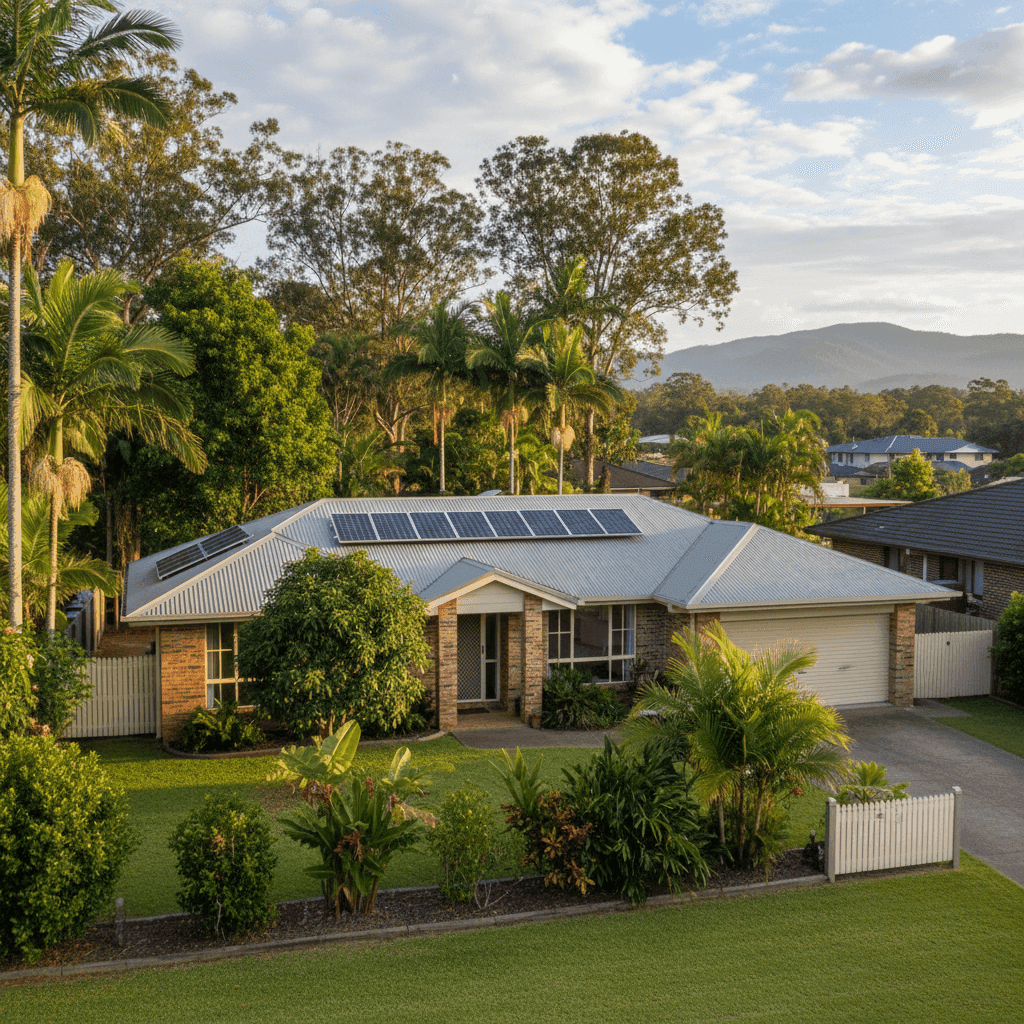

Nestled in the Atherton Tablelands of Far North Queensland, Wongabel is a quiet semi-rural locality where properties tend to sit on generous blocks surrounded by lush, tropical greenery. It's a beautiful part of the world — but that natural environment comes with its own set of insurance considerations. This article takes a close look at a real home and contents insurance quote for a three-bedroom, free-standing home in Wongabel (postcode 4883), breaking down whether the price is competitive and what factors are shaping the premium.

---

Is This Quote Fair?

The quote in question comes in at $3,264 per year (or $313 per month) for combined home and contents cover, with a $200,000 building sum insured and $10,000 in contents. Our analysis rates this as CHEAP — below average when benchmarked against comparable properties.

For homeowners in a cyclone-designated risk area like Wongabel, landing a premium below the state median is genuinely good news. Queensland is one of the most expensive states in the country for home insurance, largely driven by extreme weather exposure across the northern half of the state. A quote sitting comfortably below both the state average and the local government area (LGA) average suggests this particular property — and the insurer's assessment of it — is working in the homeowner's favour.

That said, "cheap" doesn't always mean "right." It's worth ensuring the sum insured accurately reflects what it would cost to rebuild the home from scratch, and that the contents figure covers everything of value inside.

---

How Wongabel Compares

The numbers tell a compelling story when you stack this quote against broader benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,264 |

| QLD State Median | $3,903 |

| QLD State Average | $9,129 |

| National Median | $2,764 |

| National Average | $5,347 |

| Tablelands LGA Average | $18,083 |

This quote sits $639 below the Queensland median and a remarkable $14,819 below the Tablelands LGA average. The LGA average of $18,083 is striking — it reflects just how exposed many properties across the Tablelands region are to cyclone, flood, and storm damage. The fact that this quote is so far below that figure could indicate a combination of favourable property characteristics, a competitive insurer, and a building sum insured that is lower than some comparable properties in the area.

Compared to the national median of $2,764, this quote is modestly higher — which is entirely expected given Queensland's elevated risk profile. You can explore how other properties in the region are priced on the Wongabel suburb stats page, or broaden your view with Queensland state insurance data and national home insurance statistics.

---

Property Features That Affect Your Premium

Every insurer prices a home based on a detailed picture of the property. Here's how the key features of this home likely influence the premium:

Brick Veneer Walls & Colorbond Roof

Brick veneer is generally viewed favourably by insurers — it's durable, fire-resistant, and performs reasonably well in high-wind events. Paired with a steel Colorbond roof, this combination is considered one of the more resilient construction types for Queensland conditions. Colorbond roofing in particular is designed to withstand significant wind loads, which matters greatly in a cyclone risk zone.

Slab Foundation & Tiled Flooring

A concrete slab foundation provides excellent stability and is less susceptible to water ingress from below than elevated or timber-framed subfloors. Tiled flooring throughout is similarly practical — tiles are resistant to water damage and easy to repair or replace after a weather event, which can reduce the cost of claims.

Solar Panels

The property has solar panels installed, which adds a modest layer of complexity to the insurance picture. Solar systems represent a real asset value and can be damaged in hail storms or cyclone events. Homeowners should confirm with their insurer whether the solar system is covered under the building policy and up to what value.

Ducted Climate Control

Ducted air conditioning systems are a significant fixed asset in a home. If damaged by a storm, power surge, or water ingress, replacement costs can run into the thousands. It's worth checking whether your policy covers the system for accidental damage and mechanical breakdown, or just storm-related events.

Cyclone Risk Area

This is arguably the most significant risk factor for any property in Wongabel. The entire Far North Queensland region sits within a designated cyclone risk zone, and insurers price accordingly. The relatively competitive premium here may reflect the property's solid construction materials, which are better suited to withstand cyclonic conditions than timber-framed or older homes in the same area.

Built in 1989

At around 35 years old, this home is well past its original construction phase but not yet at the age where major structural concerns typically arise. Homes of this era in Queensland were built under earlier building codes, which predate the more stringent cyclone-resistant standards introduced after Cyclone Tracy and refined further in the 1990s. Insurers may factor this in, though the brick veneer and Colorbond construction likely mitigate some of that concern.

---

Tips for Homeowners in Wongabel

1. Review Your Building Sum Insured Annually

Construction costs in regional Queensland have risen sharply in recent years. A $200,000 building sum insured for a 139 sqm home may be adequate today, but it's worth using a building cost calculator each year to ensure you're not underinsured. Rebuilding costs in regional areas can be higher than in cities due to labour and materials transport costs.

2. Confirm Your Cyclone Preparation Coverage

Many policies include specific requirements around cyclone preparation — such as securing outdoor furniture, maintaining trees, and having shutters or screens in good condition. Failing to meet these obligations could affect a claim. Read your Product Disclosure Statement (PDS) carefully and take note of any cyclone-specific conditions.

3. Check Your Solar Panel Coverage

Ask your insurer directly: are your solar panels covered, and for how much? Some policies include them as part of the building sum insured, while others treat them as a separate item or exclude them altogether. Given the cost of a quality solar system, this is worth clarifying before you need to make a claim.

4. Don't Set and Forget — Compare at Renewal

Even if this quote is competitively priced today, premiums can shift significantly at renewal. The insurance market in North Queensland is dynamic, and new entrants or policy changes can create meaningful price differences. Use a comparison tool like CoverClub each year to ensure you're still getting fair value.

---

Find the Right Cover for Your Home

Whether you're renewing your existing policy or shopping for cover for the first time, it pays to compare. CoverClub makes it easy to see how your premium stacks up against real data from properties just like yours — and to find a policy that genuinely fits your needs. Get a quote today at CoverClub and see what you could be paying.