Woree is a quiet residential suburb on the southern fringe of Cairns in Far North Queensland — and like much of the region, it sits squarely in one of Australia's most challenging home insurance markets. This article breaks down a real home and contents insurance quote for a three-bedroom, free-standing home in Woree (postcode 4868), explores how the premium stacks up against local and national benchmarks, and offers practical tips for homeowners looking to manage their insurance costs.

---

Is This Quote Fair?

The quote in question comes in at $2,719 per year (or $247 per month) for combined home and contents cover, with a building sum insured of $498,000 and contents valued at $127,000. The building excess is $2,000 and the contents excess $1,000.

Our price rating for this quote is Expensive — Above Average.

To put that in context: the average premium across the 15 quotes sampled in Woree sits at $2,122 per year, with a median of $2,001. This quote lands above the suburb's 75th percentile of $2,542, meaning it's pricier than at least three-quarters of comparable quotes in the area. That's a meaningful gap — roughly $600 more per year than the suburb average.

That said, "expensive" is relative. The sum insured here is substantial ($498,000 for the building alone), and the contents value of $127,000 is on the higher side. Higher coverage limits naturally push premiums up, so some of the price difference is likely attributable to the level of cover rather than the insurer simply overcharging. It's still worth shopping around, but the quote isn't wildly out of step when you factor in what's being covered.

---

How Woree Compares

Woree's insurance pricing tells an interesting story when set against broader benchmarks. Here's how the numbers line up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Woree (suburb) | $2,122/yr | $2,001/yr |

| Queensland (state) | $9,129/yr | $3,903/yr |

| Australia (national) | $5,347/yr | $2,764/yr |

| Cairns LGA | $12,404/yr | — |

The state and national averages look eye-watering at first glance, but those figures are heavily skewed by high-risk coastal and cyclone-prone postcodes — many of which are right here in Far North Queensland. The median figures are more representative of what most homeowners actually pay.

Woree's median of $2,001 sits comfortably below the national median of $2,764, which is somewhat surprising given the suburb's location within the Cairns LGA — an area with an average premium of $12,404 per year. This suggests that Woree, while still a cyclone risk area, may benefit from slightly more favourable risk characteristics compared to beachside or low-lying parts of the Cairns region.

You can explore more local data on the Woree suburb stats page, compare it to Queensland-wide insurance trends, or see where it sits against national home insurance averages.

---

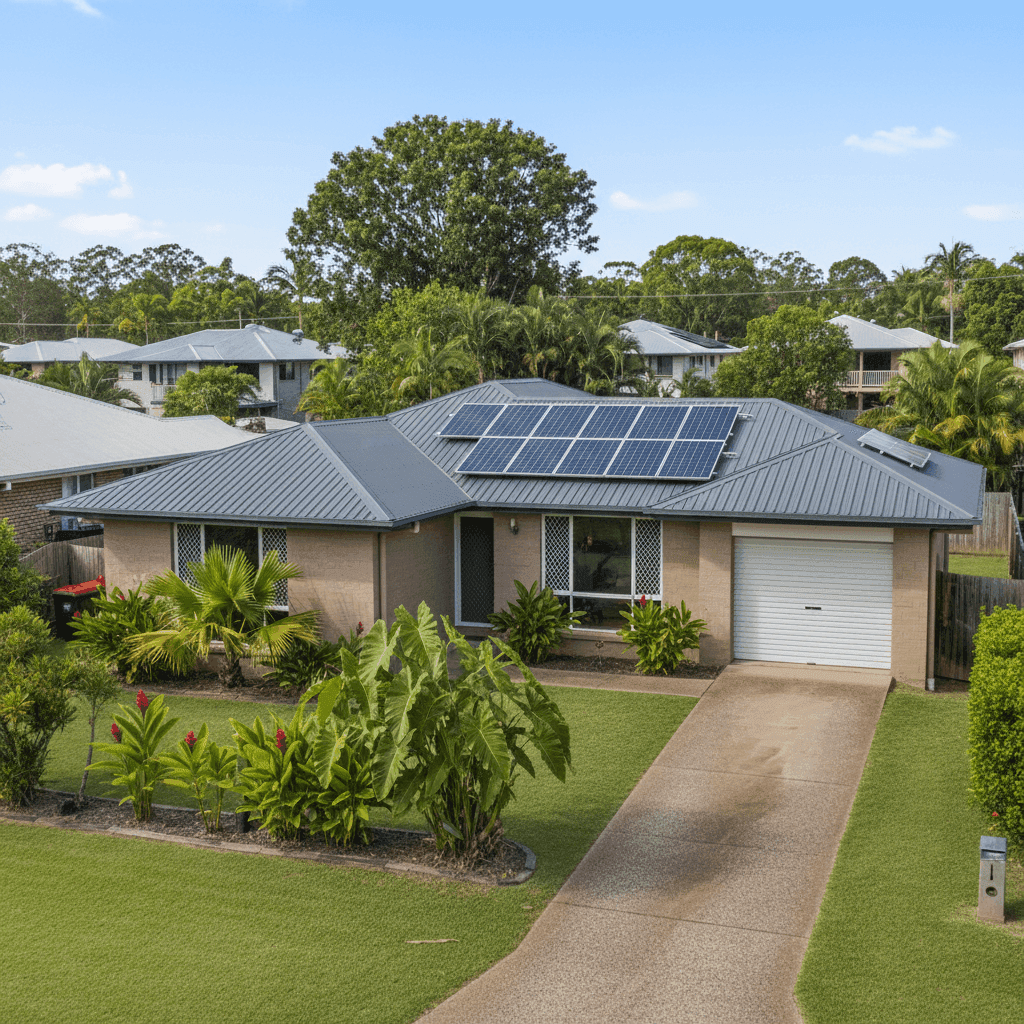

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge — for better and for worse.

🌀 Cyclone Risk Zone

This is the single biggest factor. Woree falls within a designated cyclone risk area, and insurers price this in heavily. Policies in cyclone-prone regions typically include higher base premiums and, in some cases, separate cyclone excess clauses. There's little a homeowner can do to change their geographic risk, but choosing a policy with a competitive cyclone component is essential.

🧱 Concrete Walls & Colorbond Roof

Concrete external walls are generally viewed favourably by insurers — they're durable, fire-resistant, and perform well in high-wind events. Similarly, a steel Colorbond roof is considered a resilient roofing material, particularly in cyclone-prone areas where it can be secured to meet higher wind-load standards. These construction features likely work in this property's favour when it comes to pricing.

🏗️ Slab Foundation & Tile Flooring

A concrete slab foundation is the standard for Queensland homes of this era and is generally considered low-risk. Tile flooring is similarly robust and easy to replace, which can reduce claims costs compared to timber or carpet.

☀️ Solar Panels

The property has solar panels installed. These are typically covered under home building insurance, but it's worth confirming with your insurer that the panels and associated inverter are explicitly included in the sum insured. Some policies treat solar panels as a standard fixture; others may require a separate endorsement.

📅 1980 Construction

Built in 1980, this home predates some of the more stringent cyclone-resistant building codes introduced in Queensland following Cyclone Tracy (1974) and subsequent reviews. Older homes can attract slightly higher premiums due to the potential for ageing wiring, plumbing, and structural components. That said, a well-maintained 1980s concrete home is generally still considered a solid risk.

📐 130 sqm Building Size

At 130 square metres, this is a modest-sized home, which helps keep the rebuild cost — and therefore the sum insured — at a manageable level. The $498,000 building sum insured appears reasonable for a concrete-construction home in this region, factoring in current construction costs.

---

Tips for Homeowners in Woree

1. Shop Around — Seriously

Our data shows a wide spread of premiums in Woree, from $1,488 at the 25th percentile to $2,542 at the 75th. That's over $1,000 difference for broadly similar properties. Insurers price cyclone risk very differently, so comparing multiple quotes is one of the most effective ways to reduce your premium. Get a quote at CoverClub to see what's available for your address.

2. Review Your Sum Insured Annually

Building costs in Queensland have risen sharply in recent years. Make sure your sum insured reflects current rebuild costs — not what you paid for the house, and not a figure set years ago. Underinsurance is a real risk, particularly in a market where construction labour and materials have become significantly more expensive.

3. Confirm Solar Panel Coverage

If your solar system is a meaningful asset (and at current panel and inverter prices, it likely is), confirm with your insurer exactly how it's covered. Ask whether storm, hail, and cyclone damage to the panels is included, and whether the inverter is separately listed. Don't assume — get it in writing.

4. Consider Your Excess Strategy

This quote carries a $2,000 building excess and a $1,000 contents excess. Opting for a higher excess is one of the most straightforward ways to reduce your annual premium. If you have an emergency fund and are unlikely to make small claims, a higher excess can deliver meaningful savings over time. Just make sure the excess is genuinely affordable if you do need to claim.

---

Ready to Compare?

Whether you're reviewing an existing policy or shopping for cover for the first time, comparing quotes is the smartest move you can make as a homeowner in Woree. Premiums vary significantly between insurers — especially in cyclone-risk areas — and a few minutes of comparison could save you hundreds of dollars a year.

Compare home insurance quotes at CoverClub and see what's available for your property today.