Worrigee is a quiet residential suburb on the South Coast of New South Wales, sitting within the Shoalhaven local government area. For owners of a free standing home in this part of NSW 2540, finding the right home and contents insurance at a competitive price can be a real challenge — particularly as premiums across the country continue to climb. This article breaks down a recent quote of $2,733 per year for a five-bedroom brick veneer home in Worrigee, compares it against local, state, and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The short answer: this quote is rated Expensive — sitting above average for the Worrigee area.

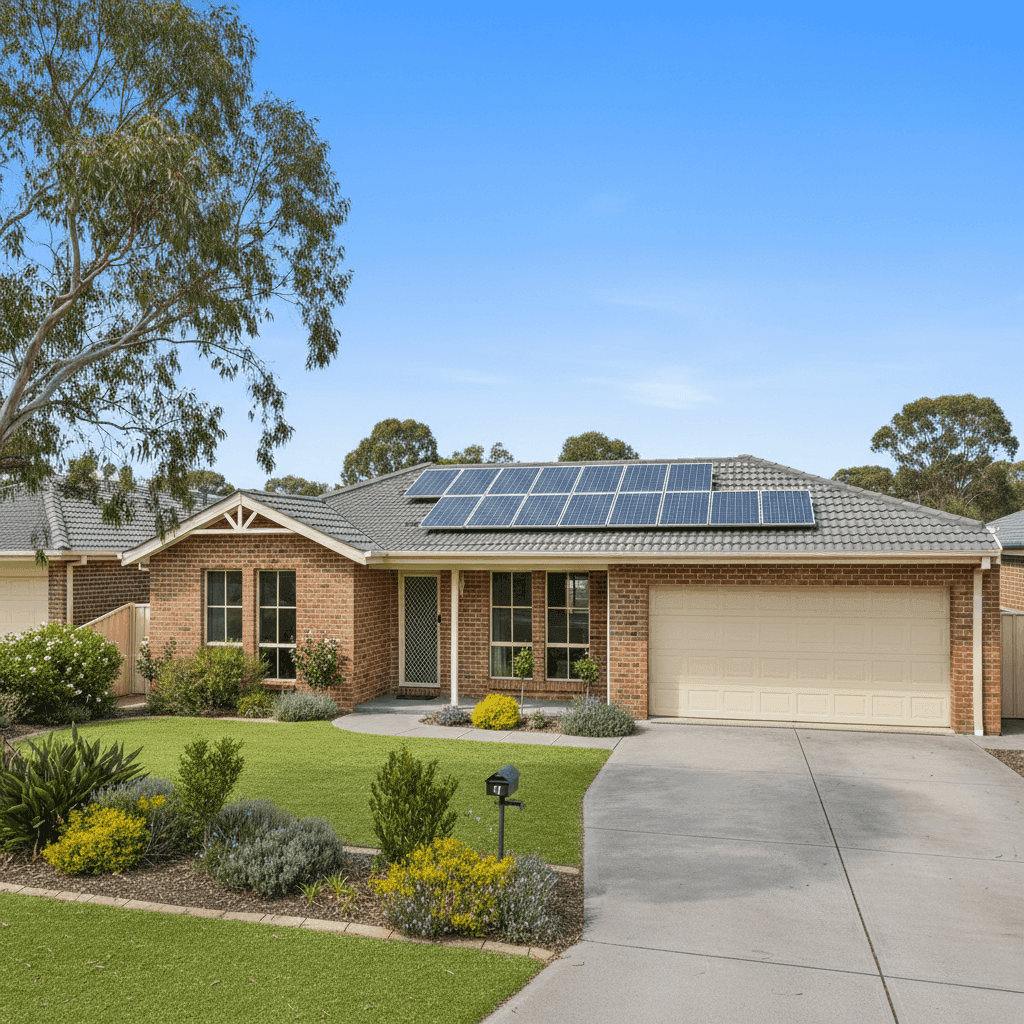

At $2,733 per year (or $262 per month), this Home and Contents policy covers a building sum insured of $667,000 and contents valued at $90,000, with a $1,000 excess on both building and contents claims. While those are reasonable coverage amounts for a five-bedroom, three-bathroom home of 214 sqm built in 2002, the premium is noticeably higher than what most Worrigee homeowners are paying.

To put it in perspective, the suburb average premium sits at just $1,354 per year, and the median is even lower at $1,143 per year. This quote comes in more than double the local median — a significant gap that warrants closer scrutiny. Even at the 75th percentile for Worrigee (meaning 75% of quotes are cheaper), the figure is $1,961 per year, still well below this quote.

That said, it's worth noting that this property's higher sum insured and larger-than-average size will naturally push the premium upward compared to smaller or lower-value homes in the area. The comparison data pool for Worrigee is also relatively modest at 13 quotes, so the local averages may not fully capture the range of property types in the suburb.

---

How Worrigee Compares

Understanding where Worrigee sits in the broader insurance landscape helps put this quote in context. Here's a snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Worrigee (NSW 2540) | $1,354/yr | $1,143/yr |

| New South Wales | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, the NSW state average of $9,528 per year is extraordinarily high — this is heavily skewed by flood- and cyclone-prone areas in regional and coastal NSW where premiums can be extreme. The state median of $3,770 is a more reliable reference point, and against that figure, this Worrigee quote of $2,733 actually looks more reasonable.

Similarly, the national median of $2,764 per year is very close to this quote, suggesting that on a broader scale, the pricing isn't wildly out of step. The Shoalhaven LGA average of $2,613 per year also aligns closely, reinforcing that this quote is in the right ballpark for the region — even if it's above the Worrigee suburb average specifically.

The key takeaway: compared to the suburb, this quote is expensive; compared to the state and nation, it's closer to average. The right benchmark depends on the specific property and coverage level being compared.

---

Property Features That Affect Your Premium

Several characteristics of this property will be influencing the premium, both positively and negatively.

Brick veneer construction and a tiled roof are generally well-regarded by insurers. These materials offer solid fire resistance and durability, and are less vulnerable to wind and hail damage than lighter cladding or metal roofing alternatives. This combination typically attracts more favourable pricing.

Slab foundation is standard for homes of this era in NSW and doesn't typically add risk from an insurance perspective. However, it does mean the property may be more exposed to ground movement if soil conditions change — something worth being aware of in coastal areas.

Solar panels are an increasingly common feature, but they do add to the insured value of the home and can complicate claims involving roof damage. Make sure your policy explicitly covers solar panels as part of the building sum insured — not all policies do by default.

Ducted climate control is another high-value fixture that contributes to the overall building replacement cost. Systems like these can be expensive to repair or replace, and ensuring your sum insured of $667,000 adequately accounts for this is important.

Property size is a significant driver. At 214 sqm with five bedrooms and three bathrooms, this is a larger-than-average home. Rebuild costs scale with size, and a $667,000 sum insured reflects that reality. Under-insuring a property of this scale would be a costly mistake.

The absence of a pool is a minor positive — pools add liability risk and can nudge premiums higher. The property is also outside a designated cyclone risk area, which removes one of the more significant premium inflators seen elsewhere in Australia.

---

Tips for Homeowners in Worrigee

1. Shop around and compare multiple insurers The gap between the cheapest and most expensive quotes in Worrigee is substantial. With suburb premiums ranging from under $986 at the 25th percentile to over $1,961 at the 75th percentile, the insurer you choose makes a real difference. Use CoverClub's free quote comparison tool to see multiple options side by side.

2. Review your sum insured carefully A $667,000 building sum insured is meaningful — but is it accurate? Overestimating your rebuild cost can inflate your premium unnecessarily, while underestimating leaves you exposed. Consider using a professional building cost estimator or asking your insurer how they calculated the figure.

3. Consider your excess strategically Both the building and contents excess on this policy are set at $1,000. Opting for a higher voluntary excess (say, $2,000 or $2,500) can meaningfully reduce your annual premium. If you have a solid emergency fund and are unlikely to make small claims, this trade-off often makes financial sense.

4. Check what's covered for solar panels and ducted systems As noted above, solar panels and ducted air conditioning are high-value inclusions that not every standard policy covers comprehensively. Before renewing or switching, confirm that these items are explicitly listed under your building cover and that the limits are sufficient.

---

Ready to Find a Better Deal?

Whether you're renewing your existing policy or shopping for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. At CoverClub, we make it easy to see how your home insurance stacks up — and to find cover that fits your property and your budget.

Get a home insurance quote for your Worrigee property today →

You can also explore detailed insurance pricing data for Worrigee and the NSW 2540 postcode, browse NSW-wide insurance statistics, or check out national home insurance benchmarks to see how your area compares across Australia.