Woombye is a charming hinterland suburb on Queensland's Sunshine Coast — known for its leafy streets, relaxed lifestyle, and a growing number of well-built family homes. If you own a free standing home in this area and you're wondering whether your home and contents insurance premium stacks up, you're in the right place. In this article, we analyse a real insurance quote for a 4-bedroom, 2-bathroom property in Woombye (postcode 4559) and put it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $3,424 per year (or roughly $321 per month) for combined home and contents cover, with a building sum insured of $911,000 and contents valued at $150,000. Both the building and contents excess sit at $1,000.

Our price rating for this quote is EXPENSIVE — above average for the Woombye area.

To put that in perspective: the suburb average premium sits at $2,823 per year, and the median is $2,867 per year. This quote is approximately 21% above the suburb average and sits well above the 75th percentile for the area ($2,998/yr), meaning it's higher than at least three-quarters of comparable quotes in Woombye.

That said, "expensive" doesn't automatically mean "wrong." A number of property-specific factors — which we'll explore below — can legitimately push a premium higher. The key question is whether those factors justify the gap, or whether there's room to shop around for a better deal.

---

How Woombye Compares

Understanding where Woombye sits in the broader insurance landscape is useful context for any homeowner.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,424 |

| Woombye Suburb Average | $2,823 |

| Woombye Suburb Median | $2,867 |

| Woombye 25th Percentile | $2,392 |

| Woombye 75th Percentile | $2,998 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

| Sunshine Coast LGA Average | $7,249 |

A few things stand out here. First, Woombye's suburb average of $2,823 is actually below the national median of $2,764 — suggesting that, on the whole, Woombye is a relatively affordable area to insure. That makes this particular quote's position above the suburb's 75th percentile even more noteworthy.

Second, Queensland's state average of $9,129 is dramatically high — largely skewed by high-risk coastal and far-north Queensland properties prone to cyclones and flooding. The QLD median of $3,903 is a more representative figure, and this quote still falls below that mark.

The Sunshine Coast LGA average of $7,249 is also elevated, likely reflecting a mix of premium coastal properties and flood- or storm-prone areas within the region. By comparison, Woombye sits in a more sheltered hinterland position, which generally works in homeowners' favour.

You can explore more local data on the Woombye suburb insurance stats page, or broaden your view with Queensland-wide insurance data and national home insurance statistics.

---

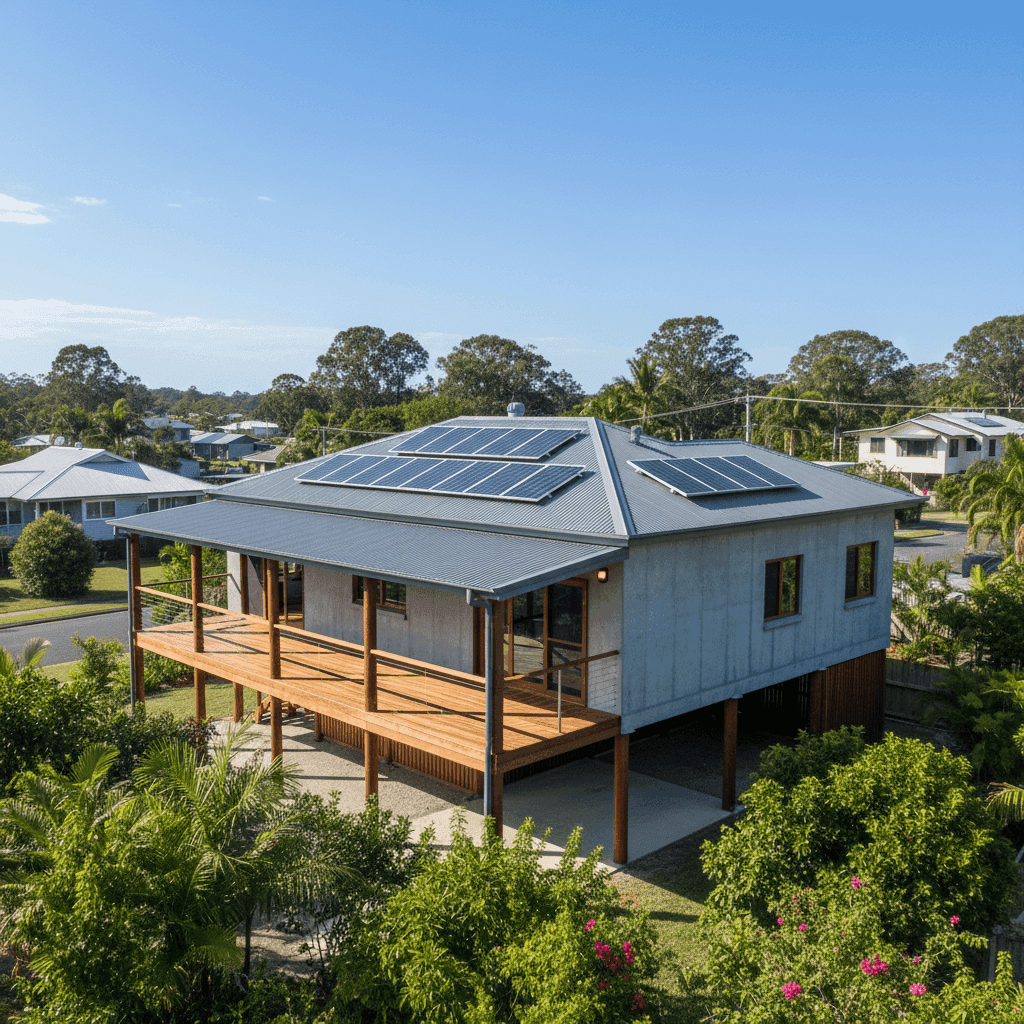

Property Features That Affect Your Premium

Every insurer assesses risk differently, but the physical characteristics of a property play a significant role in determining what you'll pay. Here's how the features of this particular home may be influencing the premium:

Concrete external walls are generally viewed favourably by insurers — they're durable, fire-resistant, and less susceptible to termite damage than timber. This should, in theory, work in the homeowner's favour.

Steel/Colorbond roofing is another positive signal. Colorbond is a popular and resilient roofing material in Queensland, offering strong resistance to wind, rain, and corrosion. Insurers typically rate it well compared to older tile or corrugated iron roofs.

Elevated construction (at least 1 metre off the ground) is a defining feature of this property. While an elevated or pole-frame home is a classic Queensland design that offers excellent flood resilience and airflow, insurers can sometimes price these homes higher due to the additional complexity of repairs, particularly to the subfloor structure and the timber/laminate flooring above.

Pole foundation ties into the elevated design and can be a factor in premium calculations. Pole homes can be more expensive to repair after storm or wind events, as the structural connection points require specialist assessment.

Timber and laminate flooring is susceptible to water damage, which may contribute marginally to the premium — particularly in a region that receives significant rainfall.

Solar panels add replacement value to the home and may slightly increase the insured sum or the assessed rebuild cost. It's worth confirming with your insurer whether your solar system is explicitly included in your building cover.

Ducted climate control is another high-value fixed inclusion that contributes to the overall building sum insured of $911,000 — a figure that is on the higher end and will directly influence the premium.

The absence of a pool and the non-cyclone-rated location are both factors that keep the premium lower than it might otherwise be in coastal Queensland.

---

Tips for Homeowners in Woombye

If you're looking to get better value on your home and contents insurance, here are some practical steps worth considering:

- Compare quotes from multiple insurers. This is the single most effective way to reduce your premium. The spread between the 25th percentile ($2,392) and this quote ($3,424) in Woombye alone is over $1,000 per year — a meaningful saving available to those who shop around. Use CoverClub to compare quotes in minutes.

- Review your sum insured carefully. A building sum insured of $911,000 is substantial. Make sure this reflects the actual cost to rebuild your home (not its market value), and consider using a professional building cost estimator. Over-insuring is a common and costly mistake.

- Ask about bundling discounts. Many insurers offer a discount when you combine home and contents cover under the same policy — which this quote already does. However, it's worth checking whether the bundled price is genuinely competitive, or whether separate policies from different providers might be cheaper overall.

- Check your excess settings. Both excesses here are set at $1,000. Opting for a higher voluntary excess can meaningfully reduce your annual premium — just ensure you could comfortably cover that amount in the event of a claim.

---

Ready to Find a Better Deal?

Whether you're renewing your policy or buying insurance for the first time, comparing your options is the smartest move you can make. CoverClub makes it easy to see what Woombye homeowners are paying and find a quote that works for your budget. Get a home insurance quote today and see how much you could save.