Yandina Creek is a leafy, semi-rural locality nestled in the Sunshine Coast hinterland of Queensland — a region that blends relaxed country living with proximity to the Sunshine Coast's beaches and amenities. It's an increasingly popular area for families and tree-changers, but like much of coastal and hinterland Queensland, home insurance here carries a premium that reflects the region's unique risk profile. This article breaks down a real home and contents insurance quote for a four-bedroom, free-standing home in Yandina Creek (postcode 4561), and puts the numbers into context so you can make a more informed decision about your own cover.

---

Is This Quote Fair?

The quote in question comes in at $7,697 per year (or $770/month) for a combined home and contents policy, covering a building sum insured of $1,811,000 and contents valued at $101,000. The building excess is $2,000 and the contents excess $600.

Our pricing engine has rated this quote as Fair — Around Average, and the data backs that up. Based on 21 quotes collected for Yandina Creek (4561), the suburb's median premium sits at $7,442/year — meaning this quote is just $255 above the midpoint. It falls comfortably within the interquartile range (between the 25th percentile of $5,699 and the 75th percentile of $8,595), which is the band where most typical quotes land.

In other words, this isn't a bargain, but it's not an outlier either. For a large, elevated, pole-frame home on the Sunshine Coast hinterland with a high building sum insured, a figure in this range is broadly in line with what insurers are pricing for similar properties in the area.

---

How Yandina Creek Compares

To understand why this quote sits where it does, it helps to zoom out and look at the broader picture.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Yandina Creek (4561) | $10,187/yr | $7,442/yr |

| Sunshine Coast LGA | $7,249/yr | — |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

The gap between Yandina Creek and the Queensland state average is striking — local premiums are running at roughly 1.7× the state average, and more than 2.5× the [national median](https://coverclub.com.au/stats/national). This is not unusual for Sunshine Coast hinterland properties. Insurers factor in flood exposure (parts of the Mary River catchment and its tributaries are nearby), storm and severe weather risk, and the higher rebuild costs associated with elevated, custom-built homes on larger rural blocks.

It's also worth noting that the suburb average of $10,187 is pulled upward by some very high quotes in the dataset — likely properties with higher sums insured or greater flood/storm exposure. The median of $7,442 is a more representative figure for a "typical" Yandina Creek property, and this quote sits just above that line.

---

Property Features That Affect Your Premium

Several characteristics of this particular home have a meaningful influence on what insurers charge:

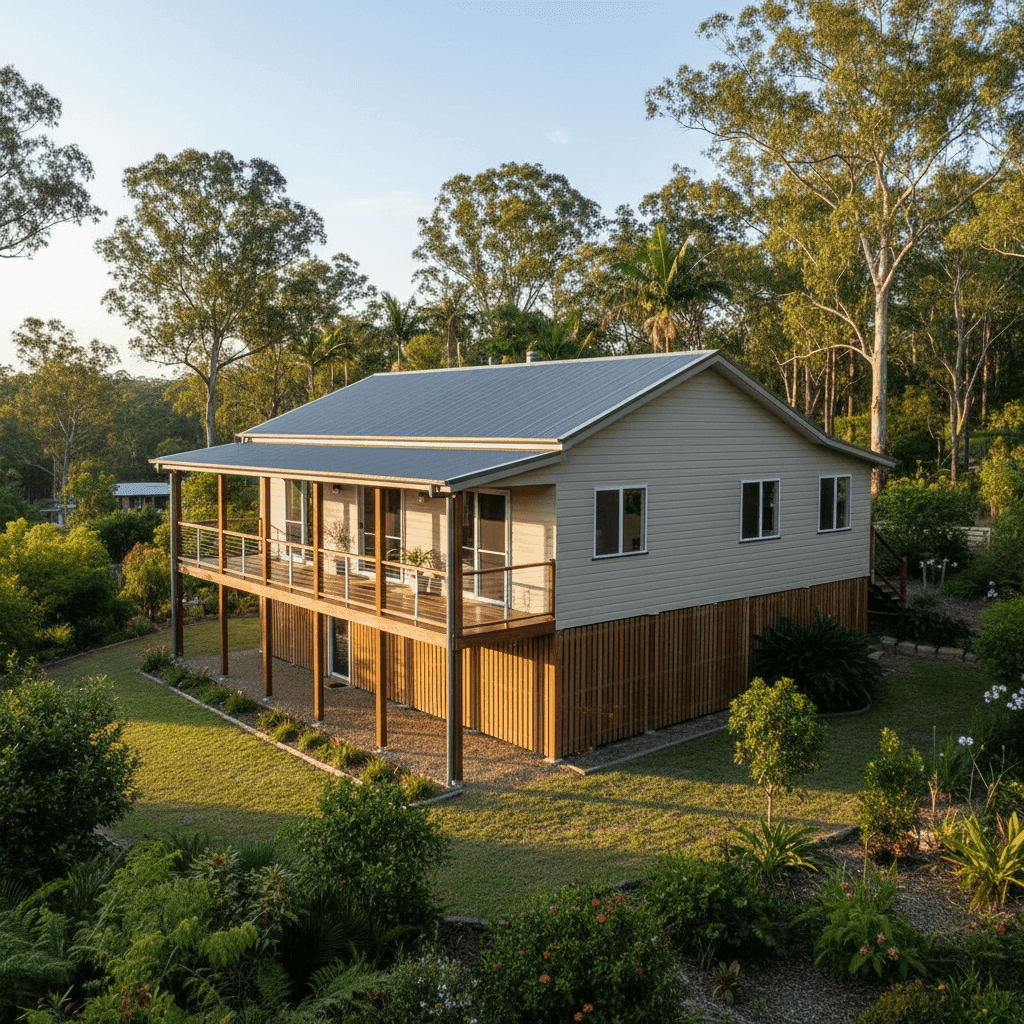

Elevated pole foundation (at least 1 metre) This is one of the most significant rating factors. Pole-frame, elevated homes — common throughout Queensland's hinterland — are more expensive to repair and rebuild than slab-on-ground construction. The elevated design can reduce flood inundation risk to the living areas, but the structural complexity adds to rebuild costs, which is reflected in both the high sum insured ($1,811,000) and the premium.

Hardiplank / Hardiflex external walls Fibre cement cladding like Hardiplank is durable and relatively fire-resistant, which insurers generally view favourably compared to weatherboard or other timber cladding. It's a neutral-to-positive factor for premium pricing.

Steel / Colorbond roof Metal roofing is well-regarded by insurers for its resilience against storm damage and fire. In a region that sees significant summer storm activity, this is a genuine positive for your risk profile.

Timber and laminate flooring Timber floors in elevated homes can be susceptible to moisture and require specialist repair after water ingress events. This is a minor risk factor that some insurers price into their assessments.

Large building size (268 sqm) and high sum insured At $1,811,000, the building sum insured is substantial. This reflects the cost of rebuilding a large, elevated, custom-quality home in a regional area where trades and materials can carry a premium. A higher sum insured directly increases the base premium — this is one of the primary drivers of the overall cost.

No pool, no solar panels The absence of a pool and solar panels removes two common sources of additional premium loading, which helps keep the quote from climbing further.

---

Tips for Homeowners in Yandina Creek

1. Review your sum insured regularly — but don't underinsure Construction costs in Queensland have risen sharply in recent years. While it might be tempting to lower your building sum insured to reduce premiums, being underinsured at claim time can be financially devastating. Use an independent building cost calculator (such as the one provided by the Housing Industry Association) to verify your figure annually.

2. Ask about flood cover specifically Not all standard home insurance policies automatically include flood cover, and definitions vary between insurers. Given Yandina Creek's proximity to creek and waterway systems, confirm explicitly whether your policy covers riverine flood, flash flooding, and storm surge — and what the excess is for flood claims.

3. Compare quotes before renewal The spread of premiums in Yandina Creek is wide — from $5,699 at the 25th percentile to $8,595 at the 75th percentile. That's a potential saving of nearly $3,000 per year for comparable cover. Insurers price the same property very differently, so shopping around at renewal is one of the most effective ways to manage your insurance costs.

4. Consider your excess settings A $2,000 building excess is on the higher side. Adjusting your excess up or down will directly affect your premium — but make sure you're comfortable covering that amount out of pocket in the event of a claim. For contents, the $600 excess is fairly standard.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for cover on a new property, CoverClub makes it easy to see how your quote stacks up. Get a home insurance quote today and compare it against real data from your suburb, your region, and across Australia. You can also explore the latest Yandina Creek insurance statistics to see how premiums in your area are trending over time.