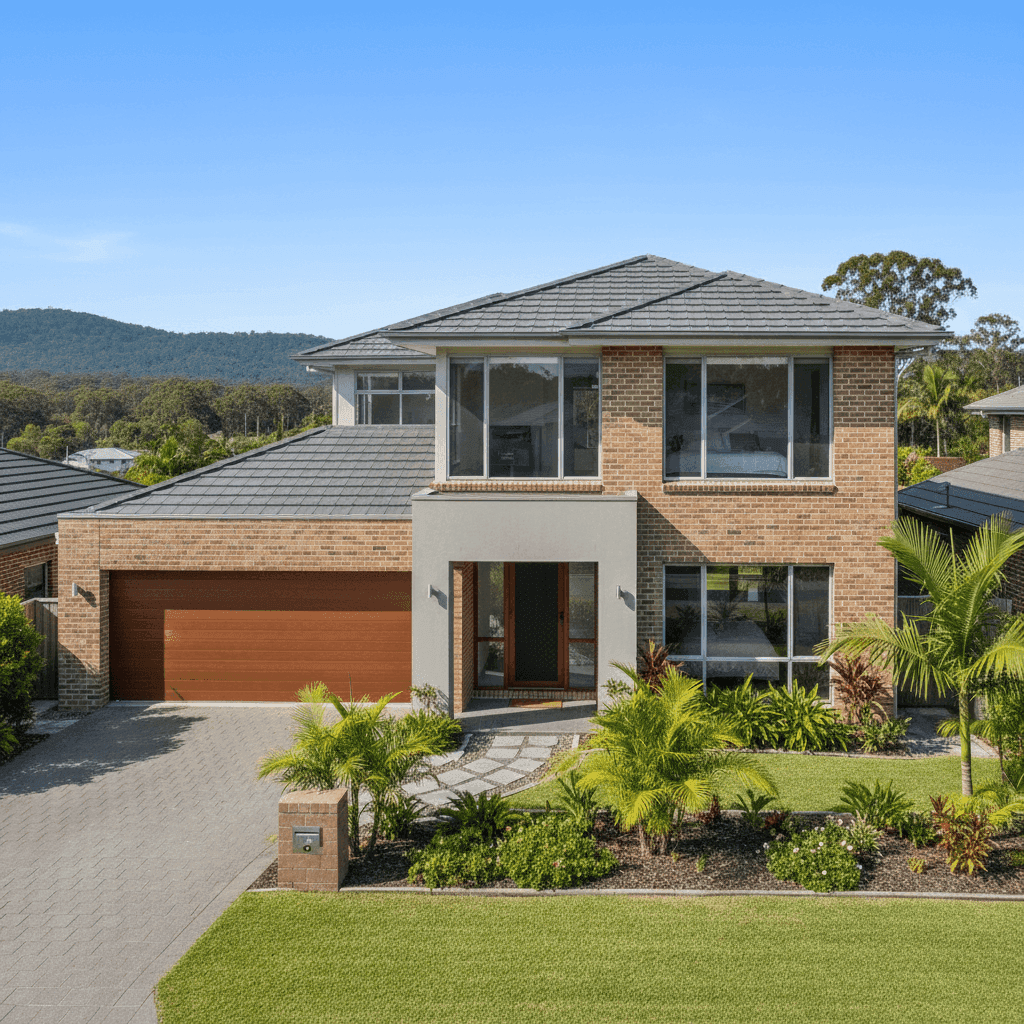

Worongary is a quiet, leafy suburb nestled in the Gold Coast hinterland — and if you own a free standing home here, you're likely paying more for insurance than you might expect. That said, not every homeowner is stuck with a hefty premium. This article breaks down a recent home and contents insurance quote for a five-bedroom property in Worongary (postcode 4213), explores how it stacks up against local, state and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The quote in question comes in at $2,777 per year (or $266 per month) for a combined home and contents policy — covering a building sum insured of $800,000 and contents valued at $80,000, each with a $1,000 excess.

Our price rating for this quote? Cheap — well below average.

To put that into perspective, the suburb average for Worongary sits at $7,358 per year, and the median is even higher at $7,804 per year. That means this quote is roughly 62% below the suburb average — a significant saving by any measure. Even at the lower end of the local market (the 25th percentile), comparable properties are paying around $5,825 per year, which is still more than double this quote.

For a five-bedroom home with above-average fittings, ducted climate control, and timber/laminate flooring, landing a premium under $3,000 annually is genuinely impressive. It suggests the insurer has assessed this particular property's risk profile favourably — likely influenced by the home's modern construction (2026), brick veneer walls, tiled roof, and slab foundation, all of which are considered low-to-moderate risk features.

---

How Worongary Compares

Understanding where Worongary sits in the broader insurance landscape helps put this quote into context. Here's a snapshot:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,777 |

| Worongary Suburb Average | $7,358 |

| Worongary Suburb Median | $7,804 |

| Gold Coast LGA Average | $8,161 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

A few things stand out here. The Gold Coast LGA average of $8,161 per year reflects the elevated risk profile of coastal and hinterland properties across the region — storm damage, flooding, and subsidence are all factors insurers price in. The Queensland state average of $9,129 is the highest in the country, largely driven by cyclone risk in northern parts of the state and severe weather events across the south-east.

Interestingly, this quote sits very close to the national median of $2,764 — suggesting it's priced more like a low-risk property in a benign climate than a Gold Coast hinterland home. That's a strong outcome for the homeowner.

You can explore more local data on the Worongary suburb stats page.

---

Property Features That Affect Your Premium

Insurance premiums aren't arbitrary — they're calculated based on a detailed assessment of your property's characteristics. Here's how the key features of this home influence its risk profile:

Brick Veneer Walls Brick veneer is one of the most common external wall types in Queensland and is generally well-regarded by insurers. It offers good resistance to fire and impact, which can help keep premiums in check compared to timber or lightweight cladding.

Tiled Roof Concrete or terracotta tiles are considered a durable, low-maintenance roofing option. They perform well in most weather conditions and are less susceptible to wind uplift than corrugated iron in non-cyclone areas, which Worongary is classified as.

Slab Foundation A concrete slab is a solid, stable foundation type that reduces the risk of subsidence and pest-related damage. Insurers generally view slab homes favourably compared to those on stumps or piers, particularly in areas with reactive soils.

New Construction (2026) A brand-new home is a significant advantage when it comes to insurance pricing. Modern builds must comply with current Australian Standards and the National Construction Code, meaning they're built to withstand contemporary weather and structural requirements. Newer homes also have less deferred maintenance risk.

Above-Average Fittings Higher-quality fittings — think stone benchtops, premium appliances, and quality fixtures — increase the replacement cost of the home, which is reflected in the $800,000 building sum insured. While this means a higher insured value, it doesn't necessarily push premiums sky-high if the risk profile is otherwise sound.

Ducted Climate Control Ducted air conditioning systems add to the overall value of the home and are factored into contents and building valuations. They can also introduce some risk around water damage if systems aren't maintained, though this is generally a minor consideration.

Timber and Laminate Flooring Timber and laminate floors are susceptible to water damage, which is worth keeping in mind when reviewing your policy's water damage inclusions and exclusions.

---

Tips for Homeowners in Worongary

Whether you're reviewing an existing policy or shopping for the first time, here are four practical steps to make sure you're getting the right cover at the right price.

1. Don't underinsure your building With a new build and above-average fittings, it's critical your building sum insured accurately reflects full replacement cost — not just market value. Construction costs have risen sharply in recent years, so it's worth revisiting your estimate annually. The $800,000 figure in this quote appears appropriate for a five-bedroom, four-bathroom home of this quality.

2. Review your contents value carefully $80,000 in contents cover is a reasonable starting point, but five-bedroom homes with quality fittings often house more than people initially estimate. Do a room-by-room inventory — furniture, electronics, appliances, clothing, and valuables all add up quickly.

3. Compare multiple quotes every year The wide spread of premiums in Worongary (from $5,825 at the 25th percentile to $9,005 at the 75th) shows that different insurers assess the same suburb very differently. Loyalty doesn't always pay — shopping around at renewal could save you thousands.

4. Check your policy's storm and water damage clauses Even though Worongary is not classified as a cyclone risk area, the Gold Coast region does experience intense summer storms, heavy rainfall, and occasional flash flooding. Make sure your policy clearly covers storm surge, rainwater ingress, and internal water damage from burst pipes or appliance leaks.

---

Get a Quote for Your Worongary Home

If you own a home in Worongary and haven't compared your insurance recently, now is a great time to see what's available. As this analysis shows, premiums in the area vary enormously — and there's every chance you could be paying significantly less than the suburb average. Get a home insurance quote at CoverClub in minutes and see how your current policy stacks up.