Woombye is a quiet, leafy town nestled in the Sunshine Coast hinterland — a popular choice for families and tree-changers who want a relaxed lifestyle without straying too far from the coast. But like anywhere in Queensland, insuring your home here comes with its own set of considerations. This article breaks down a real home and contents insurance quote for a three-bedroom, free-standing home in Woombye (postcode 4559), so you can get a clearer picture of what's typical — and whether there's room to do better.

---

Is This Quote Fair?

The quote in question sits at $2,771 per year (or $272/month) for combined home and contents cover, with a building sum insured of $748,000 and contents valued at $101,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. Based on recent quotes collected across Woombye, the suburb average premium sits at $2,390/yr and the median at $2,464/yr. At $2,771, this quote is slightly above the suburb median but still comfortably within the 75th percentile of $2,869 — meaning roughly three-quarters of comparable quotes in the area come in at a similar price or lower.

That said, "fair" doesn't necessarily mean "the best available." There's a meaningful spread between the cheapest quotes (around the 25th percentile at $1,741/yr) and the most expensive. A difference of over $1,000 per year between the bottom and top of the market is significant, and it underscores why comparing multiple insurers is always worthwhile.

---

How Woombye Compares

One of the most striking takeaways from this data is just how favourably Woombye stacks up against the broader Queensland and national markets.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Woombye (4559) | $2,390/yr | $2,464/yr |

| Sunshine Coast LGA | $4,457/yr | — |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

The contrast with the rest of Queensland is stark. The state average premium of $4,547/yr is nearly double what Woombye homeowners typically pay. Even within the Sunshine Coast LGA — which includes coastal and higher-risk areas — the average of $4,457/yr dwarfs the Woombye suburb figure.

Compared to the national average of $2,965/yr, Woombye again comes out ahead, with the suburb median sitting roughly $500 below the country-wide figure. This makes Woombye a relatively affordable pocket within what is, broadly speaking, an expensive state for home insurance.

The key driver of Queensland's elevated premiums is risk — particularly cyclone, flood, and storm exposure across much of the state. Woombye's inland hinterland location means it avoids some of the most severe coastal risks, which is reflected in its comparatively modest premiums.

---

Property Features That Affect Your Premium

Every property is different, and insurers weigh up a range of factors when calculating your premium. Here's how the specific features of this home play into the pricing:

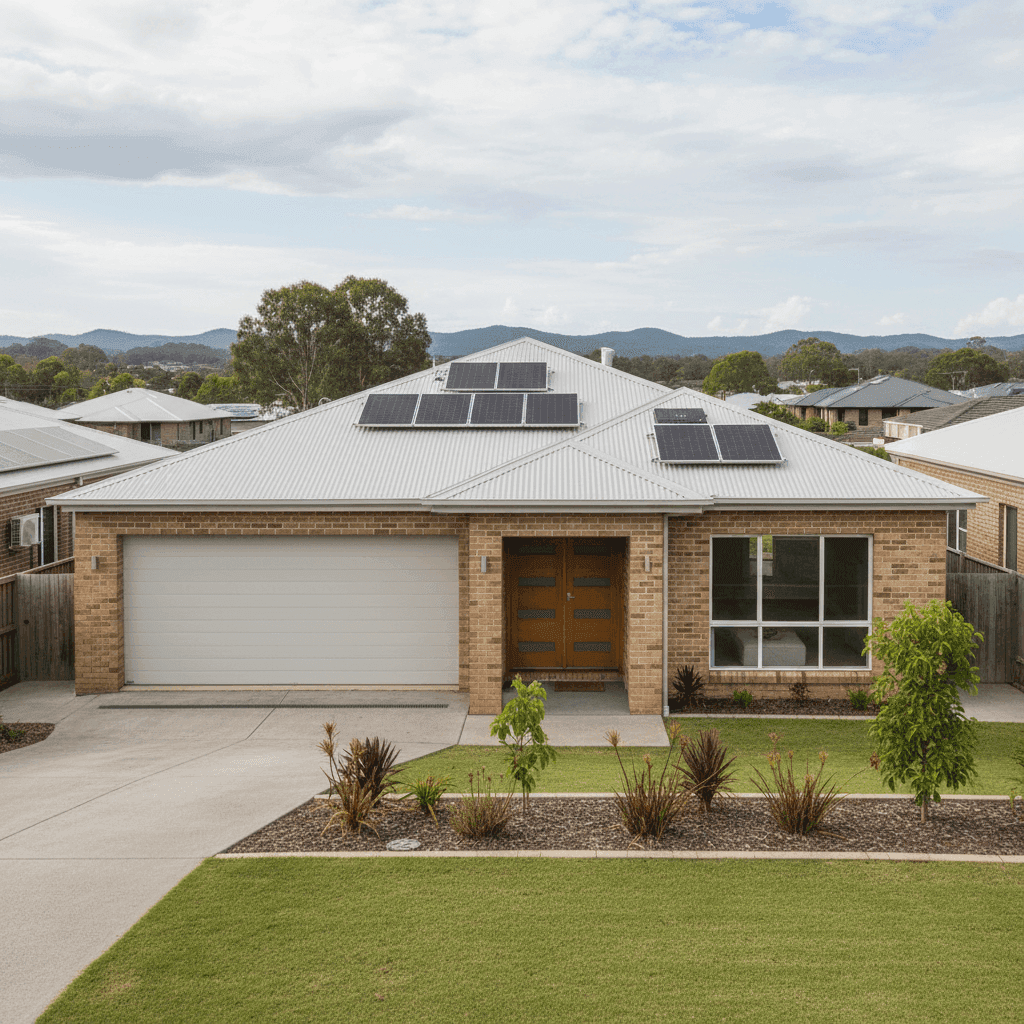

Brick Veneer Walls Brick veneer is generally viewed favourably by insurers. It offers solid fire resistance and durability, and tends to attract lower premiums than timber-framed or weatherboard construction. It's a common and well-understood building type, which helps keep pricing competitive.

Steel / Colorbond Roof Colorbond roofing is widely used across Queensland and is well-regarded for its resilience in harsh weather conditions. It's resistant to fire, doesn't rot, and handles heat well — all factors that can contribute to a more favourable risk profile compared to older roofing materials like terracotta tiles or asbestos sheeting.

Slab Foundation A concrete slab foundation is standard for homes of this era and is generally considered low-risk from an insurance perspective. It's less susceptible to subsidence and pest damage than raised timber stumps.

Construction Year: 1988 At around 36 years old, this home sits in a middle ground — old enough that some components (plumbing, electrical, roofing) may be approaching the end of their service life, but not so old as to attract the surcharges sometimes applied to heritage or pre-1970s homes. Keeping up with maintenance is important for both safety and insurance purposes.

Solar Panels The presence of solar panels is worth noting. Most home and contents policies will cover rooftop solar panels as part of the building, but it's always worth confirming this with your insurer. Damage to panels — from storms, hail, or fire — can be costly to repair or replace, so ensuring they're adequately covered under your building sum insured is essential.

Building Size: 130 sqm At 130 sqm, this is a modest-sized home, which generally keeps rebuild costs — and therefore premiums — more manageable than larger dwellings.

No Pool, No Ducted Climate Control, No Cyclone Risk Zone The absence of a pool removes a source of both liability and maintenance risk. No ducted air conditioning means fewer complex mechanical systems to insure. And crucially, Woombye falls outside the designated cyclone risk area, which is a significant factor in keeping premiums lower than coastal Queensland equivalents.

---

Tips for Homeowners in Woombye

1. Check your building sum insured regularly With a building sum insured of $748,000 for a 130 sqm home, it's worth verifying this figure reflects current rebuild costs — not just market value. Construction costs have risen sharply in recent years, and being underinsured can leave you significantly out of pocket after a major claim. Use a building cost calculator or speak with a quantity surveyor if you're unsure.

2. Confirm your solar panels are covered If your policy covers the building, solar panels are often included — but the extent of cover can vary. Ask your insurer specifically whether panels are covered for accidental damage, storm damage, and electrical faults, and check whether the replacement value is factored into your sum insured.

3. Compare quotes before renewal The spread between the 25th and 75th percentile in Woombye is over $1,100 per year. That's a meaningful saving available to those who take the time to shop around. Insurers regularly adjust their pricing models, so a quote that was competitive last year may not be the best available today.

4. Consider your excess carefully Both the building and contents excess on this policy are set at $1,000. Opting for a higher excess can reduce your annual premium, but make sure you'd be comfortable covering that amount out of pocket in the event of a claim. Conversely, if cash flow is a concern, a lower excess might be worth the slightly higher premium.

---

Ready to Compare?

Whether you're renewing your existing policy or shopping for cover on a new purchase, it pays to see what the market has to offer. Get a home insurance quote at CoverClub and compare options tailored to your property in Woombye. You can also explore local pricing data for Woombye and the surrounding area to benchmark any quote you receive.