Wyoming is a well-established residential suburb on the Central Coast of New South Wales, sitting within the City of Gosford area of the Central Coast Council. Known for its leafy streets and proximity to Gosford's amenities, it's a popular choice for families — and the housing stock reflects that, with many solid, older-era homes on generous blocks. This article breaks down a real home insurance quote for a four-bedroom, free-standing home in Wyoming (postcode 2250), examining whether the price stacks up against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes to $4,676 per year (or $448/month) for combined home and contents cover, with a building sum insured of $750,000 and contents valued at $180,000. Both the building and contents excess are set at $1,000.

Our pricing analysis rates this quote as Expensive — above average for the area.

To put that in context: the suburb average premium in Wyoming sits at $3,301/year, and the median is $3,457/year. This quote lands well above the 75th percentile for the suburb, which is $4,050/year — meaning it's pricier than at least three-quarters of comparable quotes in the area.

That said, "expensive" doesn't automatically mean "wrong." A higher sum insured, above-average fittings quality, and specific property features can all legitimately push a premium upward. The key question is whether you're getting adequate cover for what you're paying — and whether shopping around could yield a better deal for the same level of protection.

---

How Wyoming Compares

Understanding where Wyoming sits in the broader insurance landscape helps put this quote in perspective. Here's a snapshot based on data from Wyoming (NSW 2250) suburb stats:

| Benchmark | Annual Premium |

|---|---|

| This quote | $4,676 |

| Wyoming suburb average | $3,301 |

| Wyoming suburb median | $3,457 |

| Wyoming 75th percentile | $4,050 |

| NSW state average | $9,528 |

| NSW state median | $3,770 |

| National average | $5,347 |

| National median | $2,764 |

| Hawkesbury LGA average | $10,350 |

A few things stand out here. First, the NSW state average of $9,528 is dramatically higher than the Wyoming suburb average — this is largely driven by high-risk areas like flood-prone regions in the Hunter Valley and parts of western Sydney, which skew the state figure significantly. The NSW median of $3,770 is a more reliable indicator of what most homeowners pay, and it's actually quite close to Wyoming's own median.

At the national level, the average of $5,347 is above this quote, but again, the national median of $2,764 tells a different story — reflecting just how much high-risk properties inflate the averages.

Interestingly, the Hawkesbury LGA average of $10,350 is an outlier, driven by the region's well-documented flood risk. Wyoming, by contrast, is a comparatively lower-risk suburb, which helps explain why local premiums are more moderate.

The bottom line: this quote is above average for Wyoming, even if it looks reasonable against some broader benchmarks.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium calculated. Here's what insurers are likely factoring in:

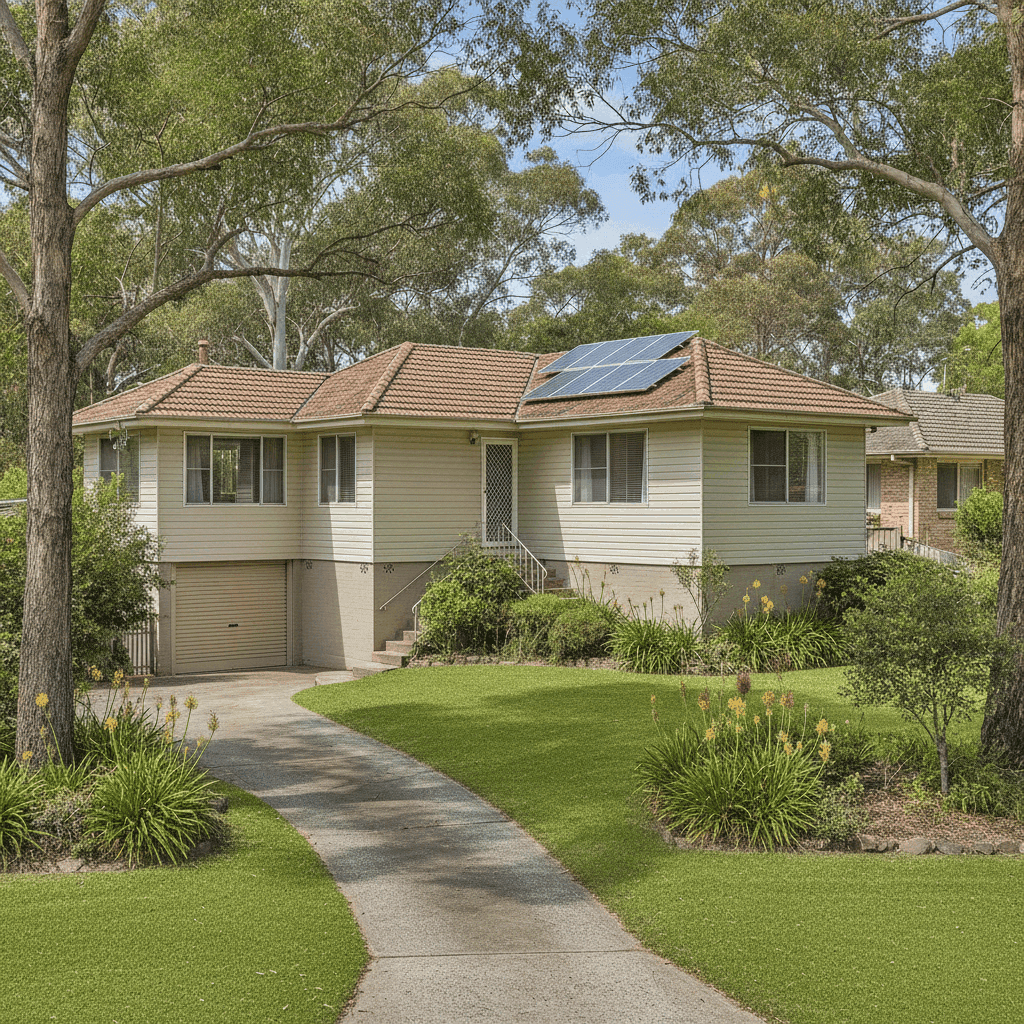

Age of construction (1975): Homes built in the mid-1970s are now approaching 50 years old. While many are structurally sound, older properties can carry higher rebuild risk due to outdated wiring, plumbing, and materials that may not meet current building codes. Insurers often price this in.

Vinyl cladding external walls: Vinyl cladding is generally considered a moderate-risk wall material. It's not as fire-resistant as brick veneer, and some insurers apply loadings for non-masonry construction. This can contribute to a higher premium compared to a brick home of similar size.

Tiled roof: A tiled roof is typically viewed favourably by insurers — tiles are durable, fire-resistant, and long-lasting. This likely works in the homeowner's favour when it comes to pricing.

Stump foundation: Homes on stumps (also known as pier and beam foundations) are common in older Australian properties. They can be more vulnerable to movement, pest damage, and moisture-related issues over time, which some insurers treat as an elevated risk factor.

Timber and laminate flooring: These floor types are generally straightforward to insure but can be costly to replace, which may influence the contents and building valuation.

Solar panels: The presence of solar panels adds value to the property and increases the cost of reinstatement if the home were to be damaged or destroyed. Insurers need to account for the replacement cost of the system, which can nudge premiums upward.

Ducted climate control: Ducted systems are expensive to install and replace. Like solar panels, their inclusion in the building's insured value is appropriate — but it does mean the sum insured (and therefore the premium) will be higher.

Above-average fittings quality: This is a significant factor. Premium fittings — think stone benchtops, quality cabinetry, high-end appliances and fixtures — cost more to replace like-for-like. Insurers price this accordingly, and it's one of the more likely contributors to this quote sitting above the suburb average.

Building size (214 sqm): At 214 square metres, this is a reasonably sized home. Rebuild costs scale with floor area, and a $750,000 sum insured for a 214 sqm home with above-average fittings is broadly reasonable for the Central Coast market.

---

Tips for Homeowners in Wyoming

If you're a Wyoming homeowner reviewing your insurance, here are some practical steps worth taking:

- Review your sum insured annually. Construction costs have risen sharply in recent years across NSW. Make sure your building sum insured reflects current rebuild costs — not what you paid for the property or what it's worth on the market. Underinsurance is a real risk, particularly for older homes with quality fittings.

- Shop around at renewal time. Loyalty doesn't always pay in insurance. Premiums can vary significantly between insurers for the same property and cover level. Use a comparison tool like CoverClub to benchmark your renewal quote before accepting it.

- Ask about discounts for security and safety features. Some insurers offer reduced premiums for homes with monitored alarms, deadbolts, smoke detectors, and similar features. It's worth asking your insurer directly what discounts may apply to your property.

- Consider your excess level carefully. This quote carries a $1,000 excess on both building and contents. Opting for a higher excess (say, $2,000 or $2,500) can meaningfully reduce your annual premium — a worthwhile trade-off if you have the financial buffer to cover a larger out-of-pocket cost in the event of a claim.

---

Compare Your Quote Today

Whether you're renewing an existing policy or taking out cover for the first time, it pays to know what the market looks like. CoverClub aggregates real quote data from across Australia, so you can see exactly how your premium stacks up against your neighbours and the broader market. Get a quote and compare — it takes just a few minutes and could save you hundreds of dollars a year.