Wowan is a small rural locality in Central Queensland, sitting within the Banana Shire roughly 100 km west of Rockhampton. It's a quiet part of the world — but that doesn't mean home insurance is simple or cheap. For owners of older free standing homes in the region, premiums can vary enormously depending on a property's age, construction materials, and risk profile. This article breaks down a real home and contents insurance quote for a 2-bedroom free standing home in Wowan QLD 4702, examines how it stacks up against Queensland and national benchmarks, and offers practical tips for getting the best value cover.

---

Is This Quote Fair?

The annual premium for this property came in at $4,487 per year (or $439/month), covering a building sum insured of $458,000 and contents valued at $10,000. CoverClub's pricing engine has rated this quote as CHEAP — below average for its risk profile.

That's encouraging news for the homeowner. Despite several features that typically push premiums upward — fibro asbestos cladding, a 1930s construction date, and a stumped timber-floor foundation — the quote lands well below what many Queensland homeowners are paying. The building excess of $5,000 is on the higher side, which will have contributed to reducing the annual cost, but even accounting for that, the premium represents solid value relative to comparable properties.

It's worth noting that a higher excess means more out-of-pocket exposure if you do need to make a claim. For a property with some age-related risk factors, that's a trade-off worth thinking about carefully.

---

How Wowan Compares

There is no suburb-level pricing data available for Wowan at this stage — not surprising given how sparsely populated the area is. However, we can draw meaningful comparisons using Wowan's postcode stats and broader benchmarks.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $4,487 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

A few things stand out here. Queensland's average premium of $9,129 is extraordinarily high — nearly double the national average — largely driven by the elevated flood, storm, and cyclone risk that affects much of the state. This property in Wowan, rated as not in a cyclone risk area, sidesteps one of the biggest premium drivers in QLD.

At $4,487, this quote sits:

- 51% below the Queensland state average

- 16% above the Queensland median

- 16% below the national average

- 62% above the national median

In plain terms: for a Queensland property, this is a very competitive premium. Compared to the national median, it's higher — but that median is skewed by lower-risk states like Victoria and South Australia where premiums are structurally cheaper. For a 95-year-old home with fibro asbestos walls in regional QLD, landing below the national average is a genuinely strong result.

You can explore Queensland-wide insurance data and national trends on CoverClub to see how different regions and property types compare.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium calculated. Here's how each one plays out:

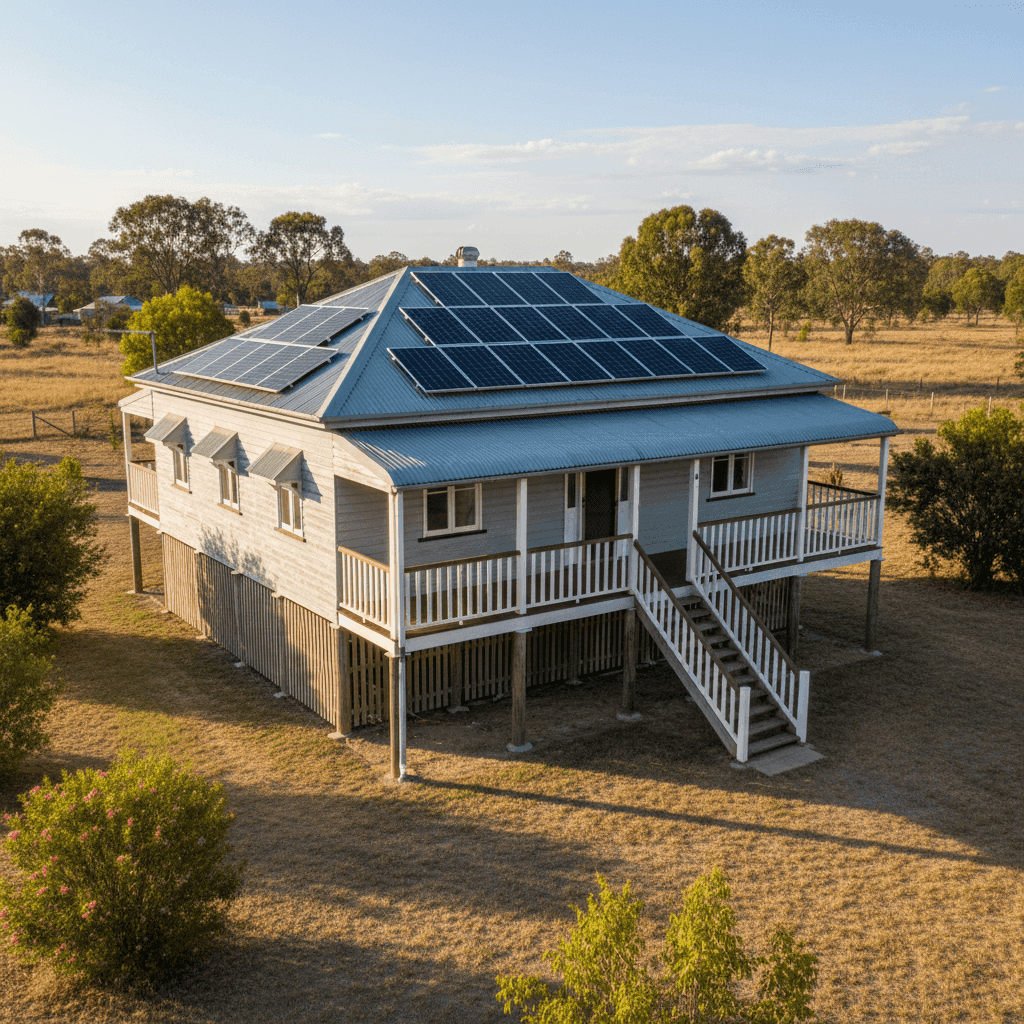

Age and Construction (1930, Fibro Asbestos Walls)

This is the most significant risk factor. A home built in 1930 is nearly a century old, and fibro asbestos cladding — common in Australian homes of that era — introduces both structural and health-related considerations for insurers. Replacement costs are higher, trades need to be licensed asbestos-removal specialists, and the risk of deterioration is greater. Most insurers load premiums accordingly, so the below-average rating here is notable.

Elevated on Stumps

Being elevated by at least one metre on stumps is a classic feature of older Queensland homes, and it works in the homeowner's favour from a flood and storm surge perspective. Water is less likely to inundate the living areas, which reduces the insurer's exposure for weather events. This elevation, combined with the absence of a cyclone risk classification, meaningfully reduces the risk profile.

Steel / Colorbond Roof

Colorbond roofing is generally viewed favourably by insurers. It's durable, fire-resistant, and lower maintenance than older corrugated iron or tile alternatives. For a home of this age, having a modern metal roof is a genuine premium-reducing factor.

Solar Panels

Solar panels are now covered under most standard home insurance policies in Australia, but their presence does add to the sum insured. Panels can be damaged by hail, storms, or fire, and replacement costs are not trivial. Homeowners should confirm that their policy explicitly covers solar panel damage and check whether inverters and mounting hardware are included.

Ducted Climate Control

Ducted air conditioning systems are expensive to repair or replace and are typically included in the building sum insured. Their presence supports the $458,000 building valuation and is a reasonable inclusion for a property of this size and fit-out.

Building Size (123 sqm)

At 123 square metres, this is a modest home. The sum insured of $458,000 implies a rebuild cost of approximately $3,724 per sqm — which is on the higher end but not unreasonable for a home with specialised construction materials (asbestos remediation during a rebuild significantly inflates costs).

---

Tips for Homeowners in Wowan

1. Review your asbestos disclosure carefully When insuring a fibro asbestos home, make sure your insurer is fully aware of the wall construction. Failing to disclose this accurately could result in a claim being reduced or denied. Ask your insurer specifically how asbestos removal and disposal costs are treated under the policy.

2. Get a professional rebuild cost assessment The $458,000 sum insured needs to be accurate. Older homes with non-standard materials are notoriously difficult to value. Consider commissioning a professional quantity surveyor or using a recognised building cost calculator to verify the figure — underinsurance is a real and costly risk.

3. Consider your excess strategy The $5,000 building excess on this policy is high. While it reduces the annual premium, it means you'd need to absorb the first $5,000 of any building claim yourself. If you have a solid emergency fund, this can be a smart trade-off. If not, it may be worth comparing quotes with a lower excess to understand the premium difference.

4. Check your contents cover At $10,000, the contents sum insured is quite low. Even in a modest 2-bedroom home, furniture, appliances, clothing, and personal items can easily exceed this figure. Do a room-by-room audit to make sure you're not underinsured on contents — it's one of the most common and easily avoidable mistakes Australian homeowners make.

---

Compare and Save with CoverClub

Whether you're a first-time buyer in regional Queensland or reviewing your existing policy, getting a second opinion on your premium is always worthwhile. Compare home insurance quotes at CoverClub to see what other insurers would charge for your property — it takes just a few minutes and could save you hundreds of dollars a year. With Queensland premiums among the highest in the country, even a small saving adds up fast.