If you own a free standing home in Wurtulla, QLD 4575, you're living in one of the Sunshine Coast's most sought-after pockets — a relaxed coastal suburb with easy access to Bokarina Beach, Currimundi Lake, and the broader Sunshine Coast lifestyle. But coastal living comes with its own insurance considerations, and understanding what you should be paying for home and contents cover is an important part of protecting your investment.

This article breaks down a real insurance quote for a five-bedroom, three-bathroom free standing home in Wurtulla, comparing it against local, state, and national benchmarks to help you decide whether your premium is money well spent — or money left on the table.

---

Is This Quote Fair?

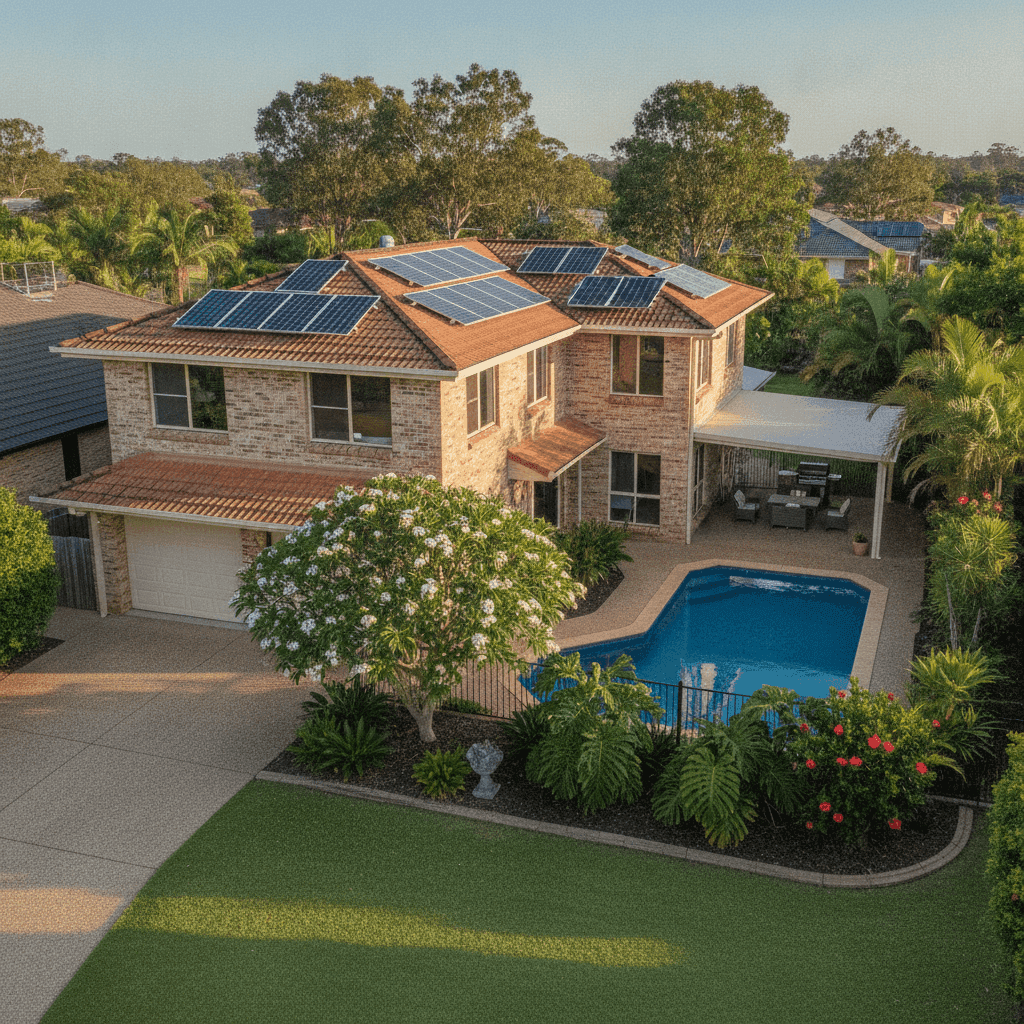

The quote in question sits at $4,018 per year (or $382/month) for combined home and contents insurance, covering a building sum insured of $1,025,000 and contents valued at $185,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. At $4,018/yr, this premium lands comfortably within the middle range of what Wurtulla homeowners are paying. It sits above the suburb's 25th percentile ($2,797/yr) but well below the 75th percentile ($4,314/yr), meaning roughly half of comparable properties in the area are paying less — but a meaningful proportion are paying more.

For a property of this size and specification — 214 sqm, double brick construction, tiled roof, slab foundation, with a pool, solar panels, and ducted climate control — a premium in this range is broadly reasonable. That said, "fair" doesn't mean you can't do better.

---

How Wurtulla Compares

Understanding your premium in context is key. Here's how this quote stacks up against broader benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $4,018/yr |

| Wurtulla Suburb Average | $3,659/yr |

| Wurtulla Suburb Median | $3,908/yr |

| Sunshine Coast LGA Average | $7,249/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

Based on [Wurtulla suburb data](https://coverclub.com.au/stats/QLD/4575/wurtulla) from 9 quotes, [QLD state data](https://coverclub.com.au/stats/QLD), and [national benchmarks](https://coverclub.com.au/stats/national).

A few things stand out here. The QLD state average of $9,129/yr is dramatically higher than both this quote and the suburb median — this is largely driven by high-risk flood and cyclone zones elsewhere in Queensland, such as Far North QLD and parts of South East QLD prone to flooding. Wurtulla, notably, is not classified as a cyclone risk area, which is a significant factor keeping premiums more manageable in this suburb.

The national average of $5,347/yr is also higher than this quote, again reflecting the influence of high-risk postcodes across Australia. When compared to the national median of $2,764/yr, this quote is above the midpoint — but that's expected given the property's size, value, and features.

Within Wurtulla itself, this quote is slightly above both the suburb average ($3,659/yr) and median ($3,908/yr), which suggests there may be some room to shop around — particularly if the insurer's policy terms and inclusions align closely with what competitors are offering.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium calculated. Here's what matters most:

Double Brick Construction Double brick walls are generally viewed favourably by insurers. They offer strong resistance to fire and impact damage, and tend to perform well in severe weather events. This construction type can contribute to lower premiums compared to lightweight or timber-framed alternatives.

Tiled Roof Concrete or terracotta tile roofs are considered a low-to-moderate risk by most Australian insurers. They're durable and fire-resistant, though they can be susceptible to hail damage. Given Wurtulla's coastal location, this is worth keeping in mind.

Slab Foundation A concrete slab foundation is standard for Queensland homes built in the 1990s and is generally neutral in terms of insurance risk — it avoids the underfloor moisture issues sometimes associated with older timber stumped homes.

Swimming Pool A pool increases the insured value of the property and introduces liability considerations, both of which contribute to a higher premium. Ensuring your policy includes adequate liability cover for pool-related incidents is essential.

Solar Panels Solar panels add to the replacement cost of the building and are typically included under building cover. With a 214 sqm home likely sporting a reasonably sized system, this adds to the sum insured and, by extension, the premium.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset and are covered under building insurance. Their replacement cost is factored into the building sum insured of $1,025,000.

Building Age (1995) At around 30 years old, this home is well past its initial build phase but not yet in the bracket where significant wear-related risk is flagged. Provided the property has been well maintained, age is unlikely to be a major premium driver here.

---

Tips for Homeowners in Wurtulla

1. Review your sum insured annually Construction costs on the Sunshine Coast have risen considerably over recent years. Make sure your $1,025,000 building sum insured reflects current rebuild costs — not what it would have cost five or ten years ago. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Shop around — even if your quote seems fair A "fair" rating means you're not being gouged, but it doesn't mean you're getting the best deal available. Insurers price risk differently, and a quote that's competitive with your suburb median from one provider could be significantly cheaper from another. Use CoverClub's quote comparison tool to see what else is available for your property.

3. Check your contents cover is adequate $185,000 in contents cover is a reasonable starting point for a five-bedroom home, but it's worth doing a proper audit of your belongings — furniture, appliances, clothing, jewellery, electronics, and outdoor items like pool equipment and outdoor furniture. Many homeowners discover they're underinsured on contents after a claim.

4. Ask about discounts for security and safety features Some insurers offer premium discounts for properties with monitored alarm systems, deadbolts, and other security measures. If your home has these features, make sure your insurer knows — it could reduce your annual premium.

---

Compare Your Home Insurance with CoverClub

Whether you're reviewing an existing policy or shopping for cover on a new property, CoverClub makes it easy to understand what you should be paying and find a deal that works for your budget. Get a home insurance quote today and see how your premium stacks up against real data from homeowners in Wurtulla and across Australia. You might be surprised at what a difference comparing quotes can make.