Yamba is one of New South Wales' most beloved coastal towns — a relaxed, sun-drenched community at the mouth of the Clarence River that consistently ranks among Australia's best places to live. But living in paradise comes with its own set of insurance considerations. This article breaks down a real home and contents insurance quote for a two-bedroom free standing home in Yamba (postcode 2464), examining how the premium stacks up against local, state, and national benchmarks — and what property owners in the area should know before renewing or switching their cover.

---

Is This Quote Fair?

The quote in question came in at $1,659 per year (or $162/month) for combined home and contents cover, with a building sum insured of $650,000 and contents valued at $50,000. The building excess is $2,000 and the contents excess is $1,000.

Our price rating for this quote is CHEAP — below average — and the data backs that up convincingly.

When you compare this figure against the Yamba suburb average of $8,684/yr, this quote is sitting at roughly 19% of what most Yamba homeowners are paying. Even measured against the suburb's median premium of $5,058/yr, this quote is less than a third of the typical cost. That's a genuinely exceptional outcome for a property in this postcode.

It's worth noting that the Yamba insurance market is unusually wide — premiums range from around $2,493/yr at the 25th percentile all the way up to $10,276/yr at the 75th percentile. That's a massive spread, which tells us that insurers are pricing risk very differently in this area. Getting a quote this far below the median is a strong result by any measure.

---

How Yamba Compares

To put this quote in full context, here's how Yamba's insurance costs compare to broader benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Yamba (2464) | $8,684/yr | $5,058/yr |

| Clarence Valley LGA | $6,052/yr | — |

| NSW | $3,801/yr | $3,410/yr |

| National | $2,965/yr | $2,716/yr |

Yamba sits significantly above both state and national averages — the suburb average is more than double the NSW average, and nearly three times the national median. This reflects the elevated risk profile of coastal NSW properties, where flooding, storm surge, and severe weather events are meaningful concerns for insurers.

The Clarence Valley LGA average of $6,052/yr also confirms that this isn't just a Yamba-specific quirk — the broader region carries higher-than-average insurance costs. Based on a sample of 92 quotes in the suburb, these figures are statistically meaningful, not just outliers skewing the numbers.

The quote analysed here — at $1,659/yr — sits well below even the national average, which makes it a standout result for a coastal property in a high-risk LGA.

---

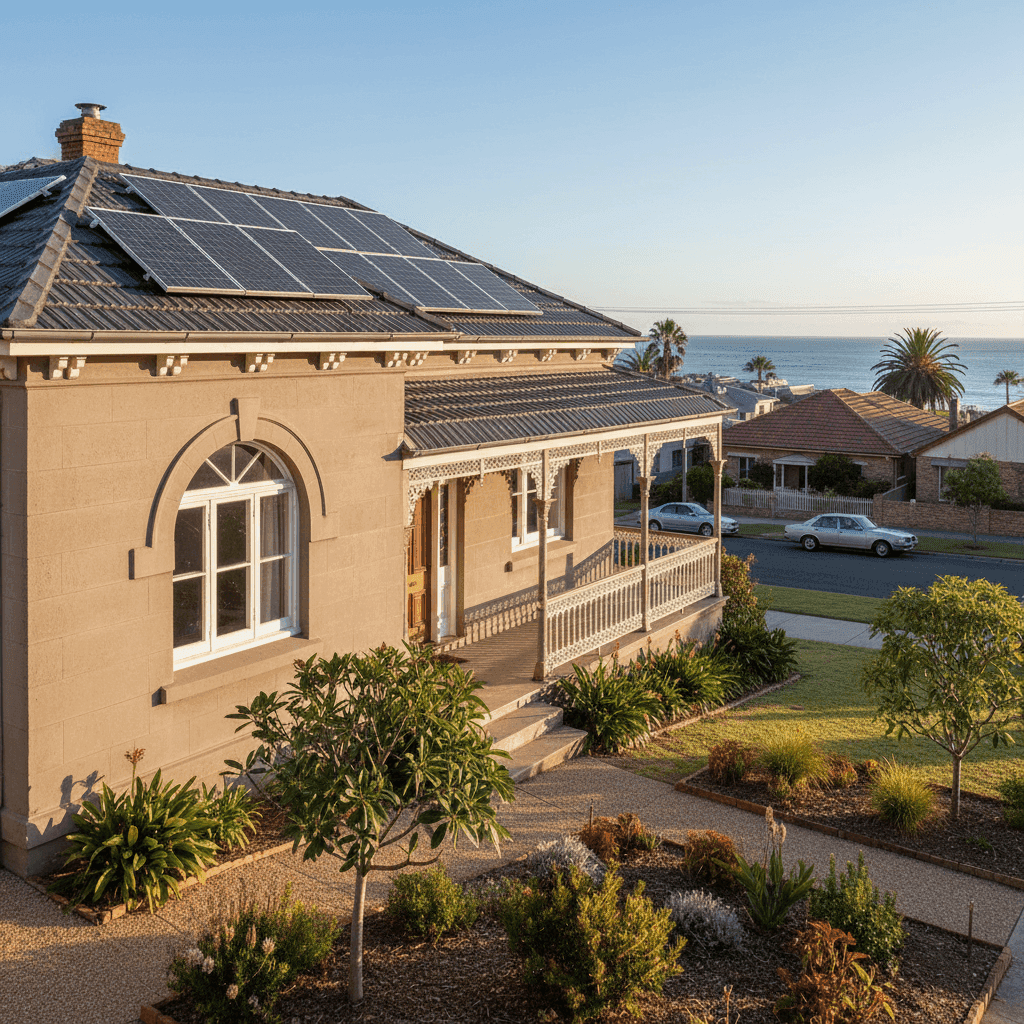

Property Features That Affect Your Premium

Several characteristics of this property likely contributed to the favourable premium outcome.

Concrete construction is one of the most significant factors. Both the external walls and the roof are concrete, which is highly resistant to fire, storm damage, and general wear. Insurers typically reward this with lower premiums compared to timber-framed or clad homes, which are more vulnerable to fire and termite damage.

Slab foundation is another positive. Homes built on concrete slabs tend to be more structurally stable and less susceptible to certain types of subsidence or underfloor moisture issues that can affect pier-and-beam or suspended floor homes.

Tile flooring throughout the home is durable and low-maintenance — less likely to suffer significant damage from minor water ingress compared to timber or carpet, which can reduce the likelihood of contents claims.

No pool removes one of the more common liability and property risk factors that insurers factor into premiums.

Solar panels are present on this property. While they add value and are worth insuring, they can sometimes add a small amount to premiums due to the replacement cost and the risk of damage during storms. It's important to confirm with your insurer that solar panels are explicitly covered under your policy.

The heritage overlay on this property is worth paying close attention to. Heritage-listed or heritage-overlay properties can be more expensive to repair or rebuild because they may require specialist tradespeople, heritage-approved materials, or council approval for works. Homeowners should ensure their sum insured of $650,000 genuinely reflects the cost of rebuilding to heritage standards — not just standard construction rates.

The property was built in 1987, which means it's approaching 40 years old. Older homes can carry higher risk of aging infrastructure — plumbing, electrical wiring, and roofing materials — so it's worth having these systems inspected periodically to avoid claim complications.

The building size of 130 sqm is relatively modest, which helps keep the sum insured and the resulting premium manageable.

---

Tips for Homeowners in Yamba

1. Review your sum insured carefully — especially given the heritage overlay. Heritage-listed or heritage-overlay homes are often more expensive to rebuild than standard properties. Make sure your $650,000 sum insured accounts for heritage-compliant materials and labour costs. Underinsurance is a common and costly mistake — if your rebuild cost exceeds your sum insured, you'll be covering the gap yourself.

2. Confirm that your solar panels are covered. Solar panels are a valuable asset but aren't always automatically covered under standard home insurance policies. Check your Product Disclosure Statement (PDS) to confirm they're included, and that the coverage extends to storm and hail damage — both of which are genuine risks in coastal NSW.

3. Compare quotes annually — the Yamba market is highly variable. With premiums in this suburb ranging from under $2,500 to over $10,000 per year, there's clearly enormous variation between insurers. The quote analysed here proves that significant savings are possible. Use CoverClub to compare quotes each year at renewal rather than simply auto-renewing with your existing provider.

4. Understand your flood and storm cover. Yamba's location near the Clarence River mouth and the Pacific coast means flood and storm surge are real risks. Not all policies treat "flood" and "storm" the same way — some policies exclude riverine flooding while covering storm-related inundation. Read your PDS carefully and ask your insurer directly about what flood scenarios are and aren't covered.

---

Get a Quote for Your Yamba Home

Whether you're a long-time Yamba local or a recent arrival, it pays to make sure your home insurance is working as hard as you are. The quote analysed here shows that genuinely competitive pricing is available in this market — even for a coastal property in a higher-risk postcode.

Compare home and contents quotes for your Yamba property at CoverClub and see how your current premium stacks up against the latest suburb data. It only takes a few minutes, and the savings could be substantial.