Yeppoon is one of Queensland's most appealing coastal communities — a relaxed seaside town on the Capricorn Coast that draws families and retirees alike. But living close to the coast in Central Queensland comes with its own set of insurance considerations. This article takes a close look at a recent home and contents insurance quote for a four-bedroom, free-standing home in Yeppoon (QLD 4703), comparing it against local, state, and national benchmarks to help you understand whether you're getting a fair deal.

---

Is This Quote Fair?

The quote in question comes in at $4,916 per year (or $464/month) for combined home and contents cover, with a building sum insured of $1,200,000 and contents valued at $150,000. Both the building and contents excesses are set at $1,000.

Our pricing engine has rated this quote as FAIR — Around Average.

That assessment holds up when you look at the numbers. The suburb average for Yeppoon sits at $4,584/year, and the median is $4,372/year. This quote lands above both of those figures, but it's well within the suburb's interquartile range — the 25th percentile is $3,414/year and the 75th percentile is $5,370/year. In other words, roughly half of comparable Yeppoon quotes fall between those two figures, and this one sits comfortably in that middle band.

It's not the cheapest quote you could find in the suburb, but it's far from an outlier. Given the property's features (more on those below), a premium in this range is broadly reasonable.

---

How Yeppoon Compares

To put this quote in proper context, it helps to zoom out and look at the bigger picture. You can explore the full data on the Yeppoon suburb stats page, the Queensland state stats page, and the national stats page.

Here's a quick snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Yeppoon (suburb) | $4,584/yr | $4,372/yr |

| Livingstone LGA | $13,146/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, the Livingstone LGA average of $13,146/year is strikingly high — significantly above both the Yeppoon suburb average and the state average. This suggests there are properties within the broader Livingstone local government area that attract very high premiums, likely due to elevated risk profiles (think beachfront or flood-prone locations). Yeppoon's suburb-level data is more representative of typical residential streets in the town.

Second, the Queensland state average of $9,129/year is well above the national average of $5,347/year — a reflection of the elevated natural hazard risks across much of the state, including cyclones, flooding, and storms. However, the QLD median of $3,903/year tells a different story: the average is being pulled upward by a relatively small number of very high-risk properties. For a typical Yeppoon home, premiums in the $4,000–$5,500 range appear to be the norm.

This quote, at $4,916/year, sits above the national median of $2,764/year but below the national average of $5,347/year — a reasonable position for a coastal Queensland property.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on its insurance cost.

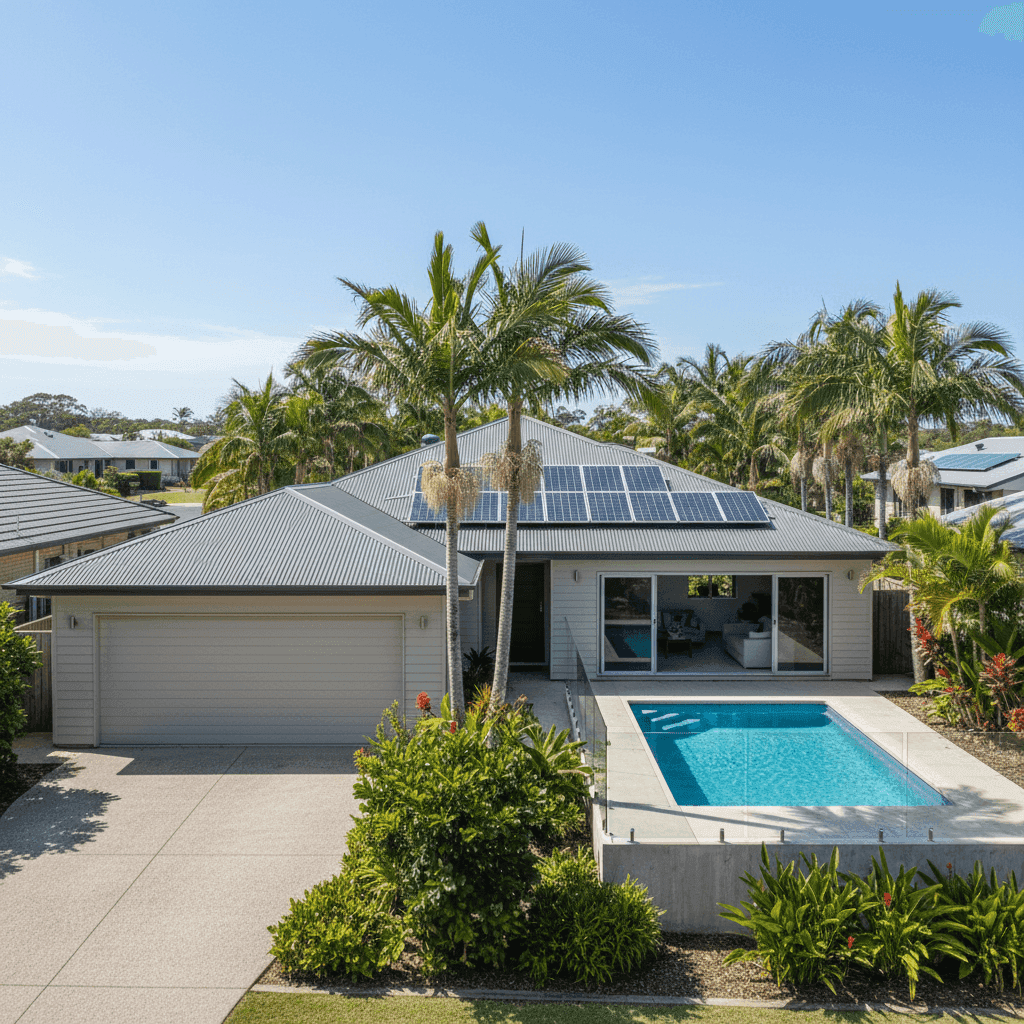

Cyclone risk area: Yeppoon sits within a designated cyclone risk zone. This is arguably the single biggest premium driver for homes in this region. Insurers apply cyclone-specific loadings to properties in these areas, which is why Queensland coastal premiums tend to run higher than those in southern states.

Weatherboard wood external walls: Timber-clad homes are generally considered higher risk than brick veneer or double-brick construction, as they are more susceptible to fire spread and wind damage. This can contribute to a higher premium compared to masonry alternatives.

Steel/Colorbond roof: On the positive side, a Colorbond steel roof is well-regarded by insurers in cyclone-prone areas. It's durable, resistant to uplift when properly installed, and less likely to fail than older tile roofs during high-wind events. This may help offset some of the premium loading associated with timber walls.

Slab foundation: A concrete slab is a stable, low-risk foundation type that generally doesn't attract any negative premium loading.

Swimming pool: Pools add to the replacement cost of a property and introduce some liability considerations, both of which can nudge premiums upward.

Solar panels: Rooftop solar systems increase the insured value of the home and can be a complicating factor in storm or hail claims. It's worth confirming with your insurer that your solar system is explicitly covered under your policy.

Ducted climate control: Ducted air conditioning systems are a significant fixture that adds to the building's replacement value, and are worth ensuring are included in your sum insured calculation.

Building size (235 sqm) and sum insured ($1,200,000): A $1.2 million building sum insured for a 235 sqm home built in 2009 works out to roughly $5,100 per square metre — on the higher end, but not unreasonable given construction costs in regional Queensland, the quality of inclusions (ducted AC, pool, solar), and the need to account for full rebuild costs including site clearance, professional fees, and current material prices.

---

Tips for Homeowners in Yeppoon

1. Review your sum insured regularly. Construction costs have risen sharply in recent years. If your building sum insured hasn't been updated since you took out the policy, there's a real risk of being underinsured. Use a building cost calculator or speak to a local builder to get a realistic current rebuild estimate — don't just rely on the property's market value.

2. Ask about cyclone mitigation discounts. Some insurers offer premium reductions for homes that have been assessed or upgraded to improve cyclone resilience — things like cyclone straps on roof trusses, impact-resistant windows, or a formal building inspection under a program like Resilient Homes. It's worth asking your insurer directly.

3. Check that your solar and pool are explicitly covered. Both solar panels and swimming pools can sometimes fall into grey areas in standard home policies. Read your Product Disclosure Statement (PDS) carefully and confirm with your insurer that these features are covered for storm damage, hail, and accidental damage.

4. Compare quotes before renewal. The insurance market in Queensland is competitive and premiums can vary significantly between providers for the same property. Don't let your policy auto-renew without shopping around — even a FAIR-rated quote might be bettered by another insurer offering equivalent cover at a lower price.

---

Ready to Compare?

Whether you're renewing your existing policy or insuring a new property, it pays to see what the broader market has to offer. Get a home insurance quote at CoverClub and compare your options in minutes — no jargon, no pressure, just clear pricing data to help you make a confident decision.