If you own a free standing home in Woodhill, QLD 4285, you're likely no stranger to the question of whether your home insurance premium is reasonable. Woodhill is a semi-rural suburb nestled in the Logan region of South East Queensland — a pleasant place to live, but one where property characteristics, local risk factors, and the sheer size of modern homes can all push premiums in unexpected directions. This article breaks down a real home and contents insurance quote for a four-bedroom, three-bathroom brick veneer home in the area, and puts the numbers into context so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question sits at $3,302 per year (or $318/month) for combined home and contents cover, with a building sum insured of $1,238,000 and contents valued at $73,000. Both the building and contents excess are set at $2,000.

Our price rating for this quote is Expensive — above average for the Woodhill area.

To understand why, it helps to look at the local benchmarks. The suburb average premium for Woodhill sits at $2,803/yr, with a median of $2,774/yr. This quote comes in roughly $499 above the suburb average — a meaningful difference that warrants a closer look. That said, it's worth noting the sample size for Woodhill is relatively small (11 quotes), so the local data, while useful, should be treated as indicative rather than definitive.

The quote does fall within the suburb's 75th percentile range (up to $3,200/yr), though it exceeds even that upper benchmark. For a homeowner seeking value, this signals that shopping around could yield meaningful savings.

---

How Woodhill Compares

One of the most striking things about this quote is how it stacks up when you zoom out beyond the suburb level.

| Benchmark | Premium |

|---|---|

| This quote | $3,302/yr |

| Woodhill suburb average | $2,803/yr |

| Woodhill suburb median | $2,774/yr |

| LGA (Logan) average | $4,617/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

When compared to the broader QLD insurance landscape, this quote is actually well below the state average of $9,129/yr — though Queensland's average is heavily skewed by high-risk areas like Far North Queensland, where cyclone exposure drives premiums to extreme levels. The QLD median of $3,903/yr is a more useful yardstick, and this quote comes in below that figure.

Against national benchmarks, the picture is similar: the national average of $5,347/yr is dragged upward by high-risk regions, while the national median of $2,764/yr is actually slightly below this quote. So while this premium is above average for Woodhill specifically, it's not out of step with broader Australian norms for a large, well-appointed home.

You can explore more localised data on the Woodhill suburb stats page.

---

Property Features That Affect Your Premium

Several characteristics of this particular property are likely contributing to the higher-than-average premium. Understanding these factors can help you have more productive conversations with insurers.

High Building Sum Insured

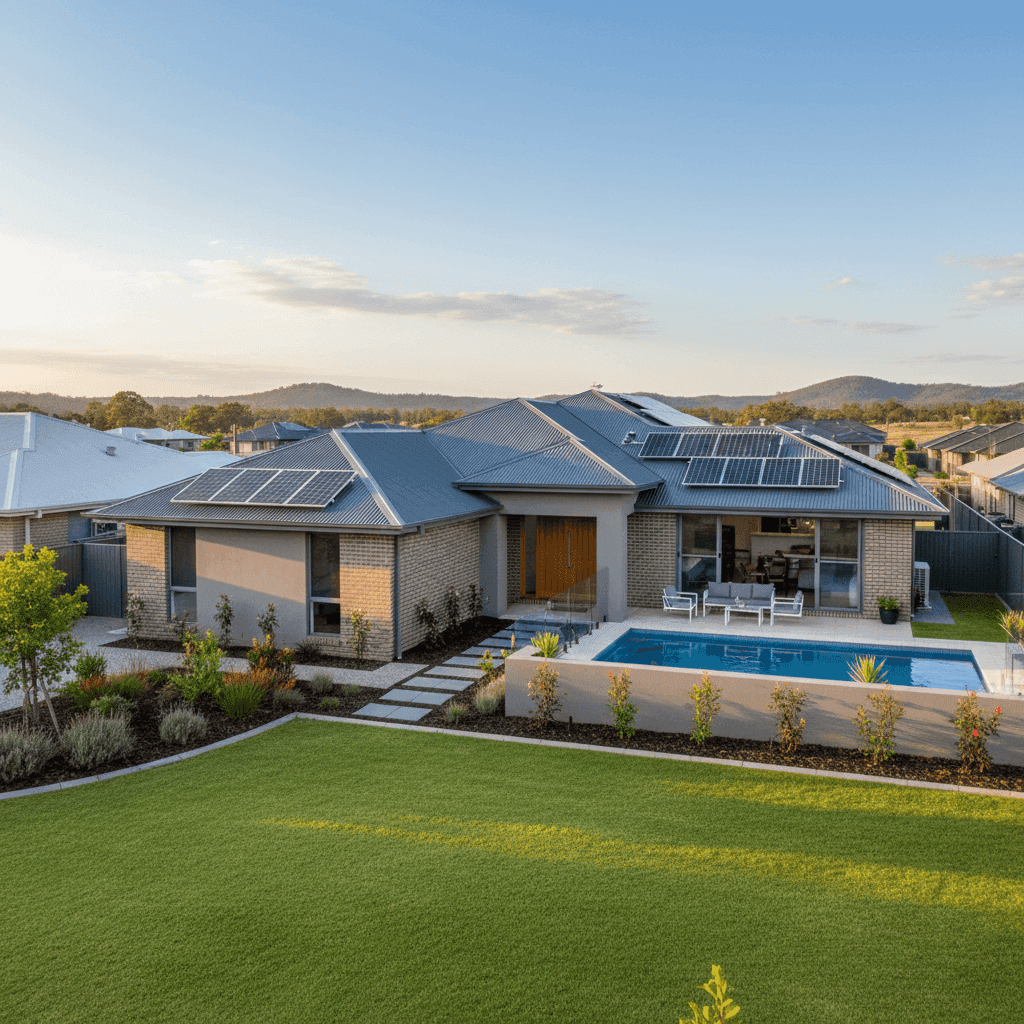

At $1,238,000, the building sum insured is substantial. This reflects the cost to fully rebuild a modern 214 sqm home with quality fittings, and it's the single biggest driver of premium cost. Newer homes built to current standards — like this 2021 build — often carry higher rebuild costs due to updated building codes, materials, and labour.

Brick Veneer Walls & Colorbond Roof

Brick veneer construction is generally viewed favourably by insurers as it's durable and fire-resistant. Similarly, a steel/Colorbond roof is considered low-maintenance and resilient. These features may actually help moderate the premium compared to, say, a timber-framed home with a tile roof prone to storm damage.

Slab Foundation & Tiled Flooring

A concrete slab foundation is standard for modern Queensland builds and is generally considered a low-risk construction type. Tiled flooring is also durable and resistant to water damage — both factors that insurers tend to view positively.

Swimming Pool

A swimming pool adds to the insurable value of the property and introduces additional liability considerations. Most insurers factor pool ownership into their risk assessment, which can nudge premiums upward.

Solar Panels

Rooftop solar panels are increasingly common in Queensland, but they do add to the replacement cost of the home. If your panels are included in the building sum insured (as they typically should be), this will contribute to a higher premium. It's worth confirming with your insurer exactly what is and isn't covered.

Ducted Climate Control

A ducted air conditioning system is a significant fixed asset within the home. Like solar panels, it adds to the overall rebuild and replacement cost, which flows through to your building sum insured and, ultimately, your premium.

No Cyclone Risk

Woodhill is not in a designated cyclone risk zone, which is a meaningful premium advantage compared to properties in North Queensland. This helps keep the quote more manageable than it might otherwise be for a Queensland property of this size and value.

---

Tips for Homeowners in Woodhill

1. Review Your Sum Insured Annually

Building costs in South East Queensland have risen sharply in recent years. It's important to ensure your sum insured keeps pace with actual rebuild costs — but equally, an over-inflated figure will unnecessarily increase your premium. Consider using an independent building cost calculator or consulting a quantity surveyor to validate your figure.

2. Compare Multiple Quotes

This quote is rated above average for Woodhill, which suggests there may be better value available in the market. Insurers assess risk differently, and a property with favourable features like brick veneer construction and a slab foundation may be priced more competitively by some providers. Use a comparison platform like CoverClub to see multiple quotes side by side.

3. Consider Your Excess Strategy

Both the building and contents excess on this policy are set at $2,000. Opting for a higher excess is one of the most straightforward ways to reduce your annual premium. If you have the financial capacity to absorb a larger out-of-pocket cost in the event of a claim, increasing your excess to $3,000 or more could deliver noticeable savings.

4. Bundle and Ask About Discounts

Many insurers offer discounts for bundling home and contents cover (as this policy does), as well as loyalty discounts, security system discounts, or discounts for paying annually rather than monthly. It's always worth asking your insurer directly what discounts are available — they aren't always proactively offered.

---

Ready to Find a Better Deal?

Whether you're happy with your current cover or suspect you might be overpaying, it pays to compare. CoverClub makes it easy for Australian homeowners to get a clearer picture of what they should be paying. Get a quote today at CoverClub and see how your premium stacks up against the market — you might be surprised at the savings on offer.