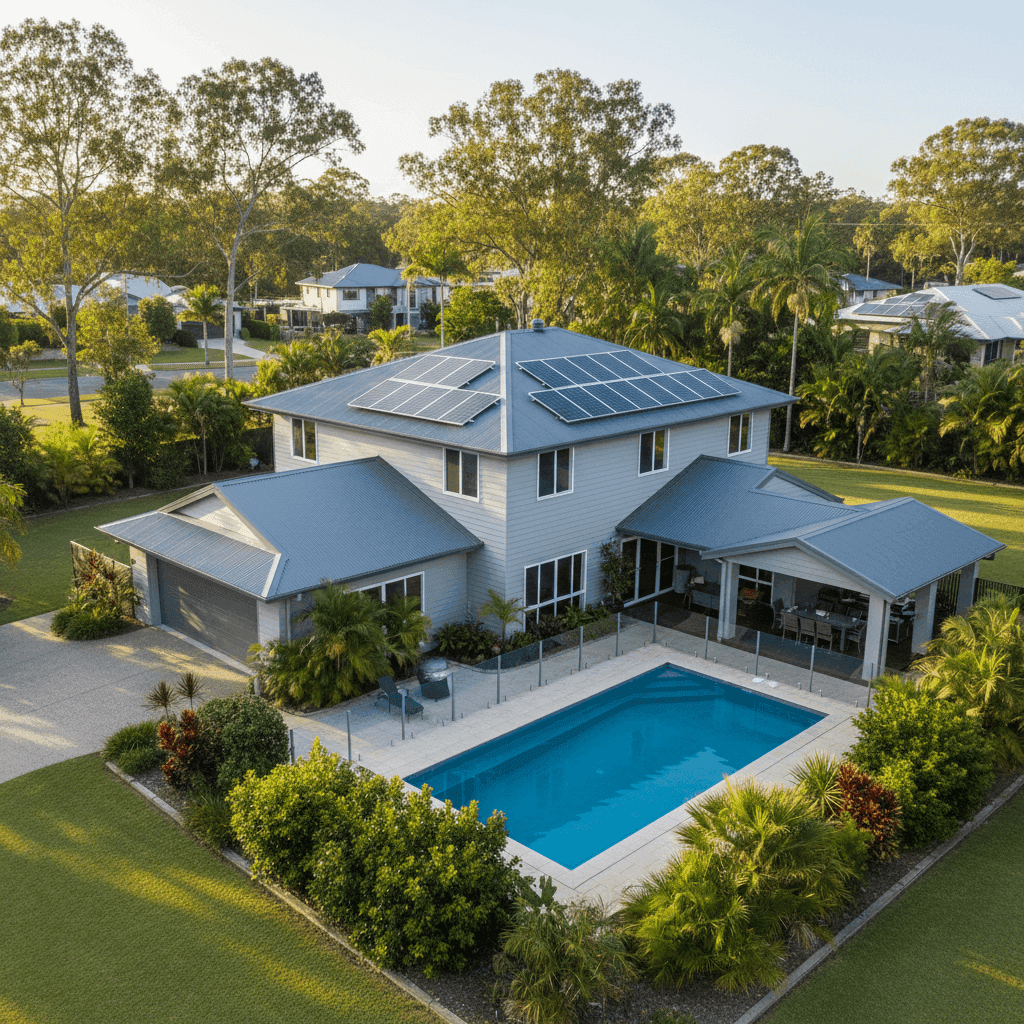

The building sum insured of $1,182,000 and contents cover of $140,000 are meaningful factors here. A five-bedroom home of 286 sqm built in 1983 with quality fittings and extras like a pool, solar panels, and ducted climate control will naturally attract a higher rebuild cost than a smaller, more modest property — and insurers price accordingly.

---

How Wolffdene Compares

The premium becomes more striking when you zoom out to the state and national level.

| Benchmark | Average Premium |

|---|---|

| Wolffdene (4207) | $6,795 / yr |

| Gold Coast LGA | $5,494 / yr |

| Queensland | $4,547 / yr |

| National | $2,965 / yr |

Wolffdene sits 54% above the Queensland average and more than double the national average. Even within the Gold Coast LGA, this suburb's premiums run notably higher — around 24% above the LGA average of $5,494.

This isn't unusual for South East Queensland. The Queensland state insurance data consistently shows that premiums across the Sunshine State are well above national averages, driven by elevated weather risk, higher rebuild costs, and the sheer scale of insured values in the region. Wolffdene, while not in a designated cyclone risk zone, still sits in a subtropical climate corridor where storm events, heavy rainfall, and flooding can be significant concerns.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge:

Age and construction (built 1983) Homes built in the early 1980s predate many modern building codes, which can mean older electrical systems, plumbing, and structural elements that are costlier to repair or replace. Insurers factor in the increased likelihood of maintenance-related claims on older properties.

Hardiplank/Hardiflex cladding Fibre cement cladding like Hardiplank is generally viewed favourably by insurers — it's fire-resistant, durable, and performs well in extreme weather. This is a positive factor compared to weatherboard or other timber-based cladding.

Steel/Colorbond roof A Colorbond roof is another tick in the right column. It's resilient against hail, wind, and bushfire ember attack, and tends to have a longer lifespan than terracotta or concrete tiles. This can help moderate premiums compared to more vulnerable roofing materials.

Slab foundation Concrete slab foundations are standard in Queensland and generally considered low-risk from an insurance perspective, with fewer issues around subsidence or moisture ingress compared to elevated or timber subfloor construction.

Swimming pool Pools add to the insured value of the property and can introduce liability considerations, both of which contribute to a higher premium. Pool equipment, fencing, and surrounds all need to be factored into the building sum insured.

Solar panels Solar systems are now a standard inclusion on many Queensland homes, but they do add to the replacement cost. A rooftop solar installation can represent tens of thousands of dollars in rebuild value, and insurers need to account for that.

Ducted climate control Ducted air conditioning is a significant fixed asset — expensive to install and expensive to repair or replace. Its inclusion in the building sum insured is appropriate and contributes to the overall premium.

Timber and laminate flooring These floor coverings can be costly to replace after water damage or flooding events, which is a relevant consideration in subtropical Queensland.

---

Tips for Homeowners in Wolffdene

1. Review your building sum insured regularly With a sum insured of $1,182,000, it's essential to ensure this figure reflects current rebuild costs — not the market value of your home. Construction costs have risen sharply in recent years, and being underinsured can leave you significantly out of pocket after a major claim. Consider using a qualified quantity surveyor or your insurer's rebuild cost calculator to validate the figure annually.

2. Understand your excess structure This policy carries a $3,000 building excess and a $1,000 contents excess. A higher excess typically reduces your premium, but make sure you're comfortable covering that amount out of pocket in the event of a claim. If cash flow is a concern, it may be worth comparing quotes with a lower excess to understand the premium trade-off.

3. Don't overlook storm and water damage cover Even outside a cyclone risk zone, Wolffdene is exposed to severe thunderstorms, flash flooding, and heavy rainfall events that are increasingly common in South East Queensland. Make sure your policy explicitly covers storm surge, rainwater ingress, and flash flooding — and check whether your property sits within a flood overlay under the Gold Coast City Council planning maps.

4. Compare quotes before renewal The "Fair" rating on this quote means you're not being gouged, but you may still be able to do better. Insurers price risk differently, and a quote that's average for one provider might be well below average from another. Use CoverClub to compare quotes before your renewal date — even saving $500–$700 per year adds up significantly over time.

---

Ready to Find a Better Deal?

Whether you're a Wolffdene local or researching insurance for a property in the Gold Coast hinterland, comparing quotes is one of the simplest ways to make sure you're not paying more than you need to. Head to CoverClub to get personalised home and contents insurance quotes tailored to your property — it takes just a few minutes and could save you hundreds. You can also explore detailed Wolffdene insurance statistics to see how premiums in your suburb are trending over time.