Worrigee is a quiet residential suburb in the Shoalhaven region of New South Wales, sitting just inland from the coastal town of Nowra. It's a popular area for families, with a mix of newer builds and established homes on generous blocks. This article takes a close look at a recent home and contents insurance quote for a four-bedroom, free-standing home in Worrigee — breaking down whether the price stacks up, how it compares to broader benchmarks, and what homeowners in the area can do to keep premiums in check.

---

Is This Quote Fair?

The quote in question comes in at $2,953 per year (or $283 per month) for combined home and contents cover, with a building sum insured of $829,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — above average for the Worrigee area.

To put that in context: the suburb average premium sits at just $1,354 per year, and the median is even lower at $1,143 per year. This quote is more than twice the suburb median, which is a significant gap worth understanding.

That said, it's important not to read too much into suburb-level data alone — the Worrigee sample includes only 13 quotes, which means the figures can shift considerably with just a few high or low outliers. The 75th percentile for the suburb is $1,961 per year, and this quote sits well above even that threshold, suggesting it is genuinely on the higher end relative to comparable properties in the postcode.

At the state level, the picture looks a little different. The NSW average premium is a striking $9,528 per year, though the median — a more reliable indicator — is $3,770 per year. Against the state median, this quote is actually below average, which reflects the relatively lower risk profile of inland Shoalhaven compared to coastal or flood-prone parts of NSW. Nationally, the median sits at $2,764 per year, putting this quote modestly above the national midpoint.

In short: this premium is on the higher side for Worrigee specifically, but not out of step with broader NSW and national benchmarks when you factor in the property's size, features, and sum insured.

---

How Worrigee Compares

Here's a quick snapshot of how this quote sits across different comparison points:

| Benchmark | Premium |

|---|---|

| This quote | $2,953/yr |

| Worrigee suburb average | $1,354/yr |

| Worrigee suburb median | $1,143/yr |

| Worrigee 75th percentile | $1,961/yr |

| NSW state median | $3,770/yr |

| National median | $2,764/yr |

You can explore Worrigee suburb insurance statistics, NSW state-wide data, and national home insurance benchmarks on CoverClub to see how other properties in the area are being priced.

One important caveat: the suburb sample of 13 quotes is relatively small. As more data comes in, the suburb averages will become more reliable. For now, the state and national medians provide a useful broader reference point.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on the premium — both upward and downward.

Building Size and Sum Insured

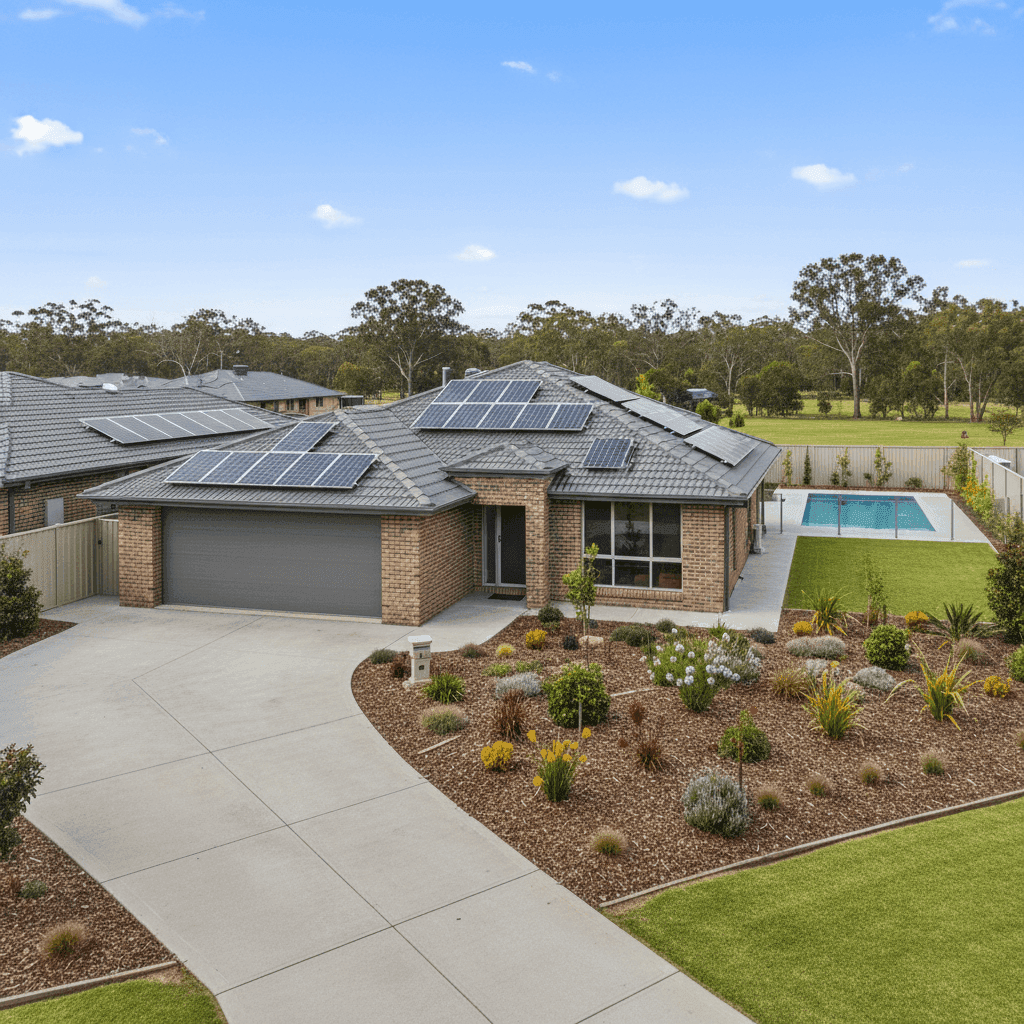

At 244 square metres and a building sum insured of $829,000, this is a substantial home. Larger homes cost more to rebuild, and insurers price accordingly. The sum insured is the single biggest driver of building premium, so it's worth ensuring this figure accurately reflects current construction costs — neither over- nor under-insured.

Brick Veneer Walls and Tiled Roof

Brick veneer construction with a tiled roof is generally viewed favourably by insurers. These materials offer solid fire resistance and durability, which can help moderate premiums compared to homes with timber frames or metal roofing in some risk categories.

Slab Foundation

A concrete slab foundation is a neutral-to-positive factor for insurers. It reduces the risk of subsidence and pest-related structural damage compared to raised timber stumps, and is a common and well-understood construction type in NSW.

Swimming Pool

The presence of a pool adds to the insured value of the property and introduces some liability considerations. Pool equipment, fencing compliance, and potential water damage risks all contribute to a slightly higher premium.

Solar Panels

Solar panels are increasingly common on Australian homes, but they do add to rebuild costs and replacement value. Insurers factor in the cost of reinstalling panels when calculating the building sum insured, so it's worth confirming your policy explicitly covers them.

Ducted Climate Control

Ducted air conditioning systems are expensive to repair or replace, and their inclusion in the home's fixtures increases the effective rebuild cost. This is another feature that nudges the sum insured — and therefore the premium — upward.

Timber and Laminate Flooring

Timber and laminate floors are popular for their aesthetics but can be costly to replace after water damage or fire. This is a factor that may influence contents and building cover assessments, particularly in the event of a claim.

---

Tips for Homeowners in Worrigee

1. Review Your Sum Insured Annually

Building costs have risen sharply in recent years. If your sum insured hasn't been updated to reflect current construction costs per square metre in the Shoalhaven region, you could be either underinsured (risky) or overinsured (expensive). Use a building cost calculator or speak to a local builder to get a realistic estimate.

2. Shop Around — Even If You're Happy With Your Insurer

The gap between the cheapest and most expensive quotes in Worrigee is significant. Using a comparison platform like CoverClub takes just a few minutes and can reveal meaningful savings without sacrificing cover quality.

3. Consider Your Excess Settings

This policy carries a $1,000 excess on both building and contents. Opting for a higher excess — say, $2,000 — can reduce your annual premium noticeably. If you're unlikely to make small claims, this trade-off often makes financial sense.

4. Bundle Building and Contents Thoughtfully

Combined home and contents policies can offer convenience and sometimes a discount, but it's worth checking whether the contents sum insured of $50,000 accurately reflects what you own. Under-insuring contents is a common mistake that can leave you out of pocket after a claim.

---

Ready to Compare?

Whether you're renewing your existing policy or shopping for cover on a new property, it pays to compare. CoverClub makes it easy to see real quotes from multiple insurers side by side, so you can make a confident, informed decision. Get a home insurance quote today and find out if you're getting a fair deal on your Worrigee home.