Yeppoon is one of Queensland's most attractive coastal destinations — a relaxed beachside community on the Capricorn Coast, roughly 40 kilometres from Rockhampton. It's a popular spot for families and retirees alike, drawn by the lifestyle, the proximity to the Great Barrier Reef, and the relative affordability compared to Southeast Queensland. But living in paradise comes with its own set of insurance considerations, particularly when it comes to protecting a substantial family home. This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom free-standing home in Yeppoon (postcode 4703) and puts it into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium on this quote comes in at $3,621 per year (or $343 per month), covering both building and contents. The building is insured for $889,000 and contents for $195,000 — a combined coverage position that reflects a well-appointed, mid-to-large family home.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. Within the Yeppoon suburb, the average annual premium sits at $4,584 and the median at $4,372. This quote lands comfortably below both figures, placing it between the 25th percentile ($3,414/yr) and the median — meaning it's better than at least half of comparable quotes in the area, but not quite in bargain territory.

In practical terms, this is a reasonable outcome for a property of this size, construction type, and location. Yeppoon sits in a designated cyclone risk zone, which is one of the most significant premium drivers in coastal Queensland. The fact that this quote is tracking below the local average suggests the insurer has assessed the specific risk profile of this property favourably — likely assisted by its relatively modern construction (built in 2010), solid brick veneer walls, and Colorbond steel roof.

---

How Yeppoon Compares

To properly contextualise this quote, it helps to zoom out and look at the broader picture. You can explore the full breakdown on our Yeppoon suburb stats page.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,621 |

| Yeppoon Suburb Average | $4,584 |

| Yeppoon Suburb Median | $4,372 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

| Livingstone LGA Average | $13,146 |

A few things stand out here. The Queensland state average of $9,129 per year is dramatically higher than the state median of $3,903 — a classic sign that a relatively small number of very high-risk properties (think flood-prone or extreme cyclone zones in Far North Queensland) are pulling the average upward significantly. This quote sits below the QLD median, which is a solid result.

The Livingstone LGA average of $13,146 is particularly eye-catching. The Local Government Area encompasses a range of properties with varying risk profiles, and the high average likely reflects some particularly exposed coastal or flood-risk properties within the LGA dragging that figure up. Yeppoon's suburb-level data is a more meaningful comparison for this specific property.

At the national level, the average of $5,347 reflects the diversity of risk across Australia — from low-risk suburban Melbourne to cyclone-prone Cairns. This Yeppoon quote sits well below the national average, which is a positive outcome for a coastal Queensland home.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Understanding these can help you make sense of your quote — and potentially improve your position at renewal.

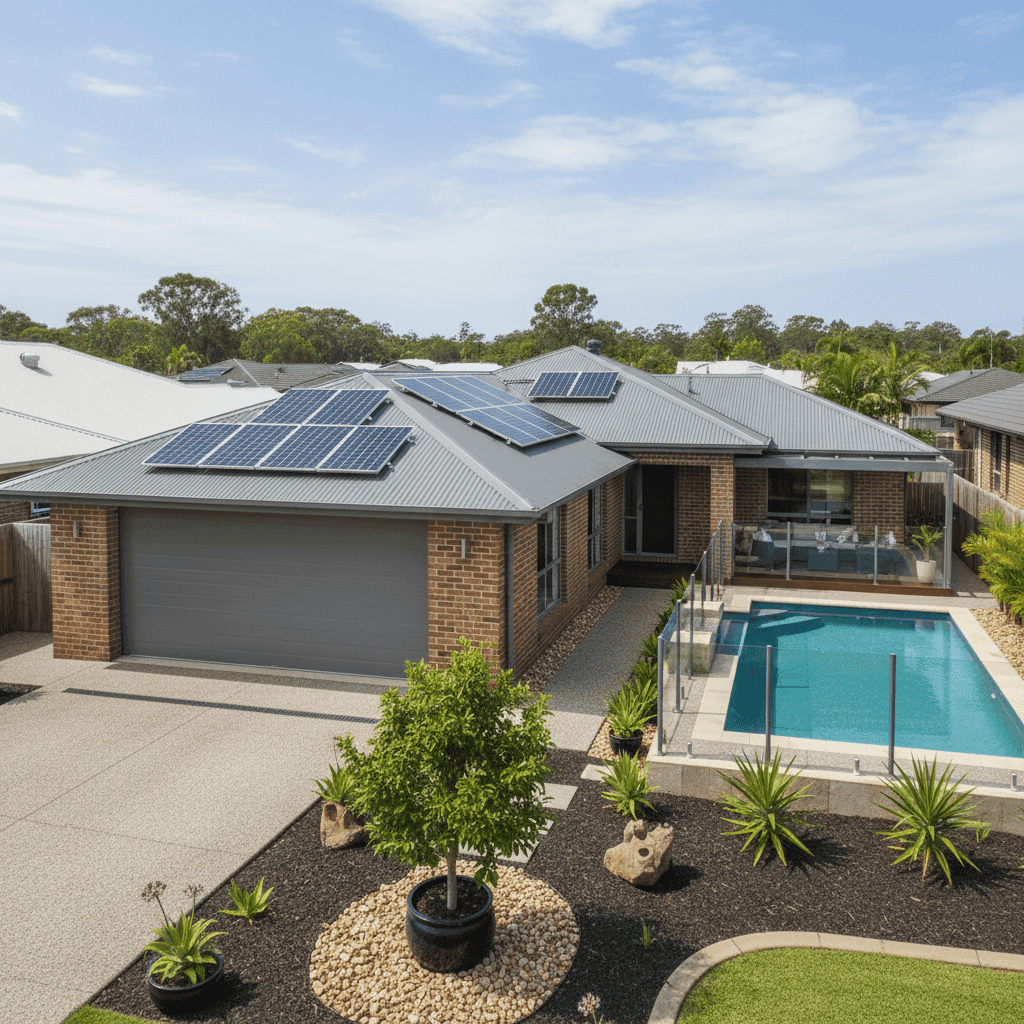

Cyclone Risk Zone This is the single biggest factor. Yeppoon falls within a designated cyclone risk area, and insurers price this in significantly. Cyclone cover typically includes damage from wind, rain, and storm surge associated with tropical weather events. It's non-negotiable for coastal Queensland properties and accounts for a meaningful portion of any premium in this region.

Construction Quality The home's brick veneer walls and Colorbond steel roof are both viewed favourably by insurers. Brick veneer offers good structural resilience, while Colorbond steel is specifically engineered to handle high-wind environments and is far more cyclone-resistant than older corrugated iron or tile roofs. The concrete slab foundation also adds stability. Together, these features signal lower rebuild risk to underwriters.

Above-Average Fittings With above-average fittings quality, the building sum insured of $889,000 is appropriate for a 214 sqm home of this standard. Underinsurance is a significant risk for homeowners with quality fixtures and finishes — if the sum insured doesn't reflect the true cost to rebuild, you could face a shortfall at claim time.

Swimming Pool and Solar Panels Both the pool and solar panel system are relevant to insurers. Pools introduce liability considerations and can add to the cost of a claim if damaged during a storm. Solar panels — increasingly common in Queensland — need to be specifically accounted for in your building sum insured, as replacement costs can be substantial. Confirm with your insurer that both are covered under your policy.

Year of Construction Built in 2010, this home benefits from post-2006 Queensland building codes, which introduced significantly stricter cyclone-resistance standards following reviews after Cyclone Larry. Newer builds generally attract more competitive premiums than older homes in high-wind zones.

---

Tips for Homeowners in Yeppoon

1. Review your building sum insured annually Construction costs in Queensland have risen sharply in recent years. A sum insured that was adequate three years ago may no longer cover a full rebuild today. Use a building cost calculator or ask your insurer to reassess, particularly given the above-average fittings in this home.

2. Confirm your solar panels and pool are explicitly covered Don't assume these are automatically included. Check your Product Disclosure Statement (PDS) to confirm coverage for your solar system — including panels, inverter, and mounting hardware — and clarify how pool damage is handled in a cyclone or storm event.

3. Prepare a home inventory for your contents claim With $195,000 in contents cover, having a detailed, up-to-date inventory of your belongings makes a world of difference if you ever need to make a claim. Photograph valuables, keep receipts where possible, and store the inventory securely in the cloud or offsite.

4. Compare quotes before each renewal Insurers don't always reward loyalty with competitive pricing. The market in coastal Queensland is active, and premiums can vary significantly between providers for the same property. Running a fresh comparison at renewal — especially given the spread between the 25th percentile ($3,414) and 75th percentile ($5,370) in Yeppoon — could save you hundreds of dollars a year.

---

Compare Your Own Quote

Whether you're a Yeppoon local or considering a property on the Capricorn Coast, it pays to know where your premium sits relative to the market. CoverClub makes it easy to compare home and contents insurance quotes in one place, with transparent pricing data to help you make a confident decision. Get a quote today and see how your property stacks up.