Getting a home insurance quote can feel like reading a foreign language — especially when you're not sure whether the number you're looking at is reasonable or whether you're being overcharged. This article breaks down a real building insurance quote for a four-bedroom, free-standing home in Zilzie, QLD 4710, helping you understand what's driving the premium and how it stacks up against the broader market.

---

Is This Quote Fair?

The annual premium for this property came in at $4,613 per year (or $442/month) for building-only cover, with a sum insured of $874,000 and a building excess of $5,000. CoverClub's pricing engine has rated this quote as FAIR — around average.

That rating reflects where this quote sits relative to comparable properties in the area. It's not a bargain, but it's not an outlier either. Given the combination of risk factors associated with this property and its location (more on those shortly), landing near the middle of the market is a reasonable outcome.

It's worth noting that a $5,000 building excess is on the higher end of the scale. Opting for a higher excess is a common way to reduce your annual premium, but it does mean a larger out-of-pocket cost if you ever need to make a claim. Make sure that figure is genuinely comfortable for your financial situation.

---

How Zilzie Compares

To put this quote in context, here's how the $4,613 annual premium measures up across different benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $4,613/yr |

| Zilzie Suburb Average | $3,796/yr |

| Zilzie Suburb Median | $4,048/yr |

| Zilzie 25th Percentile | $2,665/yr |

| Zilzie 75th Percentile | $4,986/yr |

| QLD State Average | $4,547/yr |

| QLD State Median | $3,931/yr |

| National Average | $2,965/yr |

| National Median | $2,716/yr |

| Livingstone LGA Average | $13,146/yr |

A few things stand out here. First, this quote sits above the Zilzie suburb average of $3,796 and the median of $4,048, but comfortably within the 25th–75th percentile range ($2,665–$4,986). That means roughly half of comparable Zilzie properties are paying somewhere between those two figures — and this quote falls in the upper half of that band.

Second, the quote is broadly in line with the Queensland state average of $4,547, which speaks to how elevated coastal and cyclone-prone areas in QLD push premiums well above the national norm.

That national comparison is striking: the national average of $2,965 is nearly $1,650 less per year than this quote. That gap isn't unusual for coastal Queensland — it simply reflects the higher natural hazard risk that insurers price into policies in this part of the country.

Perhaps most telling is the Livingstone LGA average of $13,146. This quote is dramatically lower than that figure, which suggests the LGA average may be skewed by higher-value properties or more exposed locations within the council area. You can explore more local data on the Zilzie suburb stats page, the Queensland state overview, or the national home insurance stats.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on what insurers charge. Understanding them helps you see why the premium lands where it does.

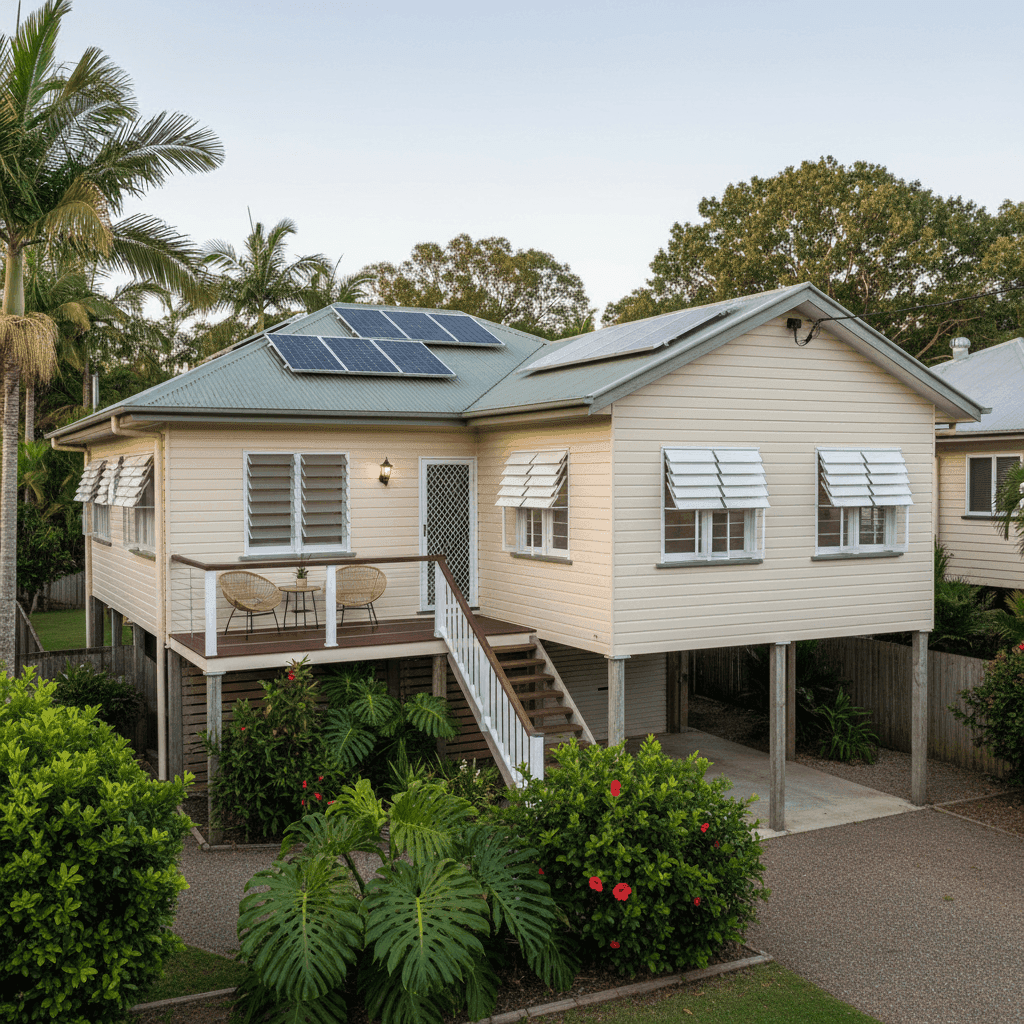

Cyclone Risk Area

This is the single biggest risk factor for properties in Zilzie. Located on the Capricorn Coast in Central Queensland, the area falls within a designated cyclone risk zone. Insurers apply significant loading to premiums in these regions to account for the potential cost of wind, storm surge, and structural damage from tropical weather events. This alone can add hundreds — sometimes thousands — of dollars to an annual premium compared to a similar home in Brisbane or Melbourne.

Fibro Asbestos Exterior Walls

Fibro asbestos cladding is a construction material that was widely used in Australian homes built before the 1990s. However, this home was built in 2009, which raises questions about whether the cladding material has been correctly identified or whether it's a fibre cement product (non-asbestos) that has been categorised under an older classification. Either way, insurers tend to view fibro construction with caution due to the potential costs involved in repair or replacement, which can push premiums higher than those for brick or rendered homes.

Elevated Foundation (Poles)

The home is elevated by at least one metre on poles — a classic Queenslander-style build well suited to flood-prone and coastal environments. Elevation can actually work in your favour with some insurers, particularly for flood risk, as it reduces the likelihood of inundation damage to the main living areas. However, the subfloor space and supporting structure also introduce their own repair considerations.

Steel/Colorbond Roof

Colorbond roofing is generally viewed positively by insurers. It's durable, cyclone-resistant when properly installed, and less prone to damage from hail than terracotta tiles. This is a feature that may help moderate the premium somewhat.

Solar Panels

Solar panels are noted on this property. Most standard building policies will cover rooftop solar as part of the building sum insured, but it's worth confirming with your insurer that the panels and inverter are explicitly included — and that the sum insured is sufficient to cover replacement costs if they're damaged in a storm or cyclone event.

Building Size & Sum Insured

At 214 sqm with a sum insured of $874,000, the per-square-metre rebuild cost works out to approximately $4,084/sqm. This is within a reasonable range for a quality build in regional coastal Queensland, particularly given elevated construction and the current cost of materials and labour.

---

Tips for Homeowners in Zilzie

1. Review your cyclone preparedness and policy inclusions Living in a cyclone risk zone means your policy's storm and cyclone clauses matter enormously. Read the Product Disclosure Statement carefully to understand what's covered, what the specific excess is for cyclone events (some insurers apply a separate, higher cyclone excess), and whether temporary accommodation is included if your home becomes uninhabitable.

2. Verify your wall construction classification If your home was built in 2009 and is classified as fibro asbestos, it's worth confirming this with your builder's records or a building inspector. Fibre cement (non-asbestos) products are common in modern construction and may attract a different rating. Correcting a misclassification could reduce your premium.

3. Ensure your sum insured reflects current rebuild costs Construction costs in Queensland have risen significantly in recent years. With a sum insured of $874,000 for a 214 sqm home, you're currently sitting at around $4,084/sqm — reasonable, but worth revisiting annually. Underinsurance is one of the most common and costly mistakes homeowners make. Use a building cost calculator or speak to a quantity surveyor to sense-check your figure each year.

4. Compare quotes annually — don't auto-renew Insurance loyalty rarely pays off. Premiums can shift substantially from year to year, and different insurers price cyclone-zone properties very differently. Shopping around at renewal time — or using a comparison tool like CoverClub — takes minutes and can save you hundreds of dollars.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for the first time, comparing quotes is the fastest way to know if you're getting a fair deal. Get a home insurance quote through CoverClub and see how multiple insurers price your specific property — in minutes, with no obligation.